Friday 24th July 2026: Technical Outlook and Review

DXY (U.S. Dollar Index): Potential Direction: Bearish Overall momentum of the chart: Bearish The price has already reacted off the pivot and may continue its bearish move toward the 1st support.…

DXY (U.S. Dollar Index): Potential Direction: Bearish Overall momentum of the chart: Bearish The price has already reacted off the pivot and may continue its bearish move toward the 1st support.…

Global Markets: Asian Stock Markets : Nikkei down 3.01%, Shanghai Composite down 1.20% Hang Seng down 1.23% ASX down 0.95% Commodities : Gold at $4,033.90 (-0.40%) Silver at $57.650 (-0.70%), Brent Oil…

US Stocks Hit as War Escalates – Nasdaq down 2.15%Global financial markets traded sharply lower overnight as investors continued to grapple with escalating geopolitical tensions in the Middle East and growing concerns…

IC – Asia Fundamental Forecast | 24 July 2026 What happened in the U.S. session?Markets were dominated by renewed geopolitical risk, a sharp surge in crude oil prices, and risk-off sentiment across…

Global Markets: Asian Stock Markets : Nikkei up 0.68%, Shanghai Composite down 0.19% Hang Seng up 1.33% ASX up 0.60% Commodities : Gold at $4,127.12 (-0.60%) Silver at $60.015 (-0.46%), Brent Oil…

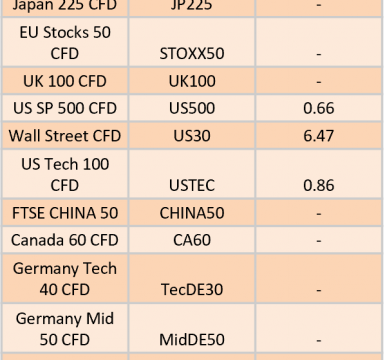

The post Ex-Dividend 24/07/2026 first appeared on IC Your Trading Edge | Official Blog.

DXY (U.S. Dollar Index): Potential Direction: Bullish Overall momentum of the chart: Bearish The price could make a short-term pullback toward the pivot before rising again toward the 1st resistance Pivot:…

IC – Europe Fundamental Forecast | 23 July 2026 What happened in the Asia session?During today’s Asian session, the primary market-moving event was the Australian June Labour Market Report, which came in…

US Stocks Slip Ahead of Key Earnings – Nasdaq down 0.6% Global markets traded cautiously overnight as investors weighed the ongoing escalation of tensions in the Middle East against the prospect of…

IC – Asia Fundamental Forecast | 23 July 2026 What happened in the U.S. session?Escalating tensions in the Middle East fueled another strong rally in crude oil, increasing concerns that higher energy…

IC – Europe Fundamental Forecast | 22 July 2026 What happened in the Asia session?Markets were driven by a combination of Japanese trade data, continued weakness in the Japanese yen, and ongoing…

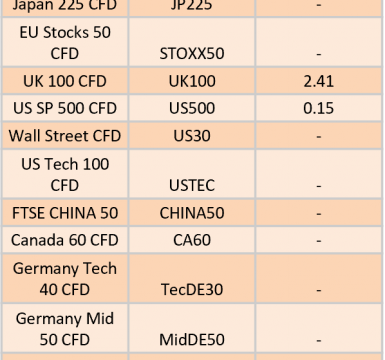

The post Ex-Dividend 23/07/2026 first appeared on IC Your Trading Edge | Official Blog.