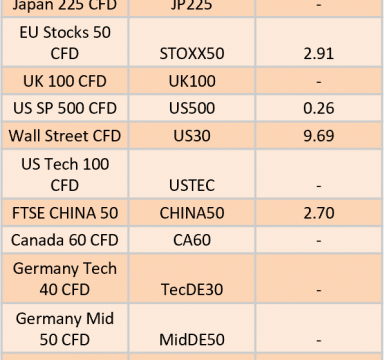

Ex-Dividend 21/07/2026

The post Ex-Dividend 21/07/2026 first appeared on IC Your Trading Edge | Official Blog.

The post Ex-Dividend 21/07/2026 first appeared on IC Your Trading Edge | Official Blog.

DXY (U.S. Dollar Index): Potential Direction: Bullish Overall momentum of the chart: Bearish The price could make a short-term pullback toward the pivot before rising again toward the 1st resistance Pivot:…

Global Markets: Asian Stock Markets : Nikkei down 4.03%, Shanghai Composite up 0.07% Hang Seng up 1.80% ASX down 0.00% Commodities : Gold at $4,015.55 (-2.05%) Silver at $56.915 (1.03%), Brent Oil…

IC – Asia Fundamental Forecast | 20 July 2026 What happened in the U.S. session?Heightened geopolitical tensions in the Middle East, which continued to dominate sentiment ahead of a relatively quiet macroeconomic…

IC – Europe Fundamental Forecast | 20 July 2026 What happened in the Asia session?Escalating U.S.-Iran tensions and renewed disruptions to shipping through the Strait of Hormuz drove a sharp rise in…

US Markets Fall as War Escalates – Nasdaq Off 1.4%US stock markets closed lower on Friday, capping off a difficult week for global equities as investors continued to scale back exposure to…

Last week saw a couple of key themes dominate as the week progressed. One was the definite increase in hostilities in the Middle East, which has also continued through the weekend, while…

Global Markets: Asian Stock Markets : Nikkei down 4.71%, Shanghai Composite down 1.64% Hang Seng down 1.99% ASX down 0.73% Commodities : Gold at $3,993.12 (0.04%) Silver at $55.600 (-1.03%), Brent Oil…

IC – Europe Fundamental Forecast | 17 July 2026 What happened in the Asia session?Market sentiment was driven primarily by geopolitical developments and positioning ahead of key U.S. events later in the…

IC – Asia Fundamental Forecast | 17 July 2026 What happened in the U.S. session?Markets were driven primarily by a combination of softer U.S. inflation signals, stronger-than-expected economic activity data, ongoing geopolitical…

DXY (U.S. Dollar Index): Potential Direction: Bearish Overall momentum of the chart: Bearish The price could see a short-term pullback toward the pivot before continuing its bearish move down toward the…

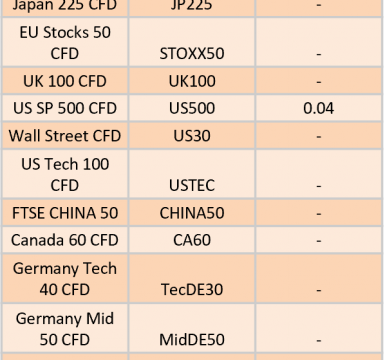

The post Ex-Dividend 20/07/2026 first appeared on IC Your Trading Edge | Official Blog.