USD/JPY Weekly Forecast: The Omicron identity

![]()

- Omicron panic on Friday November 26 set the week’s stage.

- Currency and Treasury markets waiting for proof the variant is dangerous.

- US NFP weakens Treasury yields and the dollar as payrolls miss forecast.

Last Friday’s reaction to the discovery of the new Omicron variant set the stage for this week’s trading. The Japanese yen’s long standing safe-haven status drove the USD/JPY down 2%, by far the largest US dollar loss for the day. A collapse in US Treasury yields undermined the greenback in all major pairs except the USD/CAD which was aided by a 12.8% plunge in West Texas Intermediate. The US 10-year Treasury yield lost 16 basis points on the day, closing at 1.482%.

Markets remained wary all week as Omicron case reports began to trickle in from various countries and US states, even though there were no indications of heightened danger or vaccine avoidance from the new strain. Preliminary observations from the doctor in South Africa who identified the first mutated virus noted the cases she had seen were all mild without complications.

Monday’s close at 113.66 was the high for the week and the Tuesday drop to 112.52 was the lowest trade since October 11. Wednesday’s close below 113.00 support at 112.81 did not generate an attempt at the weakly defended passage to 112.25.

Markets are waiting for information on the new variant. Virus mutations are a matter of course, and the normal evolution is toward higher transmission and lower lethality.

The Treasury market yield panic was not mitigated by Federal Reserve Chair Jerome Powell’s twin comments that it might be time to retire the ‘transitory’ description of inflation and that an advancement in the pace of the taper might be in order at the December 15 Federal Open Market Committee (FOMC) meeting.

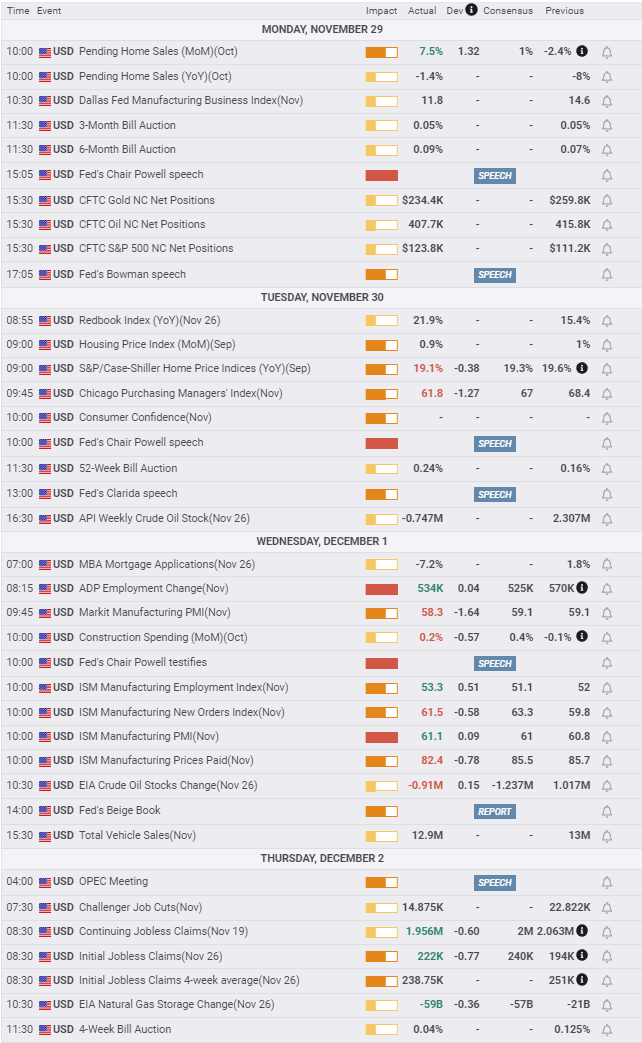

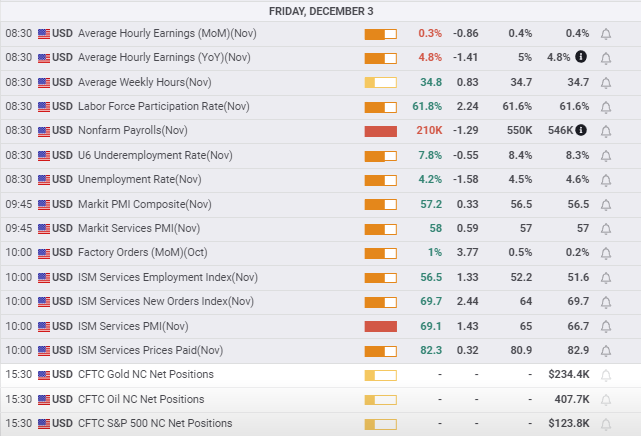

The US Nonfarm Payroll report on Friday missed its headline forecast of 550,000 new jobs producing just 210,000, but in other respects it illustrated how far the labor market has come this year.

Unemployment fell to 4.5% and underemployment dropped to 7.8%, both far better than predicted, and the lowest of the pandemic. The labor participation rate climbed to 61.8% its highest since March 2020.

Purchasing Managers’ Indexes (PMI) for the manufacturing and service sectors were strong. Overall PMI in service set an all-time record at 69.1. The New Orders Index was unchanged at 69.7, another record and much better than the 64 projection. Initial Jobless Claim rose to 222,000 in the latest week from 194,000 prior, indicating that the labor market continues to heal.

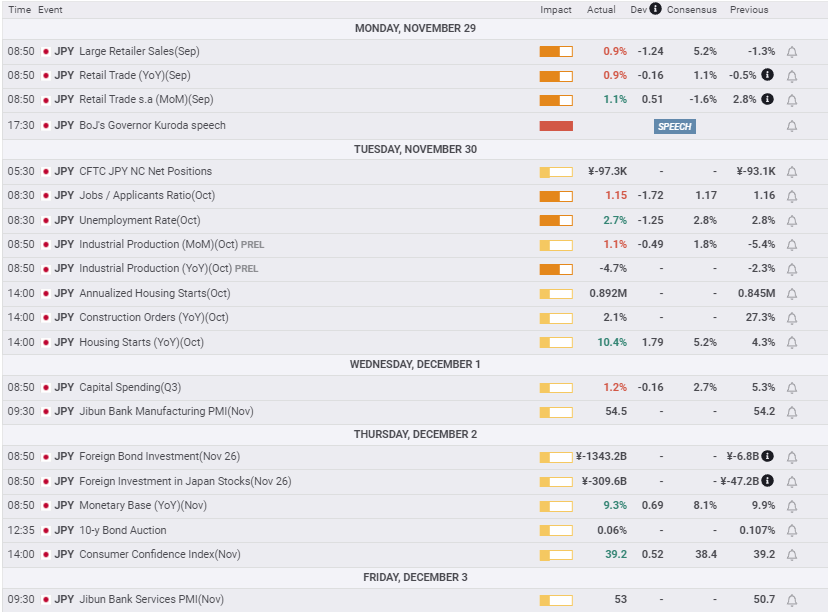

Japanese economic information was mixed with little market impact. Retail Trade (sales) was slightly weaker than forecast for the year in September, though purchases at large stores were just 0.9%, less than a fifth of the 5.2% estimate. Industrial Production in October was weaker than predicted and the annual change was -4.7%, its worst reading since January.

USD/JPY outlook

Last week’s panic reaction to the Omicron advent is the fulcrum for the USD/JPY and markets in general. At question are the objective considerations about the health danger and contagion of the strain but also how governments will respond.

If the new virus is less difficult but more transmissible, governments may still opt for restrictions and closures that will inhibit the global recovery. The plunge in oil prices and their limited return is a clear indication that commodity markets view new lockdowns as a distinct possibility.

Credit markets take the same jaundiced view, that central banks, as governments, will respond to any new problem as they answered the previous ones.

If the Omicron strain shows to be little different in outcome, it will take time for markets to accept that conclusion. Governments around the world are not likely to downplay the new variant but to use it as a pressure to supplement current economic and social restrictions.

In this week’s trading, the USD/JPY barely moved from its panic close last Friday at 113.13. Omicron is an unresolved issue. Given the weakness of support in the USD/JPY below 113.000 and the possibility that new economic restrictions will be forthcoming in many countries, the bias in the USD/JPY is lower.

If there is widespread notice that Omicron is not a threat, the USD/JPY will quickly regain the initiative.

Japan statistics November 29–December 3

US statistics November 29–December 3

FXStreet

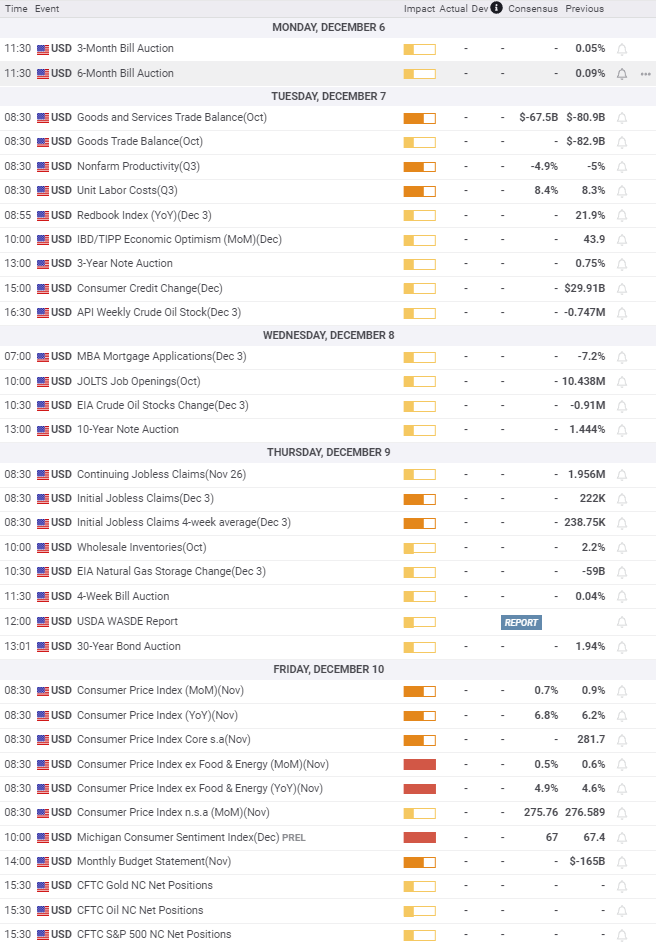

Japan statistics December 6–December 10

FXStreet

US statistics December 6–Decemebr 10