BlueGuardian: A Replacement & a Quiet Request

It has been roughly a year since my last interaction with Blue Guardian (Support ticket turning fraud)

since then: nothing. No follow-up, no apology, no (direct) contact of any kind. That changed yesterday.

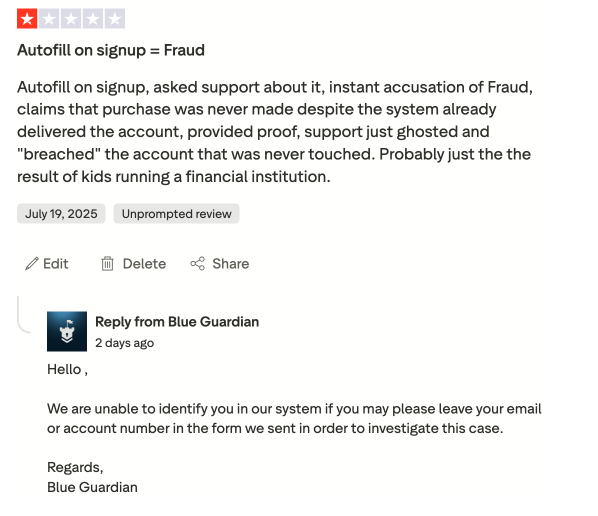

After I left a 1-star review on Trustpilot…

On Trustpilot: Publicly, Blue Guardian replied to my review with the standard boilerplate: they could not locate an account matching my details, and invited me to contact support with more information. (wich were provided when the original review was composed)

Privately, around the same time, the same company reaches out, casually mentioning “got you a new account” alongside the automated welcome emails.

and almost in passing, asking if i could “remove my comments.”

If they genuinely couldn’t find my account, how did they know which account to reissue?

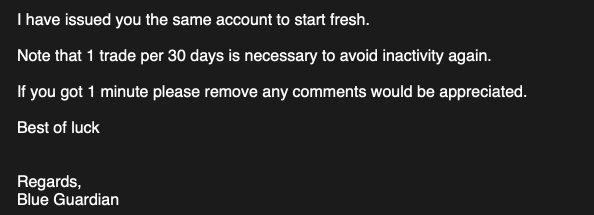

well since we are warned, i made sure the profile issues were corrected first. Took the person just a few sec to come up with a solution (create a new profile) and he will move the account in this then, well that was easy, they should have done this 1 year ago…

Well, lets have an actual look on what we got.

Reading the Fine Print on the Reissued Account

Since the account was now sitting in my dashboard again, I did what I should have done a year ago: RTFM.

**the public-facing pages and the binding contract don’t tell quite the same story.**

The Starter account is marketed with language like “24hr payout guarantee,” a “bi-weekly schedule” example in their own profit walkthrough, and a general help article stating payouts are “on demand… at any time.” Reasonable people would read that as: you trade, you get paid, repeatedly, on a cycle.

The signed contract, the one you only see *after* you’ve already paid, tells a different story.

Buried in a section called “Profits and Pay Periods,” after defining a recurring 14-day “Pay Period” (which reinforces the recurring impression), it adds a single subordinate clauses:

- “…the Trader has not previously received a payout under the Instant Funding Starter program.”

- “Upon payment of the Profit Share, the BG Customer Account shall no longer be eligible for further payout requests under the Instant Funding Starter program.”

In plain English: **one payout, ever, capped at (5%) and you are done. ** Not “bi-weekly.” Not “on demand.” just Once.

This isn’t disclosed anywhere on the sales pages. It isn’t in the Terms & Conditions publicly avaiable on the website.

The only places it appears clearly are one dedicated help-center article, and a single dependent clause in the contract.

To Be Fair: The Starter Tier Is Actually a pretty good Deal!

I don’t want this to read as a one-sided takedown, so here’s the other side of it.

The Instant Starter account is priced at roughly **20% of what the equivalent account without the one-payout limitation costs**.

Looked at on its own, that’s not a bad deal:

- you get the full Instant funding experience, the same platform, the same backend, the same rules engine, the same trading conditions.

for a fraction of the price of the “real” product. As a way to test-drive whether Blue Guardian’s execution, platform, and rules actually work for you before committing to a full-price account. This actually is a genuinely reasonable concept. A cheap, capped trial run isn’t inherently a bad idea especially since you getting paid for doing the trial.

The problem isn’t the pricing or the concept. It’s the *presentation*. Nowhere it says “this is a cheap trial version,” “this payout is one-time only,” “after this you’d need the full-price account for ongoing payouts” is communicated anywhere a buyer would naturally look before purchasing. Instead, the marketing language (bi-weekly schedules, “payouts” plural, “on demand at any time”) makes the Starter tier sound like a smaller version of the *same ongoing product*, not a one-shot trial of it.

If Blue Guardian simply said, upfront, “this is a low-cost trial account, good for one payout up to 5% so you can evaluate us before buying the full version”

that would be a fair and honestly quite attractive pitch since no other prop firm actually does this.

Instead, the trial framing is something you only piece together after the fact, by cross-referencing a help article and a contract clause. Given everything else I’ve described above, that omission doesn’t read as an accident to me. And given my prior experience with this firm, it leaves what could have been a genuinely good offer feeling sour.

Those things matters beyond the Fine Print

The reissued account itself isn’t the story, it’s the account I already paid for, finally reinstated under a corrected profile, which is the bare minimum given what happened the first time around. The story is the pattern, repeating itself across a year.

A year ago: a routine support request (please fix the country field) met with accusations instead of help, ending in a breached account.

Today: a public denial on Trustpilot (“we can’t find your account”) sitting alongside a private conversation that reissues that exact account, paired with a quiet, unspecified request to make the negative review disappear.

before the original profile issue was even resolved! And underneath both: marketing language that implies one thing about payouts, while the document you actually sign says something significantly different.

None of these things, taken alone, prove bad faith. Support teams get things wrong. Contracts have boilerplate. Reviews get canned replies. Profile corrections take time to process.

But three for three, over the course of a year, starts to look less like coincidence and more like culture.

Thoughts

I want to be clear about I’m not saying the reissued account was a bribe, nobody offered me anything explicitly in exchange for removing the review, and I haven’t agreed to remove it. I’m also not saying the payout terms are wrong, firms are entitled to structure their products however they like, including one-time promotional-style payouts.

What I am saying is this: if a company’s first instinct after a bad review is a quiet private message asking, without specifics, for it to be taken down, while *simultaneously and publicly* claiming they can’t even find your account, that tells you more about how they handle criticism than any FAQ page ever will.

And if the documentation a customer is shown *before* paying describes something materially different from what the contract says *after* paying,

that’s not an oversight worth dismissing. That’s worth writing down.