Articles

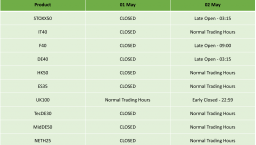

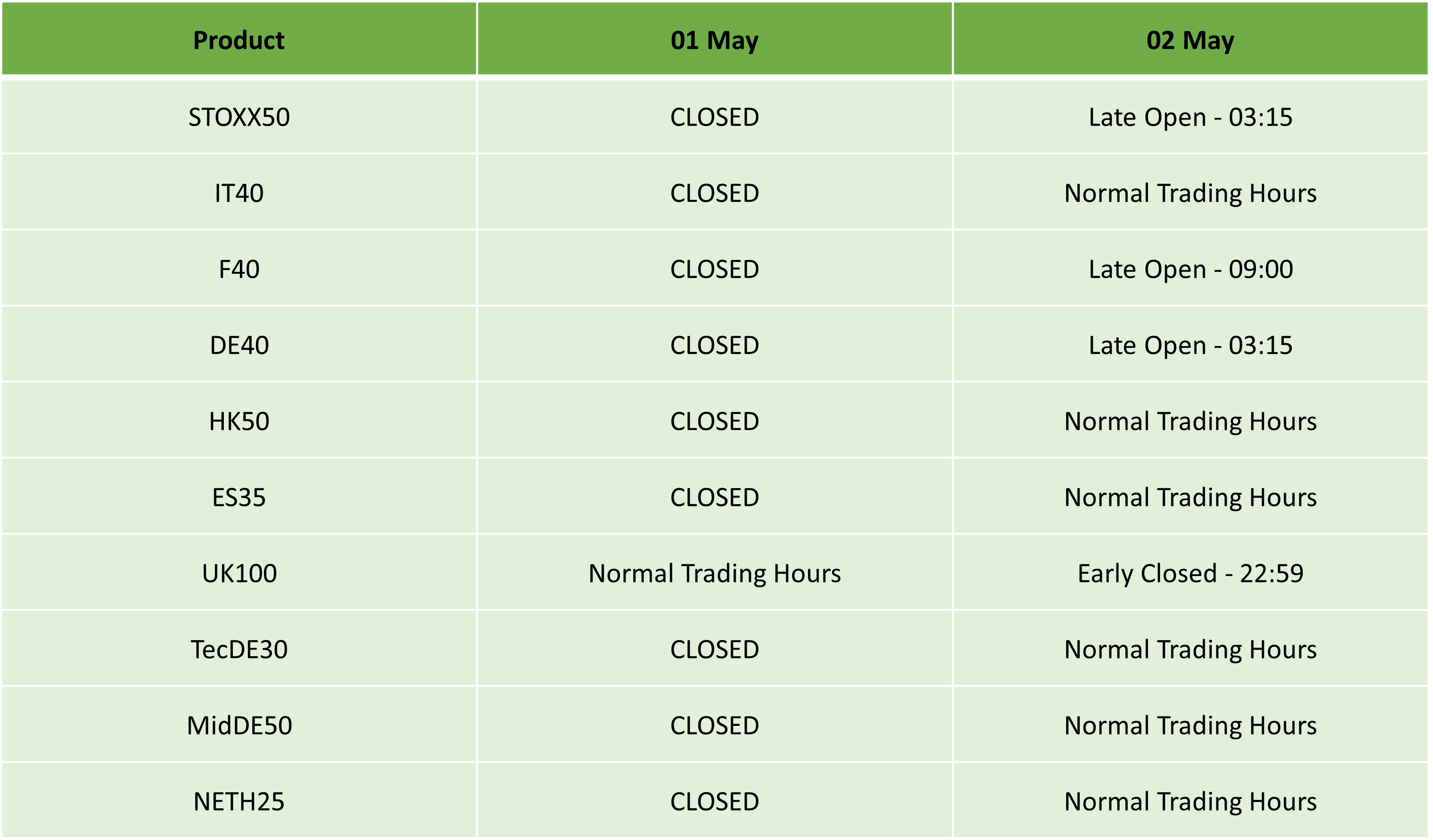

Labour Day Holiday Trading Schedule 2025

415709 April 29, 2025 14:00 ICMarkets Market News

Dear Client,

Please find our updated Trading schedule and general information related to the Labour Day Holiday on Thursday, 01 May, 2025.

Liquidity over the holidays is expected to be particularly thin so please take the necessary precaution to ensure that you are not affected by increased volatility, spreads and intermittent pricing.

All times mentioned below are Platform time (GMT +3).

Kind regards,

IC Markets Global.

The post Labour Day Holiday Trading Schedule 2025 first appeared on IC Markets | Official Blog.

Victoria Day Holiday Trading Schedule 2025

415707 April 29, 2025 13:39 ICMarkets Market News

Dear Client,

Please find our updated Trading schedule and general information related to the Victoria Day on Monday, 19 May, 2025.

Liquidity over the holidays is expected to be particularly thin so please take the necessary precaution to ensure that you are not affected by increased volatility, spreads and intermittent pricing.

All times mentioned below are Platform time (GMT +3).

Kind regards,

IC Markets Global.

The post Victoria Day Holiday Trading Schedule 2025 first appeared on IC Markets | Official Blog.

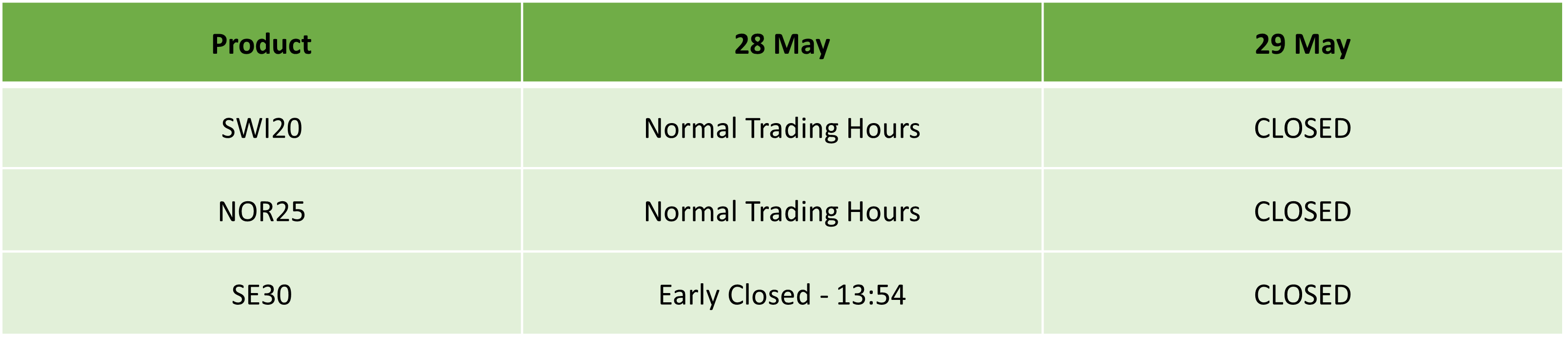

Ascension Day Holiday Trading Schedule – 2025

415705 April 29, 2025 13:39 ICMarkets Market News

Dear Client,

Please find our updated Trading schedule and general information related to the Ascension Day on Thursday, 29 May, 2025.

Liquidity over the holidays is expected to be particularly thin so please take the necessary precaution to ensure that you are not affected by increased volatility, spreads and intermittent pricing.

All times mentioned below are Platform time (GMT +3).

Kind regards,

IC Markets Global.

The post Ascension Day Holiday Trading Schedule – 2025 first appeared on IC Markets | Official Blog.

Germany May GfK consumer sentiment -20.6 vs -26.0 expected

415704 April 29, 2025 13:14 Forexlive Latest News Market News

- Prior -24.5; revised to -24.3

That’s a decent improvement but GfK warns that tariffs uncertainty is still very much weighing on the broader outlook. So, that will be a bigger factor to consider in the months ahead.

This article was written by Justin Low at www.forexlive.com.

Will sit down with Trump to discuss future ties as two sovereign nations – Carney

415703 April 29, 2025 13:00 Forexlive Latest News Market News

No time to rest on his laurels. He will be under a lot of scrutiny to see how he handles the ongoing situation with the US. That especially after getting Trump, or should I say the anti-Trump rhetoric, helped to turn their fortunes around. So, first thing’s first Carney is saying that he will be sitting down with Trump to discuss future economic and security ties between the two sovereign nations. A bit of emphasis on the ending there.

This article was written by Justin Low at www.forexlive.com.

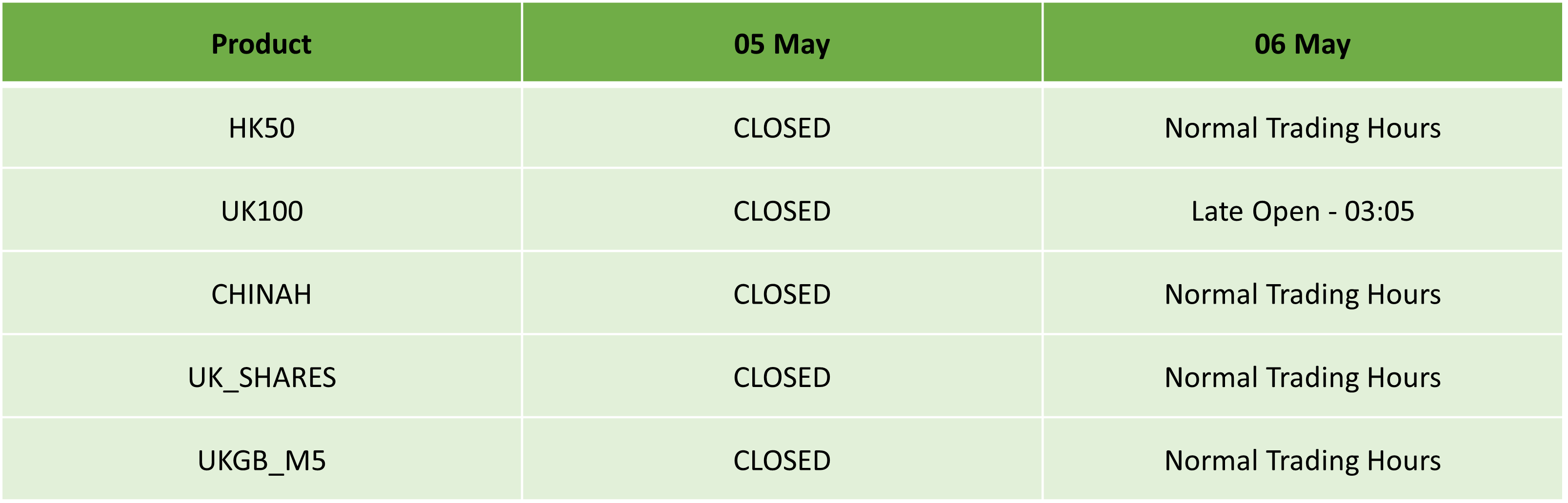

May Bank Holiday Trading Schedule 2025

415701 April 29, 2025 13:00 ICMarkets Market News

Dear Client,

Please find our updated Trading schedule and general information related to the May Bank Holiday on Monday, 05 May, 2025.

Liquidity over the holidays is expected to be particularly thin so please take the necessary precaution to ensure that you are not affected by increased volatility, spreads and intermittent pricing.

All times mentioned below are Platform time (GMT +3).

Kind regards,

IC Markets Global.

The post May Bank Holiday Trading Schedule 2025 first appeared on IC Markets | Official Blog.

General Market Analysis – 29/04/25

415700 April 29, 2025 11:39 ICMarkets Market News

US Stocks Quiet Ahead of a Big Week – Dow up 0.25%

The three major US stock indices all closed near flat in trading yesterday as investors looked ahead to key economic data updates and earnings reports later this week. The Dow added 0.28%, the S&P edged 0.06% higher, while the Nasdaq drifted 0.10% lower. There was some more volatility across other financial products; the dollar and Treasury yields took a hit as tariff concerns continued to weigh on sentiment. The DXY fell 0.69% to 98.92, while the 2-year Treasury yield dropped 5.5 basis points to 3.693%, and the 10-year fell 2.7 basis points to 4.208%. Oil prices tanked on demand concerns, with Brent off 1.72% to $66.72 and WTI down 1.76% to $61.91 a barrel, whilst gold found good buying interest to move back towards recent highs, up 0.47% to $3,342.60 an ounce.

Oil to Remain Under Pressure

Oil prices, alongside most financial products, have been volatile over the last few months and particularly over the last few weeks after Trump’s ‘Liberation Day’, and traders are expecting to see volatility remain higher in the medium term even if we see a calming in other products. We have seen a good drop in oil prices in the last few months, and it does feel like forces are aligning to keep ‘black gold’ under pressure in the medium term. Certainly, tariff implementation and further threats have influenced global growth concerns, and oil is always one of the first to take a hit in those circumstances, but it is also under pressure from the supply side, with OPEC+ countries expecting a pickup in production increases in the next few months. We have seen over 30% wiped off the value of WTI since the start of the year, and unless we see some serious changes in overall market sentiment, expect it to remain under pressure for the foreseeable future.

Economic Calendar Picks Up Today

The global economic calendar starts to pick up today and then speeds up over the next few days, culminating in the key Non-Farms data on Friday. The Asian session is set to be fairly quiet today with little on the event calendar, and despite federal election results coming through from Canada in the session, the loonie is expected – and so far, has been – relatively quiet. It is also relatively quiet in the London session today, although euro traders will keep a close eye on Spanish Flash CPI data (exp. +2.0%) early in the day. Things should start to get interesting on the New York open though, with the first of four major US jobs updates due out early in the session in the form of the JOLTS Job Openings data (exp. 7.48mio). This is released alongside the CB Consumer Confidence data (exp. 87.4), with investors expected to monitor both closely for tariff influences.

The post General Market Analysis – 29/04/25 first appeared on IC Markets | Official Blog.

Tuesday 29th April 2025: Technical Outlook and Review

415699 April 29, 2025 11:14 ICMarkets Market News

DXY (US Dollar Index):

Potential Direction: Bearish

Overall momentum of the chart: Bearish

Price could rise toward the pivot and potentially make a bearish reversal off this level to fall toward the 1st support.

Pivot: 100.27

Supporting reasons: Identified as an overlap resistance that aligns close to a 38.2% Fibonacci retracement, indicating a potential area where selling pressures could intensify.

1st support: 98.56

Supporting reasons: Identified as a pullback support that aligns close to the 61.8% Fibonacci retracement, indicating a potential area where the price could stabilize once again.

1st resistance: 101.38

Supporting reasons: Identified as a pullback resistance that aligns with the 61.8% Fibonacci retracement, indicating a potential level that could cap further upward movement.

EUR/USD:

Potential Direction: Bearish

Overall momentum of the chart: Bullish

Price could potentially make a bearish continuation toward the 1st support.

Pivot: 1.1427

Supporting reasons: Identified as an overlap resistance, indicating a potential area where selling pressures could intensify.

1st support: 1.1147

Supporting reasons: Identified as a pullback support that aligns with the 61.8% Fibonacci retracement, indicating a potential area where the price could stabilize once more.

1st resistance: 1.1567

Supporting reasons: Identified as a swing-high resistance, indicating a potential area that could halt any further upward movement.

EUR/JPY:

Potential Direction: Bearish

Overall momentum of the chart: Neutral

Price could rise toward the pivot and potentially make a bearish reversal off this level to fall toward the 1st support.

Pivot: 164.10

Supporting reasons: Identified as an overlap resistance that aligns close to the 61.8% Fibonacci projection, indicating a potential area where selling pressures could intensify.

1st support: 160.38

Supporting reasons: Identified as an overlap support, indicating a potential area where the price could stabilize once again.

1st resistance: 166.59

Supporting reasons: Identified as a swing-high resistance that aligns close to the 100% Fibonacci projection, indicating a potential area that could halt any further upward movement.

EUR/GBP:

Potential Direction: Bullish

Overall momentum of the chart: Bullish

Price could fall toward the pivot and potentially make a bullish bounce off this level to rise toward the 1st resistance.

Pivot: 0.8446

Supporting reasons: Identified as a pullback support, indicating a potential area where buying interests could pick up to stage a rebound.

1st support: 0.8377

Supporting reasons: Identified as a pullback support, indicating a potential area where the price could stabilize once more.

1st resistance: 0.8519

Supporting reasons: Identified as a pullback resistance, indicating a potential level that could cap further upward movement.

GBP/USD:

Potential Direction: Bearish

Overall momentum of the chart: Bullish

Price could potentially make a bearish continuation toward the 1st support.

Pivot: 1.3425

Supporting reasons: Identified as an overlap resistance, indicating a potential area where selling pressures could intensify.

1st support: 1.3206

Supporting reasons: Identified as an overlap support, acting as a potential level where the price could stabilize once again.

1st resistance: 1.3543

Supporting reasons: Identified as a resistance that aligns with the 161.8% Fibonacci extension, indicating a potential level that could cap further upward movement.

GBP/JPY:

Potential Direction: Bearish

Overall momentum of the chart: Bearish

Price could make a bearish continuation toward the 1st support.

Pivot: 191.73

Supporting reasons: Identified as an overlap resistance that aligns close to the 61.8% Fibonacci retracement and the 78.6% Fibonacci projection, indicating a potential area where selling pressures could intensify.

1st support: 189.52

Supporting reasons: Identified as an overlap support, indicating a potential level where the price could stabilize once more.

1st resistance: 193.73

Supporting reasons: Identified as a pullback resistance that aligns close to the 78.6% Fibonacci retracement, indicating a potential level that could cap further upward movement.

USD/CHF:

Potential Direction: Bullish

Overall momentum of the chart: Bearish

Price could potentially make a bullish bounce off this level to rise toward the 1st resistance.

Pivot: 0.8195

Supporting reasons: Identified as an overlap support, indicating a potential area where buying interests could pick up to stage a rebound.

1st support: 0.8046

Supporting reasons: Identified as a swing low support, indicating a potential level where the price could stabilize once again.

1st resistance: 0.8372

Supporting reasons: Identified as a pullback resistance that aligns with the 61.8% Fibonacci retracement, indicating a potential level that could cap further upward movement.

USD/JPY:

Potential Direction: Bullish

Overall momentum of the chart: Bearish

Price could potentially make a bullish bounce off this level to rise toward the 1st resistance.

Pivot: 141.81

Supporting reasons: Identified as a pullback support, indicating a potential area where buying interests could pick up to stage a rebound.

1st support: 140.14

Supporting reasons: Identified as a swing-low support, suggesting a potential area where the price could stabilize once more.

1st resistance: 144.38

Supporting reasons: Identified as an overlap resistance that aligns close to the 50% Fibonacci retracement and the 61.8% Fibonacci projection, indicating a potential level that could cap further upward movement.

USD/CAD:

Potential Direction: Bearish

Overall momentum of the chart: Bearish

Price could rise toward the pivot and potentially make a bearish reversal off this level to fall toward the 1st support.

Pivot: 1.3894

Supporting reasons: Identified as a multi-swing-high resistance that aligns close to a 23.6% Fibonacci retracement, indicating a potential area where selling pressures could intensify. The presence of the red Ichimoku Cloud adds further significance to the strength of the bearish momentum.

1st support: 1.3794

Supporting reasons: Identified as a multi-swing-low support, indicating a key level where the price could stabilize once more.

1st resistance: 1.3974

Supporting reasons: Identified as a swing-high resistance that aligns close to a 38.2% Fibonacci retracement, indicating a potential area that could halt any further upward movement.

AUD/USD:

Potential Direction: Bearish

Overall momentum of the chart: Bullish

Price could rise toward the pivot and potentially make a bearish reversal off this level to pull back toward the 1st support.

Pivot: 0.6459

Supporting reasons: Identified as a swing-high resistance, indicating a potential area where selling pressures could intensify.

1st support: 0.6379

Supporting reasons: Identified as a multi-swing-low support, suggesting a potential area where the price could stabilize once again. The presence of the green Ichimoku Cloud adds further significance to the strength of the bullish momentum.

1st resistance: 0.6523

Supporting reasons: Identified as a swing-high resistance that aligns close to a 127.2% Fibonacci extension, indicating a potential area that could halt any further upward movement.

NZD/USD

Potential Direction: Bullish

Overall momentum of the chart: Bullish

Price has made a bullish bounce off the pivot and could potentially rise toward the 1st resistance.

Pivot: 0.5938

Supporting reasons: Identified as a multi-swing-low support, indicating a potential area where buying interests could pick up to resume the uptrend. The presence of the green Ichimoku Cloud adds further significance to the strength of the bullish momentum.

1st support: 0.5887

Supporting reasons: Identified as an overlap support that aligns close to a 23.6% Fibonacci retracement, suggesting a potential area where the price could stabilize once more.

1st resistance: 0.6019

Supporting reasons: Identified as a swing-high resistance, indicating a potential area that could halt any further upward movement.

US30 (DJIA):

Potential Direction: Bearish

Overall momentum of the chart: Neutral

Price could rise toward the pivot and potentially make a bearish reversal off this level to fall toward the 1st support.

Pivot: 40,819.80

Supporting reasons: Identified as a multi-swing-high resistance that aligns close to a 50% Fibonacci retracement, indicating a potential area where selling pressures could intensify.

1st support: 37,844.90

Supporting reasons: Identified as a swing-low support, indicating a potential level where the price could stabilize once again.

1st resistance: 42,740.30

Supporting reasons: Identified as a swing-high resistance, indicating a potential area that could halt any further upward movement.

DE40 (DAX):

Potential Direction: Bearish

Overall momentum of the chart: Bullish

Price could rise toward the pivot and potentially make a bearish reversal off this level to pull back toward the 1st support.

Pivot: 22,521.00

Supporting reasons: Identified as a swing-high resistance that aligns close to a 78.6% Fibonacci retracement, indicating a potential area where selling pressures could intensify.

1st support: 21,523.30

Supporting reasons: Identified as a pullback support that aligns close to a 23.6% Fibonacci retracement, indicating a key level where the price could stabilize once more.

1st resistance: 23,438.30

Supporting reasons: Identified as a multi-swing-high resistance, indicating a potential area that could halt any further upward movement.

US500 (S&P 500):

Potential Direction: Bullish

Overall momentum of the chart: Neutral

Price could fall toward the pivot and potentially make a bullish bounce off this level to rise toward the 1st resistance.

Pivot: 5,480.90

Supporting reasons: Identified as an overlap support, indicating a potential area where buying interests could pick up to resume the uptrend. The presence of the green Ichimoku Cloud adds further significance to the strength of the bullish momentum.

1st support: 5,101.40

Supporting reasons: Identified as a swing-low support, indicating a potential level where the price could stabilize once again.

1st resistance: 5,785.00

Supporting reasons: Identified as a swing-high resistance, indicating a potential area that could halt any further upward movement.

BTC/USD (Bitcoin):

Potential Direction: Bearish

Overall momentum of the chart: Bullish

Price could rise toward the pivot and potentially make a bearish reversal off this level to pull back toward the 1st support.

Pivot: 95,364.14

Supporting reasons: Identified as an overlap resistance, indicating a potential area where selling pressures could intensify.

1st support: 92,463.38

Supporting reasons: Identified as an overlap support, indicating a potential level where the price could stabilize once more. The presence of the green Ichimoku Cloud adds further significance to the strength of the bullish momentum.

1st resistance: 99,293.10

Supporting reasons: Identified as a swing-high resistance, indicating a potential area that could halt any further upward movement.

ETH/USD (Ethereum):

Potential Direction: Bearish

Overall momentum of the chart: Neutral

Price could rise toward the pivot and potentially make a bearish reversal off this level to fall toward the 1st support.

Pivot: 1,828.47

Supporting reasons: Identified as a multi-swing-high resistance that aligns with a 61.8% Fibonacci retracement, indicating a potential area where selling pressures could intensify.

1st support: 1,669.20

Supporting reasons: Identified as a pullback support indicating a potential level where the price could stabilize once again.

1st resistance: 1,947.17

Supporting reasons: Identified as an overlap resistance that aligns with a 78.6% Fibonacci retracement, indicating a potential area that could halt any further upward movement.

WTI/USD (Oil):

Potential Direction: Bullish

Overall momentum of the chart: Neutral

Price could fall toward the pivot and potentially make a bullish bounce off this level to rise toward the 1st resistance.

Pivot: 58.85

Supporting reasons: Identified as a swing-low support that aligns close to a 61.8% Fibonacci retracement, indicating a potential area where buying interests could pick up to stage a minor rebound.

1st support: 55.83

Supporting reasons: Identified as a swing-low support, indicating a key level where the price could stabilize once more.

1st resistance: 64.55

Supporting reasons: Identified as a swing-high resistance, indicating a potential area that could halt any further upward movement.

XAU/USD (GOLD):

Potential Direction: Bearish

Overall momentum of the chart: Bullish

Price could potentially make a bearish continuation toward the 1st support.

Pivot: 3349.51

Supporting reasons: Identified as an overlap resistance, indicating a potential area where selling pressures could intensify

1st support: 3240.37

Supporting reasons: Identified as a pullback support that aligns with the 50% Fibonacci retracement, acting as a potential level where price could stabilize once again.

1st resistance: 3492.38

Supporting reasons: Identified as a swing resistance, indicating a potential area that could halt any further upward movement.

The accuracy, completeness and timeliness of the information contained on this site cannot be guaranteed. IC Markets does not warranty, guarantee or make any representations, or assume any liability regarding financial results based on the use of the information in the site.

News, views, opinions, recommendations and other information obtained from sources outside of www.icmarkets.com, used in this site are believed to be reliable, but we cannot guarantee their accuracy or completeness. All such information is subject to change at any time without notice. IC Markets assumes no responsibility for the content of any linked site.

The fact that such links may exist does not indicate approval or endorsement of any material contained on any linked site. IC Markets is not liable for any harm caused by the transmission, through accessing the services or information on this site, of a computer virus, or other computer code or programming device that might be used to access, delete, damage, disable, disrupt or otherwise impede in any manner, the operation of the site or of any user’s software, hardware, data or property.

The post Tuesday 29th April 2025: Technical Outlook and Review first appeared on IC Markets | Official Blog.

ForexLive Asia-Pacific FX news wrap: Canada election result tight, CAD yo-yo

415698 April 29, 2025 11:00 Forexlive Latest News Market News

*

- There is one Canadian election outcome that could hurt the loonie … and here it comes

- CAD sliding further now after projections show a minority Carney government is likely

*

- Hidden damage: Trump tariffs threaten bigger blow to China’s economy, Nomura warns

- CTV projects Carney’s Liberals will form a minority government

- More on China for min urging defiance of Trump tariff bullying

- Canadian dollar gaining ground as Carney wins election

- CTV says Carney has won the election – too early to say if majority or minority though

- Big bounce in odds for a Liberal majority in Canada

- Barclays on plans by Japan’s largest four life insurers to reduce JGB holdings

- PBOC sets USD/ CNY central rate at 7.2029 (vs. estimate at 7.2781)

- Barclays says US credit spreads likely to widen in the coming six months

- Canadian election, early results trickling in

- Goldman Sachs says Trump tariffs could endanger 16 million export jobs in China

- “Iran Dangles ‘Trillion Dollar’ Incentive For Trump in Deal Talks”

*

- Reuters report now – White House official says Trump expected to soften auto tariffs

- Wall Street Journal says Trump to soften blow on automotive tariffs

*

- ICYMI – Tesla expects first Semi trucks to enter production by end-2025

- China’s FM says concession and retreat will only make the bully more aggressive

- Reports that US (R) Senator Paul expects to have votes to block Trump’s tariffs (but …)

- Morgan Stanley says the falling US dollar could fuel US stock outperformance

- Nikkei: “Japan life insurers set to cut JGB holdings by $9bn”

- Dalio on Trump tariff turmoil – warns it’s ‘too late’

- Extend-and-Pretend. US tax bill goal date was Memorial Day, now Bessent hopes for July 4

- Spain to release 3 days worth of Strategic Oil Reserves

- Forexlive Americas FX news wrap 28 Apr. GBPUSD moves to highest level since 2022

*

*

- Friday’s non-farm payroll report for April – preview

- New Zealand fin min says Treasury sees lower growth in 2025 & 2026 – due to Trump tariffs

- US stocks close mixed/little changed

- GBPUSD moves to a new high going back to February 2022

- Trade ideas thread – Tuesday, 29 April, insightful charts, technical analysis, ideas

As

I post projections show that Mark Carney’s Liberal Party has won

the election, but its tight. As I post the question it appears if Carney does win he’ll govern as leader of a minority government. is if Carney will govern in a

majority or minority government.

The

Canadian dollar rose on the early projections of a Carney win. More broadly, EUR, AUD,

NZD and GBP popped a little higher alongside.

As

counting progressed it became more likely that Carney would govern in

a minority. if he wins. CAD slid away after this, other FX along for the rise too

with a lower EUR, AUD, NZD, GBP alongside.

News

and data flow otherwise has been light. Of most note, news broke that

Trump is expected to soften

the impact of his automotive tariffs, preventing duties on

foreign-made cars from stacking on top of other tariffs he has

imposed and easing some levies on foreign parts used to manufacture

cars in the U.S. He’s

expected to confirm this on Tuesday (US time) on a trip top Detroit.

US

equity index futures reopened for evening trade (US time) with a gap

lower but on this latest Trump reversal have gained.

As

a bonus news item for UK readers (good morning!) … The UK and the

EU are set to sign a formal declaration committing to “free and

open trade” in defiance of Donald Trump’s tariff agenda. A leaked

draft seen by POLITICO promises a “new strategic partnership”

between London and Brussels. Bye-bye Brexit?

This article was written by Eamonn Sheridan at www.forexlive.com.

IC Markets Asia Fundamental Forecast | 29 April 2025

415697 April 29, 2025 11:00 ICMarkets Market News

IC Markets Asia Fundamental Forecast | 29 April 2025

What happened in the U.S. session?

With no major macroeconomic data release overnight, news headlines focused on U.S. President Donald Trump’s plan to modify the White House’s automotive tariffs by preventing duties from stacking on top of other tariffs that had been imposed earlier, while also scaling back some duties on foreign parts, according to a Wall Street Journal report. The move will mean that U.S. automakers paying automotive tariffs will not be subject to other duties, such as those on steel and aluminium, with the potential tariff relief likely aimed at allowing automakers more time to shift and onshore their supply chains. After seeing demand pick up last week, the greenback fell out of favour once more on Monday as the dollar index (DXY) fell 0.7%, dipping under the 99 level by the end of this session. Despite positive tariff news feeding through over the past week, financial markets remain on edge while trade policy uncertainty persists.

What does it mean for the Asia Session?

Reserve Bank of Australia (RBA) Assistant Governor Christopher Kent will be delivering a speech titled “Australia’s External Position and the Evolution of the FX Markets” at an event hosted by Bloomberg in Sydney. During this event, he may be pressed with questions on the ongoing tariff negotiations between the U.S. and China – which is Australia’s largest trading partner. Demand for the Aussie remained robust as this currency pair climbed above the threshold of 0.6400 overnight.

The Dollar Index (DXY)

Key news events today

JOLTS Job Openings (2:00 pm GMT)

CB Consumer Confidence (2:00 pm GMT)

What can we expect from DXY today?

After decreasing from 7.76M to 7.57M in February, job openings are anticipated to fall for the second consecutive month in March, down to 7.49M as reported by the JOLTS report. With the ongoing trade uncertainty between the U.S. and its major trading partners, it will not be surprising to see many U.S. corporations applying the brakes on aggressive hiring policies in the near term. Meanwhile, consumer confidence is set to report another notable drop. Following last Friday’s sharp decline in the University of Michigan’s sentiment survey, the Conference Board (CB) is expected to fall from 92.9 in the previous month to 87.7 in April – this would mark the fifth successive month of decline. The dollar could face strong headwinds should the above data come in worse than originally forecasted.

Central Bank Notes:

- The Board of Governors of the Federal Reserve System voted unanimously to maintain the Federal Funds Rate in a target range of 4.25 to 4.50% on 19 March 2025

- The Committee seeks to achieve maximum employment and inflation at the rate of 2% over the longer run but uncertainty around the economic outlook has increased; the Committee is attentive to the risks to both sides of its dual mandate.

- Recent indicators suggest that economic activity has continued to expand at a solid pace while the unemployment rate has stabilized at a low level in recent months, and labour market conditions remain solid. However, inflation remains somewhat elevated.

- GDP growth forecasts were revised downward for 2025 (1.7% vs. 2.1% in the December projection) while PCE inflation projections have been adjusted slightly higher for 2025, with core inflation expected to reach 2.5%, partly due to tariff-related pressures.

- In assessing the appropriate stance of monetary policy, the Committee will continue to monitor the implications of incoming information for the economic outlook and is prepared to adjust the stance of monetary policy as appropriate if risks emerge that could impede the attainment of its goals.

- Beginning in April, the Committee will slow the pace of decline of its securities holdings by reducing the monthly redemption cap on Treasury securities from $25B to $5B while maintaining the monthly redemption cap on agency debt and agency mortgage-backed securities at $35B.

- The next meeting is scheduled for 6 to 7 May 2025.

Next 24 Hours Bias

Weak Bearish

Gold (XAU)

Key news events today

JOLTS Job Openings (2:00 pm GMT)

CB Consumer Confidence (2:00 pm GMT)

What can we expect from Gold today?

After decreasing from 7.76M to 7.57M in February, job openings are anticipated to fall for the second consecutive month in March, down to 7.49M as reported by the JOLTS report. With the ongoing trade uncertainty between the U.S. and its major trading partners, it will not be surprising to see many U.S. corporations applying the brakes on aggressive hiring policies in the near term. Meanwhile, consumer confidence is set to report another notable drop. Following last Friday’s sharp decline in the University of Michigan’s sentiment survey, the Conference Board (CB) is expected to fall from 92.9 in the previous month to 87.7 in April – this would mark the fifth successive month of decline. The dollar could face strong headwinds should the above data come in worse than originally forecasted, which would provide a lift for gold.

Next 24 Hours Bias

Weak Bearish

The Australian Dollar (AUD)

Key news events today

RBA Assist Gov Kent Speaks (2:05 am GMT)

What can we expect from AUD today?

Reserve Bank of Australia (RBA) Assistant Governor Christopher Kent will be delivering a speech titled “Australia’s External Position and the Evolution of the FX Markets” at an event hosted by Bloomberg in Sydney. During this event, he may be pressed with questions on the ongoing tariff negotiations between the U.S. and China – which is Australia’s largest trading partner. Demand for the Aussie remained robust as this currency pair climbed above the threshold of 0.6400 overnight.

Central Bank Notes:

- The RBA maintained the cash rate at 4.10% on 1 April, following a 25-basis point reduction on 18 February.

- Inflation has fallen substantially since the peak in 2022, as higher interest rates have been working to bring aggregate demand and supply closer towards balance.

- Recent information suggests that underlying inflation continues to ease in line with the most recent forecasts published in the February Statement on Monetary Policy.

- Private domestic demand appears to be recovering, real household incomes have picked up and there has been an easing in some measures of financial stress. However, businesses in some sectors continue to report that weakness in demand makes it difficult to pass on cost increases to final prices.

- At the same time, a range of indicators suggest that labour market conditions remain tight. Despite a decline in employment in February, measures of labour underutilisation are at relatively low rates and business surveys and liaison suggest that availability of labour is still a constraint for a range of employers. Wage pressures have eased a little more than expected but productivity growth has not picked up and growth in unit labour costs remains high.

- There are notable uncertainties about the outlook for domestic economic activity and inflation. The central projection is for growth in household consumption to continue to increase as income growth rises. But there is a risk that any pick-up in consumption is slower than expected, resulting in continued subdued output growth and a sharper deterioration in the labour market than currently expected.

- Uncertainty about the outlook abroad also remains significant. On the macroeconomic policy front, recent announcements from the U.S. on tariffs are having an impact on confidence globally and this would likely be amplified if the scope of tariffs widens, or other countries take retaliatory measures. Geopolitical uncertainties are also pronounced.

- The Board’s assessment is that monetary policy remains restrictive and the continued decline in underlying inflation is welcome, but there are nevertheless risks on both sides and the Board is cautious about the outlook.

- The Board will rely upon the data and the evolving assessment of risks to guide its decisions and is resolute in its determination to sustainably return inflation to target and will do what is necessary to achieve that outcome.

- The next meeting is on 20 May 2025.

Next 24 Hours Bias

Weak Bullish

The Kiwi Dollar (NZD)

Key news events today

No major news events.

What can we expect from NZD today?

The Kiwi has rallied over 7% since the beginning of April with no signs of demand waning. This currency pair dipped under the threshold of 0.6000 as Asian markets came online on Tuesday but the weaker greenback should keep it supported as the day progresses.

Central Bank Notes:

- The Monetary Policy Committee (MPC) agreed to reduce the Official Cash Rate (OCR) by 25 basis points bringing it down to 3.50% on 9 April, marking the fifth consecutive rate cut.

- The Committee assessed that annual consumer price inflation remains near the midpoint of the MPC’s 1 to 3% target band while firms’ inflation expectations and core inflation are consistent with inflation remaining at target over the medium term.

- Economic activity has evolved largely as expected since the February Monetary Policy Statement; higher-than-expected export prices and a lower exchange rate have supported primary sector incomes and overall economic growth.

- Although monetary restraint had been removed at pace, household spending and residential investment have remained weak.

- The recently announced increases in global trade barriers weaken the outlook for global economic activity. On balance, these developments create downside risks to the outlook for economic activity and inflation.

- The Committee noted that the increase in tariffs will take time to work through the global economy, but the direct price increases for economies imposing tariffs and the dampening impact of increased economic uncertainty on global demand will occur relatively quickly.

- With CPI inflation close to the mid-point of the target range, significant spare capacity in the economy, and a weaker activity outlook stemming from global trade policy, the Committee agreed that a further reduction in the OCR was appropriate.

- Meanwhile, future policy decisions will be determined by the outlook for inflationary pressure over the medium term.

- The next meeting is on 28 May 2025.

Next 24 Hours Bias

Weak Bullish

The Japanese Yen (JPY)

Key news events today

No major news events.

What can we expect from JPY today?

Global trade policy uncertainties have kept demand for safe-haven currencies elevated with USD/JPY falling 1.2% overnight. This currency pair fell under 142 at the beginning of this session, with overhead pressures building once again.

Central Bank Notes:

- The Policy Board of the Bank of Japan decided on 19 March, by a unanimous vote, to maintain the following guidelines for money market operations for the inter-meeting period:

- The Bank will encourage the uncollateralized overnight call rate to remain at around 0.5%.

- The Bank will continue its plan to reduce the amount of its monthly outright purchases of JGBs, aiming to reach about 3 trillion yen by January-March 2026.

- Japan’s economy has continued to recover moderately, with some sectors showing improvement. Exports and industrial production have remained relatively stable, while corporate profits continue on an improving trend and business sentiment maintains a favourable level.

- The employment and income situation has shown moderate improvement, with private consumption on a moderately increasing trend despite ongoing impacts from price rises.

- On the price front, the year-on-year rate of increase in the consumer price index (CPI, all items less fresh food) has been in the range of 3.0-3.5% recently. Services prices continue to rise moderately, reflecting factors such as wage increases, while the effects of cost pass-through from past import price rises have diminished.

- Inflation expectations have continued to rise moderately, with underlying CPI inflation gradually increasing toward the price stability target of 2%. The virtuous cycle between wages and prices continues to strengthen, with businesses increasingly reflecting higher costs in selling prices.

- Japan’s economy is expected to maintain growth above its potential rate, supported by moderately growing overseas economies and the intensifying virtuous cycle from income to spending, underpinned by accommodative financial conditions.

- The next meeting is scheduled for 1 May 2025.

Next 24 Hours Bias

Weak Bearish

The Euro (EUR)

Key news events today

Germany GfK Consumer Climate (6:00 am GMT)

What can we expect from EUR today?

Germany’s consumers have seen their confidence level plummet since November 2021 with no signs of improvement. The estimate of -25.6 for May points to another month of consumer pessimism despite the recently adopted fiscal stimulus package, which many hope would be implemented swiftly and effectively. Should consumer sentiment deteriorate more than anticipated, the Euro could face headwinds before the start of the European session.

Central Bank Notes:

- The Governing Council reduced the three key ECB interest rates by 25 basis points on 17 April to mark the sixth successive rate cut.

- Accordingly, the interest rate on the main refinancing operations and the interest rates on the marginal lending facility and the deposit facility will be decreased to 2.40%, 2.65% and 2.25% respectively.

- The disinflation process is well on track with both headline and core inflation declining in March while services inflation has also eased markedly over recent months. Most measures of underlying inflation suggest that inflation will settle at around the Governing Council’s 2% medium-term target on a sustained basis.

- Wage growth is moderating, and profits are partially buffering the impact of still elevated wage growth on inflation. The euro area economy has been building up some resilience against global shocks, but the outlook for growth has deteriorated owing to rising trade tensions.

- Increased uncertainty is likely to reduce confidence among households and firms, and the adverse and volatile market response to the trade tensions is likely to have a tightening impact on financing conditions. These factors may further weigh on the economic outlook for the euro area.

- The asset purchase programme (APP) and pandemic emergency purchase programme (PEPP) portfolios are declining at a measured and predictable pace, as the Eurosystem no longer reinvests the principal payments from maturing securities.

- The Governing Council is determined to ensure that inflation stabilises sustainably at its 2% medium-term target. Especially in current conditions of exceptional uncertainty, it will follow a data-dependent and meeting-by-meeting approach to determining the appropriate monetary policy stance.

- In particular, the Council’s interest rate decisions will be based on its assessment of the inflation outlook in light of the incoming economic and financial data, the dynamics of underlying inflation and the strength of monetary policy transmission.

- The next meeting is on 5 June 2025.

Next 24 Hours Bias

Weak Bullish

The Swiss Franc (CHF)

Key news events today

No major news events.

What can we expect from CHF today?

The Swiss franc continues to see strong inflows due to elevated demand for safe-haven currencies as USD/CHF declined 1.2% overnight. This currency pair was floating around 0.8200 as Asian markets came online but overhead pressures persist.

Central Bank Notes:

- The SNB eased monetary policy by lowering its key policy rate by 25 basis points, from 0.50% to 0.25% on 20 March 2025, marking the fifth consecutive reduction.

- Underlying inflationary pressure has decreased further this quarter.

- Inflation in the period since the last monetary policy assessment has again been lower than expected, decreasing from 0.7% in November to 0.3% in February, primarily due to lower electricity prices.

- In the shorter term, the new conditional inflation forecast is slightly higher than December: 0.3% for Q2 2025, 0.4% for 2025 overall, and 0.8% for 2026 and 2027, based on the assumption that the SNB policy rate remains at 0.25% over the entire forecast horizon.

- GDP growth in Switzerland remains moderate, with the services sector continuing to show slightly stronger growth, while manufacturing faces challenges.

- The SNB anticipates GDP growth of around 1.0% to 1.5% for 2025.

- The SNB will continue to monitor the situation closely and will adjust its monetary policy if necessary to ensure inflation remains within the range consistent with price stability over the medium term.

- The next meeting is on 19 June 2025.

Next 24 Hours Bias

Weak Bearish

The Pound (GBP)

Key news events today

No major news events.

What can we expect from GBP today?

Demand for the pound remained robust as Cable rebounded over 0.5% after gapping lower at yesterday’s open. This currency pair once again climbed above the threshold of 1.3300, showing no signs of losing steam – a break above 1.3400 on Tuesday should come as no surprise.

Central Bank Notes:

- The Bank of England’s Monetary Policy Committee (MPC) voted by a majority of 8 to 1 to maintain the Bank Rate at 4.50% on 19 March 2025, while one member preferred to reduce it by 25 basis points (bps).

- The MPC also voted unanimously to reduce the stock of UK government bond purchases held for monetary policy purposes and financed by the issuance of central bank reserves, by £100B over the next 12 months to a total of £558B, starting in October 2024. On 18 December 2024, the stock of UK government bonds held for monetary policy purposes was £655B.

- Twelve-month CPI inflation increased to 3.0% in January from 2.5% in December, slightly higher than expected in the February Report; domestic price and wage pressures are moderating, but remain somewhat elevated.

- Although global energy prices have fallen back recently, they remain higher than last year and CPI inflation is still projected to rise to around 3.75% in 2025 Q3. While CPI inflation is expected to fall back thereafter, the Committee will pay close attention to any consequent signs of more lasting inflationary pressures.

- While UK GDP growth estimates have been slightly stronger than expected at the time of the February Monetary Policy Report, business survey indicators generally continue to suggest weakness in growth and particularly in employment intentions. In recent quarters, subdued activity has been judged to reflect both demand and supply factors.

- The labour market had continued to ease, although it was still judged to be broadly in balance – some indicators of employment intentions had deteriorated markedly, to levels consistent with shrinking employment while other indicators, such as the number of vacancies, had not weakened to the same extent.

- Domestic price and wage pressures were moderating, but remained somewhat elevated. A range of indicators suggested that underlying pay growth had eased further in recent months, although annual growth in private sector regular average weekly earnings had picked up to 6.1% in the three months to January.

- Based on the Committee’s evolving view of the medium-term outlook for inflation, a gradual and careful approach to the further withdrawal of monetary policy restraint is appropriate and it will continue to monitor closely the risks of inflation persistence and what the evolving evidence may reveal about the balance between aggregate supply and demand in the economy.

- Monetary policy will need to continue to remain restrictive for sufficiently long until the risks to inflation returning sustainably to the 2% target in the medium term have dissipated further and the Committee will decide the appropriate degree of monetary policy restrictiveness at each meeting.

- The next meeting is on 8 May 2025.

Next 24 Hours Bias

Medium Bullish

The Canadian Dollar (CAD)

Key news events today

Federal Election (All Day)

What can we expect from CAD today?

Canadian voters continue to head to the polls to elect members of the House of Commons to the 45th Canadian Parliament – this will be the first election to use a new 343-seat electoral map based on the 2021 Canadian census. Mark Carney, incumbent Prime Minister and the leader of the Liberal party, will be looking to secure another term for his party. Traders should brace themselves for higher volatility in the Loonie, especially if there is a major upset for the incumbents.

Central Bank Notes:

- The Bank of Canada today maintained its target for the overnight rate at 2.75%, with the Bank Rate at 3% and the deposit rate at 2.70% – marking the first pause after seven consecutive meetings where rates were reduced.

- The major shift in direction of U.S. trade policy and the unpredictability of tariffs have increased uncertainty, diminished prospects for economic growth, and raised inflation expectations.

- Pervasive uncertainty makes it unusually challenging to project GDP growth and inflation in Canada and globally – the April Monetary Policy Report (MPR) presents two scenarios that explore different paths for US trade policy.

- In the first scenario, uncertainty is high but tariffs are limited in scope – Canadian growth weakens temporarily and inflation remains around the 2% target. In the second scenario, a protracted trade war causes Canada’s economy to fall into recession this year and inflation rises temporarily above 3% next year.

- Global economic growth was solid in late 2024 and inflation has been easing towards central bank targets. However, tariffs and uncertainty have weakened the outlook. In the U.S., the economy is showing signs of slowing amid rising policy uncertainty and rapidly deteriorating sentiment, while inflation expectations have risen. In the Euro Area, growth has been modest in early 2025, with continued weakness in the manufacturing sector. China’s economy was strong at the end of 2024 but more recent data shows it slowing modestly.

- In Canada, the economy is slowing as tariff announcements and uncertainty pull down consumer and business confidence. Consumption, residential investment and business spending all look to have weakened in the first quarter. Trade tensions are also disrupting recovery in the labour market. Employment declined in March and businesses are reporting plans to slow their hiring. Wage growth continues to show signs of moderation.

- The Governing Council will continue to assess the timing and strength of both the downward pressures on inflation from a weaker economy and the upward pressures on inflation from higher costs while proceeding carefully, with particular attention to the risks and uncertainties facing the Canadian economy.

- Monetary policy cannot resolve trade uncertainty or offset the impacts of a trade war and the Governing Council will focus on ensuring that Canadians continue to have confidence in price stability through this period of global upheaval by supporting economic growth while ensuring that inflation remains well-controlled.

- The next meeting is on 4 June 2025.

Next 24 Hours Bias

Weak Bullish

Oil

Key news events today

API Crude Oil Stock (8:30 pm GMT)

What can we expect from Oil today?

Lower demand growth expectations for crude oil continue to weigh on this commodity as WTI oil tumbled 2.3% on Monday. U.S. President Donald Trump’s push to reshape world trade by imposing tariffs on all U.S. imports has created a high risk that the global economy will slip into a recession this year, according to a majority of economists in a Reuters poll. Moving over to U.S. inventories, the API stockpiles have been building steadily since February, a sign of weaker demand. Another week of higher inventory levels would heap even more pressure on oil prices later today.

Next 24 Hours Bias

Medium Bearish

The post IC Markets Asia Fundamental Forecast | 29 April 2025 first appeared on IC Markets | Official Blog.

China’s 2nd batch of 81 bn yuan ultra-long special treasury bonds for consumer trade-in

415696 April 29, 2025 10:39 Forexlive Latest News Market News

China’s NDRC allocates second batch of 81 billion yuan in ultra-long special treasury bonds for consumer trade-in programs.

—

The National Development and Reform Commission of the People’s Republic of China (NDRC) is China’s State Planner.

This article was written by Eamonn Sheridan at www.forexlive.com.

There is one Canadian election outcome that could hurt the loonie … and here it comes

415695 April 29, 2025 10:39 Forexlive Latest News Market News

Adam posted this prior to the election, and it looks like its coming to fruition:

- The outcome I believe that could offer some downside in the loonie (in the 50-120 pip range) is a Liberal minority held up by the NDP. That would essentially extend the current status quo and leaves the Liberals at the mercy of the left-leaning NDP.

Link here for more:

CAD sliding further:

This article was written by Eamonn Sheridan at www.forexlive.com.