General Market Analysis – 01/07/26

US Stocks Drive Higher on Final Day of the Quarter – Nasdaq up 1.5% US financial markets extended their strong run overnight, with equity indices finishing higher once again to cap one…

US Stocks Drive Higher on Final Day of the Quarter – Nasdaq up 1.5% US financial markets extended their strong run overnight, with equity indices finishing higher once again to cap one…

IC Markets Global – Asia Fundamental Forecast | 01 July 2026 What happened in the U.S. session?Financial markets were driven by a combination of stronger-than-expected U.S. macroeconomic data, easing geopolitical concerns in…

Traders are expecting to see a very lively session on Thursday this week with the key US employment data due out a day early due to the big US Independence Day holiday…

IC Markets Global – Europe Fundamental Forecast | 30 June 2026 What happened in the Asia session?Chinese macroeconomic data and broad market positioning ahead of major U.S. economic releases later this week.…

The post Ex-Dividend 01/07/2026 first appeared on IC Your Trading Edge | Official Blog.

DXY (U.S. Dollar Index): Potential Direction: Bullish Overall momentum of the chart: Bearish Price could see a short-term pullback toward the pivot before rising again toward the 1st resistance. Pivot: 101.12…

Global Markets: Asian Stock Markets : Nikkei up 1.45%, Shanghai Composite up 0.20% Hang Seng down 0.31% ASX down 0.04% Commodities : Gold at $3,988.12 (-1.26%) Silver at $7.820 (-1.38%), Brent Oil…

US Stocks Rally on Peace Hopes Again – Nasdaq up 2%Global financial markets began the week on a positive footing overnight as improving sentiment surrounding developments in the Middle East encouraged investors…

IC Markets Global – Asia Fundamental Forecast | 30 June 2026 What happened in the U.S. session?Markets were driven primarily by geopolitical developments, positioning ahead of this week’s key U.S. labor market…

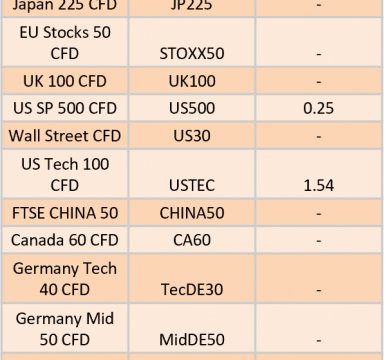

Dear Client, Please find our updated Trading schedule and general information related to the US Independence Day holiday on Saturday, 4 July, 2026. Liquidity over the holidays is expected to be particularly…

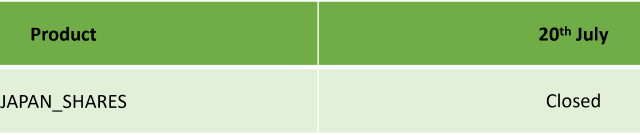

Dear Client, Please find our updated Trading schedule and general information related to the Japan Marine Day holiday on Monday, 20 July, 2026. Liquidity over the holidays is expected to be particularly…

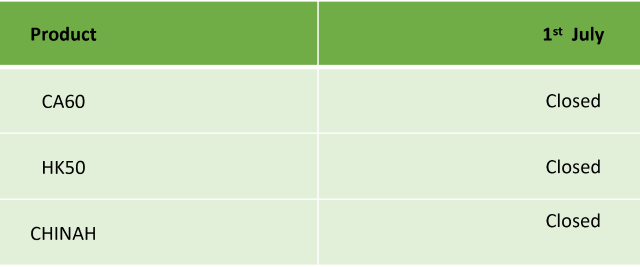

Dear Client, Please find our updated Trading schedule and general information related to the Hong Kong Special Administrative Region Establishment Day holiday on Wednesday, 1 July, 2026. Liquidity over the holidays is…