IC – Asia Fundamental Forecast | 06 August 2026

IC – Asia Fundamental Forecast | 06 August 2026 What happened in the U.S. session?A tug-of-war between signs of a cooling labor market and continued economic resilience. A weaker ADP employment report…

IC – Asia Fundamental Forecast | 06 August 2026 What happened in the U.S. session?A tug-of-war between signs of a cooling labor market and continued economic resilience. A weaker ADP employment report…

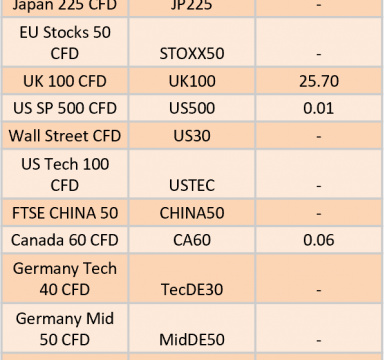

The post Ex-Dividend 06/08/2026 first appeared on IC Your Trading Edge | Official Blog.

Global Markets: Asian Stock Markets : Nikkei up 3.13%, Shanghai Composite up 1.34% Hang Seng down 0.01% ASX up 0.74% Commodities : Gold at $4,196.55 (1.05%) Silver at $61.108 (1.42%), Brent Oil…

IC – Europe Fundamental Forecast | 05 August 2026 What happened in the Asia session?The Asia session was dominated by improving geopolitical sentiment rather than major regional economic releases. Reports of progress…

DXY (U.S. Dollar Index): Potential Direction: Bearish Overall momentum of the chart: Bearish The price could see a short-term pullback toward the pivot before continuing its bearish move down toward the…

US Stocks Surge as Middle East Optimism Grows – S&P up 1.8% to Fresh Record US equity markets pushed sharply higher again overnight as optimism around a potential peace deal in the…

IC – Asia Fundamental Forecast | 05 August 2026 What happened in the U.S. session?The U.S. session was dominated by positioning ahead of key labor and services-sector releases, with traders balancing signs…

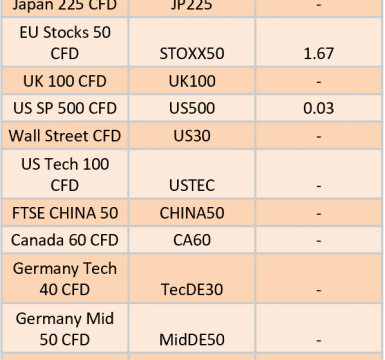

The post Ex-Dividend 05/08/2026 first appeared on IC Your Trading Edge | Official Blog.

Global Markets: Asian Stock Markets : Nikkei down 0.35%, Shanghai Composite up 0.16% Hang Seng down 0.57% ASX up 1.23% Commodities : Gold at $4,112.72 (0.54%) Silver at $59.000 (1.98%), Brent Oil…

IC Markets – Europe Fundamental Forecast | 04 September 2026 What happened in the Asia session?Today’s Asia session was relatively quiet, with no major regional data releases driving markets. Instead, investors focused…

DXY (U.S. Dollar Index): Potential Direction: Bearish Overall momentum of the chart: Bearish The price could see a short-term pullback toward the pivot before continuing its bearish move down toward the…

US Stocks Drive Higher on Peace Talks – S&P up 1.5%US equity markets rallied strongly overnight as investors grew increasingly optimistic that a peace agreement may be reached in the Middle East.…