Articles

US treasury to complete coupon auction w/ sale of 7 year notes at the bottom of the hour

423912 November 26, 2025 23:30 Forexlive Latest News Market News

The U.S. Treasury will complete the coupon auctions for the week with the sale of 7 year notes at the bottom of the hour ($44 billion). The auction is a little early ahead of the Thanksgiving day holiday. Despite the early auction, the bond market will remain open for the rest of the trading day.

The auction results will be compared to the 6 month averages of the major components to determine the relative demand for both domestic and international buyers:

- Tail -0.6 basis points

- Bid to cover 2.56X

- Direct buyers (domestic buyers) 23.5%

- Indirect buyers (international buyers) 67.2%

- Dealers (they take the balance) 9.2%

The 2 and 5 year note auctions were met with average demand.

This article was written by Greg Michalowski at investinglive.com.

US Durable goods orders for September 0.5% versus 0.3% estimate

423911 November 26, 2025 20:39 Forexlive Latest News Market News

- Prior month (August 2.9% revised to 3.0%)

- Durable goods orders for September 0.5% vs 0.3% expected.

- Durable goods orders ex Transport 0.6% vs 0.2% expected. The prior of 0.3% revised to 0.5%

- Durable goods ex defense 0.1% vs 1.9% last month

- Non-Defense capital goods ex air 0.9% vs 0.2% expected. Prior month 0.4% revised to 0.9%

The data comes in stronger than expected with higher revisions. The initial jobs claims were also better than expected. The initial jobs claims more recent than the durable goods orders.

The general expectations is that the growth will have slowed because of the shutdown, but any slowdown would be recovered .

This article was written by Greg Michalowski at investinglive.com.

US initial jobless claims 216K vs 225K expected

423910 November 26, 2025 20:39 Forexlive Latest News Market News

- Prior 220K (revised to 222K)

- Continuing claims 1960K vs 1969K expected

- Prior 1974K (revised to 1953K)

Jobless claims continue to point to a “low firing, low hiring” labour market. The data is not going to change anything for the Fed at this point though with the probabilities for a December cut now standing around 79%.

This article was written by Giuseppe Dellamotta at investinglive.com.

investingLive European markets wrap: Another UK budget fiasco

423909 November 26, 2025 20:14 Forexlive Latest News Market News

Headlines:

- UK OBR publishes fiscal outlook and forecasts earlier than expected, before the budget

- Sterling slides back down after OBR published fiscal forecasts ahead of the budget

- UK OBR says technical error resulted in forecasts being put up too early

- UK chancellor Reeves: There will be no return to austerity

- Japan prime minister Takaichi says stimulus package isn’t reckless spending

- ECB’s de Guindos: The present interest rates level is the correct one

- Switzerland November UBS investor sentiment 12.2 vs -7.7 prior

- US MBA mortgage applications w.e. 21 November +0.2% vs -5.2% prior

- China issues plan to further promote consumption activity

Markets:

- NZD leads, JPY lags on the day

- European equities higher; S&P 500 futures up 0.2%

- US 10-year yields up 0.6 bps to 4.007%

- Gold up 0.7% to $4,158.37

- WTI crude down 0.3% to $57.79

- Bitcoin down 0.4% to $86,650

There was a lot of anticipation ahead of the UK budget but the release ended up being rather anti-climactic amid a cock up by the OBR.

The UK body made an unprecedented mess up in publishing their fiscal outlook before Rachel Reeves’ statement, with it also containing key details of the budget itself. They proceeded to blame it all on a “technical error” of course but what’s done is done.

The forecast showed that Reeves’ budget will more than double the fiscal headroom from March, roughly amounting to £22 billion. Much of that will come from tax hikes, which were to be fair expected. That said, there will be much more spending as well.

While the fiasco might have stolen much of the headlines, the market reaction is rather choppy overall. GBP/USD rose from 1.3155 to 1.3200 initially before falling back to 1.3125 as traders digested the numbers and the headlines. Will this be Reeves’ final budget? The political backlash is now something to watch out for.

10-year gilt yields also moved lower initially from 4.49% to 4.43%. But all of that reversed in the past hour with GBP/USD now coming back up to 1.3180 and 10-year yields in the UK are now at 4.49%, after having hit a high of 4.54%. Expect much more volatility in the day(s) ahead as market players continue to digest the situation.

In other markets, there wasn’t much to talk about. The dollar is trading more mixed as it holds lower against the antipodeans but lightly changed against the rest of the major currencies bloc. USD/JPY remains underpinned though, up 0.3% to 156.50 as the yen continues to struggle amid the fallout from Takaichi’s fiscal plans.

AUD/USD is up 0.4% to 0.6495, keeping near large expiries at the 0.6500 level, after a push higher earlier from hotter-than-expected Australia monthly CPI data. Meanwhile, NZD/USD is up 0.9% to 0.5673 after the RBNZ looked to have delivered their final rate cut in this cycle. The pair moved close to 0.5700 earlier but is facing rejection from the mid-November highs just below the figure level.

In the equities space, stocks continue to stay optimistic on the week with European indices holding modest gains while US futures continue to nudge a little higher as well. As for commodities, gold is also keeping higher on the day but still stuck in the recent wedge/flag pattern with the high earlier touching $4,173 but is now at $4,158 – still up 0.7% on the day though.

This article was written by Justin Low at investinglive.com.

UK chancellor Reeves: There will be no return to austerity

423908 November 26, 2025 19:45 Forexlive Latest News Market News

- OBR release of forecasts is deeply disappointing, serious error

- There will be no return to austerity

- This budget will bring down inflation

- Borrowing will fall as a share of GDP in every forecast year

- OBR forecasts show more than doubled fiscal headroom of £21.7 billion

With the details all laid out there earlier by the OBR, there’s not much for her to really say at this point. It’s just a formality of sorts in getting the message across. In terms of price action, we’re seeing continued pushing and pulling with GBP/USD now back up to 1.3160 from a low of 1.3125 earlier. 10-year gilt yields are still keeping up at 4.52% though.

This article was written by Justin Low at investinglive.com.

UK OBR says technical error resulted in forecasts being put up too early

423907 November 26, 2025 19:30 Forexlive Latest News Market News

It felt a bit weird initially when reading the headlines that some of the things felt like it should’ve been in the budget. The early release was already a cock up but leaking pretty much all the details of the budget is a screw up of a whole other level I guess. The OBR has now apologised for the incident and are of course blaming it on a “technical error” and said that “it will never happen again”. Jokes.

This article was written by Justin Low at investinglive.com.

US MBA mortgage applications w.e. 21 November +0.2% vs -5.2% prior

423906 November 26, 2025 19:14 Forexlive Latest News Market News

- Market index 317.6 vs 316.9 prior

- Purchase index 181.6 vs 168.7 prior

- Refinance index 1090.4 vs 1156.8 prior

- 30-year mortgage rate 6.40% vs 6.37% prior

This is never a market moving release. Mortgage applications are generally inversely correlated to mortgage rates.

This article was written by Giuseppe Dellamotta at investinglive.com.

UK OBR sets out forecasts for the budget, earlier than expected

423905 November 26, 2025 19:00 Forexlive Latest News Market News

That figure is up from the £9.9 billion headroom as set out in their forecast in March. As for the other details:

- Budget extends freezes of personal tax thresholds for a further 3 years from 2028-29 to 2030-31

- The freezing of personal tax and employer NICs thresholds raises £8.0 billion

- There will be a total increase in receipts by £14.9 billion on personal tax changes

- Probability of meeting current budget target is at 59% (previously 54% in March)

- 2025 GDP growth seen at 1.5% (previously 1.0%)

- 2026 GDP growth seen at 1.4% (previously 1.9%)

- 2027 GDP growth seen at 1.5%

- 2025 CPI inflation seen at 3.5% (previously 3.3%)

- 2027 CPI inflation seen at 2.0%

- Debt as a share of GDP seen at 95% this year and to end the decade at 96%

- Full document

This feels a little odd as some of these things feel like they should be part of the budget announcement itself. Markets are already of course taking to it and reacting accordingly with UK gilt yields tumbling lower while the pound spiked higher for a brief moment before settling a little bit.

10-year yields in the UK are down from 4.50% to 4.46% while GBP/USD pushed up from around 1.3155 earlier to 1.3185 currently with the high earlier touching 1.3200.

The big round numbers are what we’re looking for and they are a positive, especially the fiscal headroom indicated in the headline. So, no need for Reeves I guess? Seems like we could just call it a day unless she messes up the delivery.

This article was written by Justin Low at investinglive.com.

Deutsche Bank bumps up gold forecast for next year

423904 November 26, 2025 17:39 Forexlive Latest News Market News

In terms of where the range that they are expecting for gold, it is from $3,950 to $4,950 in 2026. On the bump higher, Deutsche cites continued central bank demand as a key reason:

“Third quarter supply-demand data supports a continued central bank bid. The positive structural picture shows inelastic demand from central banks and ETF investment diverting supply from the jewellery market. Also, overall growth in demand outpaces supply.”

Before adding that:

“Gold often exhibits a positive correlation to risk, so a deeper equity market correction would be damaging, as would our House view for less Fed easing than the market expects in 2026 (-50 bps vs -93 bps). A negotiated end to the Russia-Ukraine conflict would be a temporary negative. In the bigger picture, reserve managers could slow their pace of buying, and dramatic increases in real gold prices are often followed by significant corrections.”

With their more bullish outlook on gold prices, they also see that as having spillover effects to other precious metals as well.

“Consecutive years of undersupply enables silver, platinum, and palladium to participate more fully in gold’s strength. Elevated lease rates indicate physical scarcity which affects industrial users, many of whom prefer to lease than own. We expect supply-demand to remain in deficit for silver and platinum next year, while palladium is balanced.”

This article was written by Justin Low at investinglive.com.

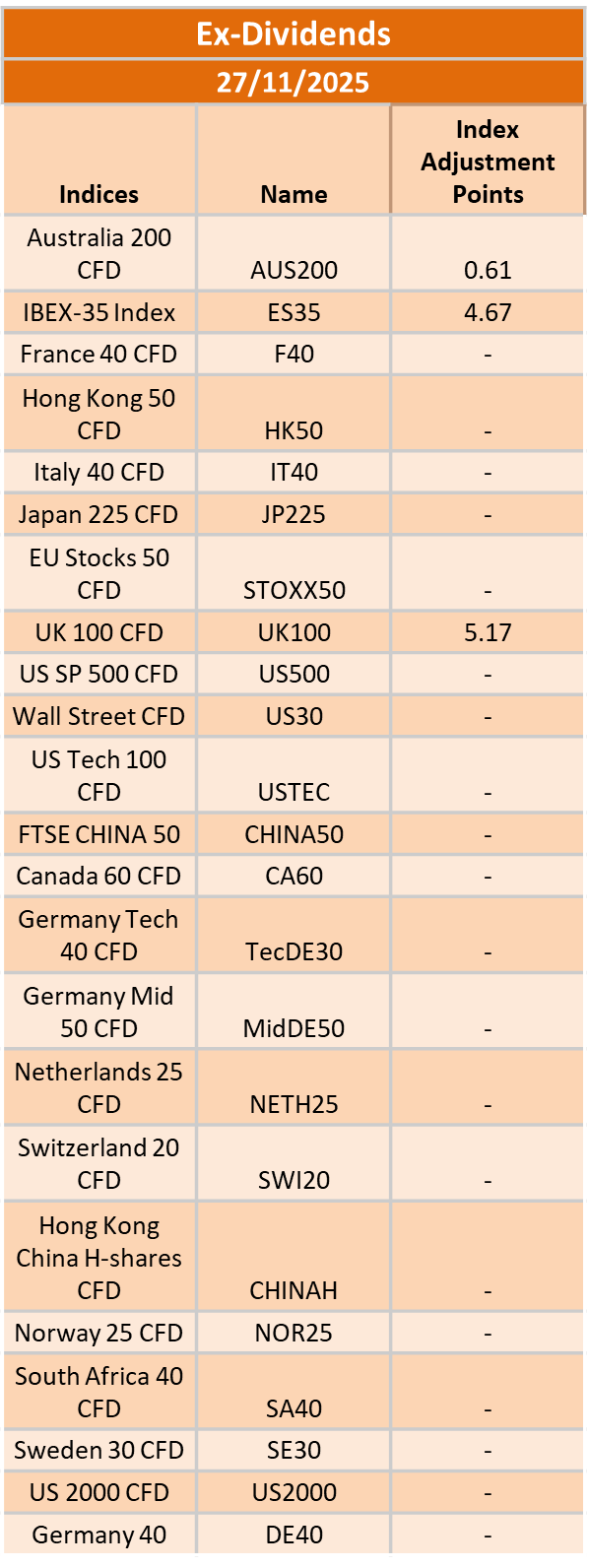

Ex-Dividend 27/11/2025

423902 November 26, 2025 17:14 ICMarkets Market News

The post Ex-Dividend 27/11/2025 first appeared on IC Markets | Official Blog.

IC Markets Global – Asia Fundamental Forecast | 26 November 2025

423901 November 26, 2025 16:39 ICMarkets Market News

IC Markets Global – Asia Fundamental Forecast | 26 November 2025

What happened in the U.S. session?

During the U.S. session overnight, a significant rally in U.S. stock indices driven by renewed expectations of a Federal Reserve rate cut in December, supported by comments from Fed officials about rising labor market risks and a more accommodative policy stance. Major macroeconomic data releases included retail sales, producer price data for September, consumer confidence for November, and home price indices, with delayed releases due to the recent government shutdown.

What does it mean for the Asia Session?

RBNZ delivering a more hawkish message than expected could spark volatility in Antipodean currencies. Australia’s new monthly CPI format introduces uncertainty around data quality and interpretation. UK budget execution risk remains high given the fiscal constraints. The absence of US GDP data removes a key anchor for market expectations. Continued Fed dovish repricing supports risk assets and Asian equities. China property stimulus speculation could lift sentiment for property developers and domestically-focused stocks.

The Dollar Index (DXY)

Key news events today

Unemployment Claims (1:30 pm GMT)

Core Durable Goods Orders m/m (1:30 pm GMT)

Durable Goods Orders m/m (1:30 pm GMT)

CB Consumer Confidence (Tentative)

What can we expect from DXY today?

The US Dollar faces a pivotal trading day with the Dollar Index (DXY) hovering near the 100 level amid heightened expectations of a Federal Reserve rate cut in December. Key drivers include dovish Fed signals, important economic data releases (jobless claims, durable goods orders), and significant global events, including the RBNZ rate decision, UK Autumn Budget, and ECB Financial Stability Review. Markets are pricing approximately 75-81% probability of a 25 basis point rate cut at the December FOMC meeting, up sharply from around 42% just a week ago.

Central Bank Notes:

- The Federal Open Market Committee (FOMC) voted, by majority, to lower the federal funds rate target range by 25 basis points to 3.75% — 4.00% at its October 28–29, 2025, meeting, marking the second consecutive cut following the 25 basis points reduction in September.

- The Committee maintained its long-term objectives of maximum employment and 2% inflation, noting that the labor market continues to soften, with modest job creation and an unemployment rate edging higher. In comparison, inflation remains above target at around 3.0%.

- Policymakers highlighted ongoing downside risks to economic growth, tempered by signs of resilient economic activity. September’s consumer price index (CPI) came in slightly below expectations at 3.0% year-over-year, easing inflationary pressure but still warranting vigilance amid tariff-driven price effects.

- Economic activity expanded modestly in the third quarter, with GDP growth estimates around 1.0% annualized; however, uncertainty remains elevated amid persistent global trade tensions and the U.S. government shutdown, which is impacting data availability.

- The updated Summary of Economic Projections anticipates an unemployment rate averaging approximately 4.5% for 2025, with headline and core personal consumption expenditures (PCE) inflation projections remaining near 3.0%, indicating a slow easing path ahead.

- The Committee emphasized its flexible, data-dependent approach and underscored that future policy adjustments will be guided by incoming labor market and inflation data. As in prior meetings, there was dissent, including one member advocating a more aggressive 50-basis-point cut.

- The FOMC announced the planned conclusion of its balance sheet reduction (quantitative tightening) program, intending to cease runoff in the near term to maintain market stability. Treasury redemption caps will remain steady at $5 billion per month, and agency mortgage-backed securities caps will remain at $35 billion.

- The next meeting is scheduled for 9 to 10 December 2025.

Next 24 Hours Bias

Medium Bullish

Gold (XAU)

Key news events today

Unemployment Claims (1:30 pm GMT)

Core Durable Goods Orders m/m (1:30 pm GMT)

Durable Goods Orders m/m (1:30 pm GMT)

CB Consumer Confidence (Tentative)

What can we expect from Gold today?

Gold is expected to range trade between $4,000 and $4,160-$4,200 in the near term, with the December Fed rate cut probability remaining the primary directional driver. A break above $4,200 with momentum could see gold retest October highs, while weak data surprising to the upside or hawkish Fed rhetoric could push prices toward the $3,950-$4,000 support zone. The combination of Wednesday’s data releases, Thanksgiving liquidity reduction, and ongoing geopolitical developments creates a potentially volatile environment for precious metals traders heading into month-end.

Next 24 Hours Bias

Medium Bearish

The Australian Dollar (AUD)

Key news events today

CPI y/y (12:30 am GMT)

What can we expect from AUD today?

The Australian dollar faces a pivotal session with the inaugural complete monthly CPI release taking center stage. A reading at or above 3.6% would reinforce expectations that the RBA will maintain its cautious, hold-steady approach, providing modest support for the currency. Conversely, a softer inflation print could revive rate cut speculation and push AUD/USD toward the lower end of its range near 0.6400. Traders should also monitor the RBNZ decision and US economic data for secondary catalysts throughout the session.

Central Bank Notes:

- The Reserve Bank of Australia held its cash rate steady at 3.60% at the November policy meeting, citing persistent inflationary pressures and lingering uncertainties in both domestic and global outlooks. This is the third consecutive pause following the cut in August.

- Policymakers remain alert to renewed inflation momentum. After a temporary uptick in September’s CPI, trimmed mean inflation for Q3 stands at 3.0%, above the intended 2–3% band. The RBA now anticipates that core inflation will stay above target until at least mid-2026, delaying any hopes of further easing.

- Headline CPI climbed by 3.2% in the year to September 2025, driven by resilient housing (+2.5%) and insurance costs, while discretionary goods inflation is subdued. The transition to monthly CPI reporting from November will improve the accuracy of inflation tracking.

- Domestic demand remains firm, particularly in services and housing, while manufacturing and discretionary retail continue to lag. Household incomes have stabilized, but high borrowing costs and elevated rents are constraining consumption and risking a slowdown in Q1 2026.

- Labor market tightness persists, though job growth has moderated. Underutilization edged higher. Wage growth is plateauing, but weak productivity is keeping unit labor costs elevated—a medium-term risk that remains central to the Board’s narrative.

- The RBA highlights geopolitical tensions and volatile commodity markets as primary global risks, against a backdrop of modest upward revisions to world growth forecasts. The Board stresses that its stance remains “cautious and data-dependent,” with ongoing vigilance on inflation, labor, and spending trends.

- Monetary policy remains mildly restrictive, balancing progress on price stability against vulnerabilities in household demand and global outlook. Board communications reaffirm a dual mandate: price stability and full employment, while underscoring readiness to respond should risks materialize sharply.

- Analysts generally expect the cash rate to remain at current levels through early 2026, with only modest cuts possible later in the year if inflation moderates. The new monthly CPI release (first full edition Nov 2025) will be watched closely for timely signals on price trends.

- The next meeting is on 9 December 2025.

Next 24 Hours Bias

Medium Bearish

The Kiwi Dollar (NZD)

Key news events today

Official Cash Rate (1:00 am GMT)

RBNZ Monetary Policy Statement (1:00 am GMT)

RBNZ Rate Statement (1:00 am GMT)

RBNZ Press Conference (2:00 am GMT)

RBNZ Gov Hawkesby Speaks (8:10 pm GMT)

Retail Sales q/q (9:45 pm GMT)

What can we expect from NZD today?

Wednesday represents a pivotal moment for New Zealand’s monetary policy landscape. The widely expected 25 basis point rate cut to 2.25% will cap an unprecedented easing cycle that has delivered 325 basis points of cuts since August 2024. The decision comes as the New Zealand economy struggles with weak growth, elevated unemployment, and persistent inflation near the top of the target band.

The New Zealand dollar remains under pressure near seven-month lows around 0.5610, weighed down by aggressive RBNZ easing, monetary policy divergence with the US Federal Reserve, and broader global risk sentiment favoring the USD.

Central Bank Notes:

- The Monetary Policy Committee (MPC) left the Official Cash Rate (OCR) unchanged at 2.25% at its 26 November 2025 meeting, following the widely anticipated 25-basis-point reduction from 2.50%, and signaled that policy is now firmly in stimulatory territory while keeping the option of further easing on the table if needed.

- The decision was again reached by consensus, with members judging that the cumulative 325 basis points of easing over the past year warranted a period of assessment, even as several emphasized a willingness to cut further should incoming data point to a more protracted downturn or renewed disinflationary pressures.

- Headline consumer price inflation is projected to hover near 3% in late 2025 before gradually easing toward the 2% midpoint of the 1–3% target band through 2026, supported by contained inflation expectations around 2.3% over the two-year horizon and an expected pickup in spare capacity.

- The MPC noted that domestic demand remains subdued but shows tentative signs of stabilisation, with softer household spending and construction only partially offset by improving services activity; nevertheless, policymakers still expect services inflation to ease as wage growth moderates and the labour market loosens further over the coming year.

- Financial conditions continue to ease as wholesale and retail borrowing rates reprice to the lower OCR, contributing to gradually rising mortgage approvals and improving housing-related sentiment, although broader business credit growth remains patchy and sensitive to uncertainty about the durability of the recovery.

- Recent data confirm that GDP momentum is weak but not deteriorating as sharply as earlier in 2025, with high-frequency indicators pointing to a shallow recovery from a low base and ongoing headwinds from elevated living costs and fragile confidence weighing on discretionary consumption and investment.

- The MPC reiterated that external risks remain skewed to the downside, particularly from softer Chinese demand and uncertainty around United States trade policy, but noted that a lower New Zealand dollar continues to provide some offset via improved export competitiveness and support for tradables inflation.

- Looking ahead to early 2026, the Committee maintained a mild easing bias, indicating that a further cut toward 2.00–2.10% cannot be ruled out if activity fails to gain traction or if inflation undershoots projections, but current forecasts envisage the OCR remaining near 2.25% for an extended period provided inflation converges toward target and the recovery proceeds broadly as expected.

- The next meeting is on 18 February 2026.

Next 24 Hours Bias

Medium Bearish

The Japanese Yen (JPY)

Key news events today

No major news events

What can we expect from JPY today?

The Japanese yen enters Wednesday at a critical juncture, trading around 156 per dollar after recovering slightly from 10-month lows. The currency faces conflicting pressures: downward pressure from PM Takaichi’s ¥21.3 trillion stimulus package and fiscal concerns, but upward support from intensifying intervention warnings and rising expectations for a December BoJ rate hike. Traders are positioning cautiously ahead of Tokyo CPI data on Thursday and watching the 158-160 zone as the likely intervention trigger.

Central Bank Notes:

- The Policy Board of the Bank of Japan met on 30–31 October and, by a clear majority vote, decided to maintain its key monetary policy approach for the upcoming period.

- The BOJ will continue to encourage the uncollateralized overnight call rate to remain at around 0.5%, in line with the prior stance.

- The gradual quarterly reduction in monthly outright purchases of Japanese Government Bonds (JGBs) remains intact, with amounts unchanged from the previous schedule. Purchases are set to decrease by about ¥400 billion per quarter through March 2026, shifting to about ¥200 billion per quarter from April to June 2026, and targeting a ¥2 trillion purchase level for Q1 2027. The bank reaffirmed its intention to maintain flexibility, with readiness to respond if market conditions warrant an adjustment.

- Japan’s economy continues to show moderate recovery, primarily led by solid capital expenditures, although export growth and corporate activity remain restrained by external demand uncertainty and the ongoing effects of U.S. trade policies.

- Annual headline inflation (excluding fresh food) accelerated to 2.9% year-on-year in September, marking the first uptick in four months and staying above the BOJ’s 2% target. Broad-based inflation persists, with food and energy cost pressures, but wage growth continues to support household consumption. Input cost pressures from the earlier surge in imports eased slightly.

- Short-term inflation momentum could moderate as food-price hikes ease, though rent, healthcare, and service-sector price increases tied to labor shortages provide support. Firms and households maintain a gradual upward drift in inflation expectations.

- For the near term, BOJ projects growth below trend as external demand stays subdued and corporate investment plans remain cautious. Still, accommodative financial conditions and steady gains in real labor income will underpin domestic consumption.

- Over the medium term, as overseas economies recover and trade conditions normalize, Japan’s growth potential should improve. Persistent labor market tightness, higher wage settlements, and rising medium- to long-term inflation expectations are expected to keep core inflation on a gradual upward trajectory, converging toward the 2% price stability target later in the forecast horizon.

- The next meeting is scheduled for 18 to 19 December 2025.

Next 24 Hours Bias

Weak Bearish

Oil

Key news events today

EIA Crude Oil Inventories ( 2:30 pm GMT)

What can we expect from Oil today?

Crude oil prices have experienced significant downward pressure as markets head into Wednesday. WTI crude settled at approximately $57.72 per barrel while Brent crude dropped to around $62.15 per barrel on Tuesday, representing notable declines of 1.9% and 1.9% respectively. This marks oil’s lowest levels in approximately five weeks, with WTI down over 14% year-to-date and Brent falling roughly 12.5% from year-ago levels.

Next 24 Hours Bias

Medium Bearish

The post IC Markets Global – Asia Fundamental Forecast | 26 November 2025 first appeared on IC Markets | Official Blog.

General Market Analysis – 26/11/25

423900 November 26, 2025 16:39 ICMarkets Market News

US Stocks Push Higher Again on Rate Cut Hopes – Dow up 1.4%

US stock indices pushed higher again overnight, marking a third consecutive day of gains as Fed rate-cut expectations continued to firm. The Dow led the move with a strong 1.43% rise to finish at 47,112, the S&P 500 gained 0.91%, closing at 6,765, while the Nasdaq added 0.67% to end the session at 23,025. The improving risk sentiment saw Treasury yields ease back further, with the 2-year yield falling 2.7 basis points to 3.45% and the 10-year slipping 3.1 basis points to close at 3.994%, comfortably below the key 4% level. The US dollar also weakened against the majors, the DXY falling 0.34% to 99.80. In commodities, oil prices extended their decline, with Brent dropping 1.20% to settle at $62.61 and WTI sliding 1.26% to $58.10, as optimism around potential progress in resolving the Russia–Ukraine conflict continued to weigh on prices. Gold eased slightly, dipping 0.14% to trade at $4,130.01 as it remained confined within its recent range.

Dollar Plays Catch Up with Fed Rates and Yields

The dollar at last played a bit of catch-up with both Fed rate-cut expectations and bond yields in trading yesterday as it fell against the majors, dropping just over 0.3% on the day. While estimates for a Fed rate cut have jumped from below 40% to above 85% in the last week, and the 10-year yield has dropped from well above 4.10% to under 4%, the dollar had remained resolutely strong, but yesterday’s trading saw the first dip against the majors. Traders are expecting more volatility in the sessions ahead today, with more data from the US due and Thanksgiving holiday trading conditions looming. However, some feel that the huge move in expectations may be overdone, with little really changed on the fundamentals except some updates from Fed officials, and that the FX market may be right to keep the greenback at relatively high levels.

Hectic Day on the Macroeconomic Calendar

It is shaping up to be a particularly busy session across global markets today, with key economic data, central bank decisions, and fiscal updates scheduled throughout the day. There is a heavy focus on antipodean markets in the Asian session today, with Australian CPI data (exp. +3.6% y/y) due out shortly before the Reserve Bank of New Zealand announces its latest rate call, where it is firmly expected to cut by 25 basis points. The London session will see the initial focus on the continent, with the ECB Stability Report due out early in the piece, before focus jumps across the channel to the UK for HM Treasury’s Autumn Forecast Statement. The New York session sees more data crammed in ahead of the Thanksgiving Day holiday, with the weekly unemployment claims numbers (exp. 226k), durable goods data (exp. +0.2% m/m, core +0.5% m/m), and Chicago update (exp. 43.9) all set for release. There were some rumours earlier in the week that we may see a delayed Core PCE Price Index release today, but that has failed to materialize.

The post General Market Analysis – 26/11/25 first appeared on IC Markets | Official Blog.