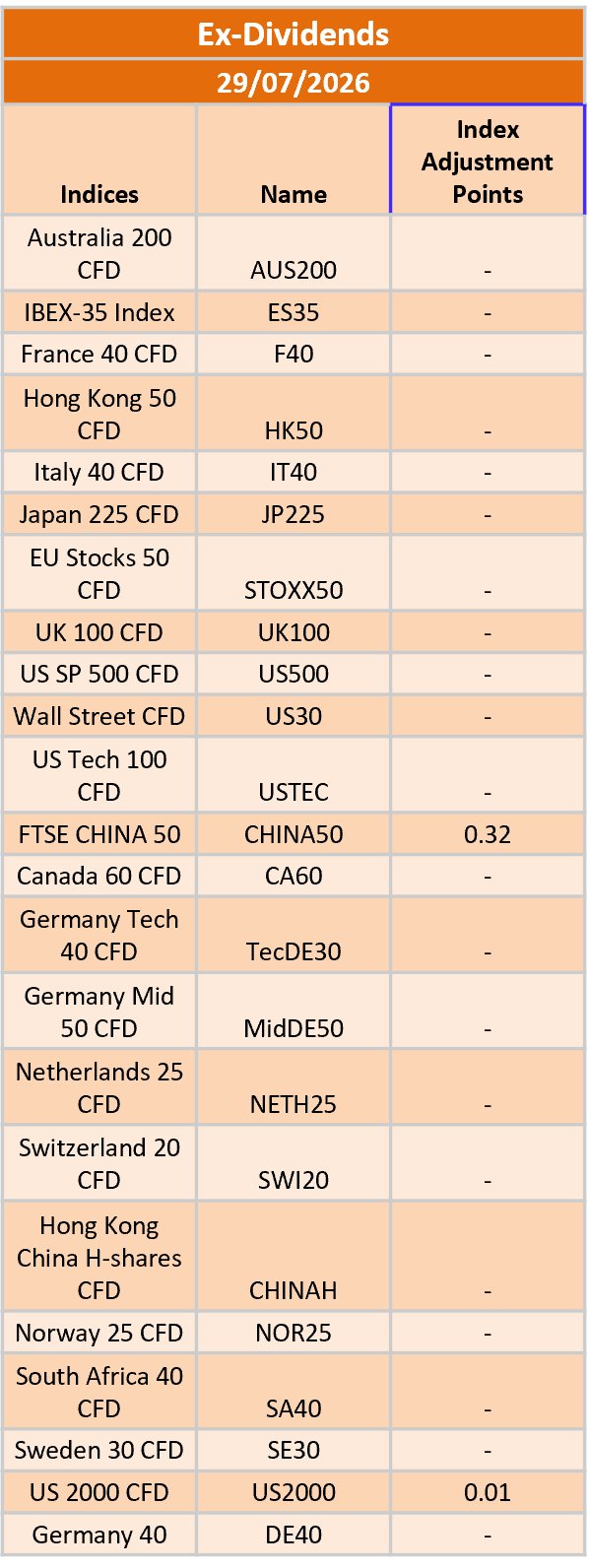

Ex-Dividend 29/07/2026

{kind=link}

The post Ex-Dividend 29/07/2026 first appeared on IC Your Trading Edge | Official Blog.

Forex Market News .. collected from serval sources, all in one place for you to review.

[most entries here, will be auto-removed after 90 days]

The post Ex-Dividend 29/07/2026 first appeared on IC Your Trading Edge | Official Blog.

USD:

The US dollar opened the week lower yesterday after the US halted its strikes following 13 consecutive days of attacks, while Iran pledged to maintain a ceasefire so long as the US remained on pause.

This has led to some optimism as traders took this latest development as an early sign of a potential de-escalation and triggered a selloff in oil prices.

Despite this positive development, the greenback erased the losses and printed a new weekly high. The support hasn’t come from Treasury yields or economic data, so this suggests that it might have been just hedging activity ahead of tomorrow’s FOMC decision.

The Fed is expected to hold interest rates steady but…

QatarEnergy is reported to have extended force majeure for its European buyers until the end of September at least, further reaffirming that the energy disruption from the Strait of Hormuz is having a prolonged impact. As a reminder, the company is one of the world's largest LNG exporters and while Europe is not their biggest customer base, the impact here is just a hint of what is being felt in Asia surely. Still, there will be some European players heavily impacted by the continuation of the status quo.

For some context, no LNG tankers have made their way out of the Strait of Hormuz since 16 July. And even if there are shadow fleet movements (unlikely for Qatar), the number is likely to be rather minimal.

One of its biggest European…

With all that is happening with US-Iran developments and the big selloff in tech shares, let's not forget that there is still the central bank bonanza this week. And on that note, none is bigger than the FOMC meeting that will come tomorrow.

The Fed policy decision in itself is expected to be rather straightforward. The central bank is widely expected to keep interet rates unchanged, but will there be a more hawkish twist to follow after?

Personally, I feel that the threshold for that is a bit high. That especially with the risks involved in changing their communique, not least with still some way to go before the next meeting in September. Who knows what will happen with US-Iran developments by then.

That being said, some analysts are…

IC – Europe Fundamental Forecast | 28 July 2026

What happened in the Asia session?

Market attention was dominated by Reserve Bank of Australia (RBA) Governor Michele Bullock’s speech, while traders also continued to react to geopolitical developments and position ahead of this week’s major central bank meetings, including the Federal Reserve and the Bank of Japan. Bullock reiterated that underlying inflation remains too high and stressed that the RBA is prepared to raise interest rates further if required to return inflation to its 2–3% target.

What does it mean for the Europe & US sessions?

Traders are primarily focused on central bank commentary, U.S. consumer sentiment, and persistent geopolitical risks that continue to influence…

U.S. stock futures edged lower in early Asian trading on Tuesday as investors prepared for a crucial week featuring earnings from major technology companies and the Federal Reserve’s latest interest rate decision.

S&P 500 futures fell 0.1%, while Nasdaq 100 futures declined 0.5%. Dow Jones…

USD:

The US dollar opened the week lower yesterday after the US halted its strikes following 13 consecutive days of attacks, while Iran pledged to maintain a ceasefire so long as the US remained on pause.

This has led to some optimism as traders took this latest development as an early sign of a potential de-escalation and triggered a selloff in oil prices.

Despite this positive development, the greenback erased the losses and printed a new weekly high. The support hasn’t come from Treasury yields or economic data, so this suggests that it might have been just hedging activity ahead of tomorrow’s FOMC decision.

The Fed is expected to hold interest rates steady but…

Potential Direction: Bearish

Overall momentum of the chart: Bearish

The price has already reacted off the pivot and may continue its bearish move toward the 1st support.

Pivot: 101.52

Supporting reasons: Identified as an overlap resistance, where selling pressures could intensify and potentially cap any upward retracement

1st support: 101.20

Supporting reasons: Identified as a pullback support, indicating a potential area where the price could again stabilize.

1st resistance: 101.70

Supporting reasons: Identified as a swing high resistance, indicating a potential area that could halt any further upward movement

Potential Direction: Bearish

Overall momentum of the…

The market is swiftly turning its attention back to fundamentals this week despite the improving situation in the Middle East. This week’s Federal Reserve Bank meeting is one of the most highly anticipated interest rate decisions of the year, and maybe even the last few years. Just a week ago the odds of a 25-basis point rate hike were sitting around the 16% mark, however the increased inflationary concerns from the situation in the Middle East has led to the market now pricing in a 40% chance of a hike which puts the meeting very much in the ‘live’ category. Despite a sharp deescalation in the conflict over the past few days, US yields and the dollar remain bid near annual highs.

The market is also wary of the new Kevin Warsh led FOMC…

FUNDAMENTAL OVERVIEW

The S&P 500 has been mostly rangebound this month as the US-Iran crisis brought back inflation and growth risks. This has also happened amid overcrowded stock market positioning which has led to deleveraging across the board.

The latest weakness seems to be more about hedging/deleveraging activity ahead of tomorrow’s FOMC decision rather than fresh Middle East news. In fact, the ceasefire is still intact, and the diplomatic efforts are ongoing (although things can change on a dime).

The Fed is expected to hold interest rates steady but there might be one or two dissenters voting for a rate hike at this meeting already. The forward guidance will…

The reading continues to reaffirm a further rebound in French consumer sentiment in July, though keeping well below the peak earlier this year in February of 92. And overall, the estimate is still well below the long-term average reading of 100.

French households are seen feeling better about their personal financial situation, past and future, in July. Both estimates of the past and expected financial situation showed a two point increase to -26 and -14 respectively on the month. Besides that, consumers also were more optimistic about their expected saving capacity and current ability to save. So, there's that.

But perhaps the most notable part of the report is a drop in inflation…

US Stocks Mixed as Oil Extends Sharp Decline on Middle East Optimism – Dow up 0.5%

US financial markets delivered a mixed performance overnight as investors continued to respond positively to signs of easing tensions in the Middle East. Sentiment improved after President Trump stated that the US was having “good talks” with Iran, raising hopes that diplomatic progress could eventually lead to increased oil exports through the Strait of Hormuz and help alleviate concerns over global energy supply.

The prospect of improving supply conditions weighed heavily on crude oil prices, with Brent crude tumbling 9.26% to US$87.82 a barrel, while West Texas Intermediate (WTI) fell 8.19% to US$82.00. The sharp decline in energy prices also…

{kind=link}