IC – Asia Fundamental Forecast | 04 August 2026

IC – Asia Fundamental Forecast | 04 August 2026 What happened in the U.S. session?A shift toward diplomacy between the U.S. and Iran caused crude oil prices to tumble, easing inflation fears…

IC – Asia Fundamental Forecast | 04 August 2026 What happened in the U.S. session?A shift toward diplomacy between the U.S. and Iran caused crude oil prices to tumble, easing inflation fears…

IC – Europe Fundamental Forecast | 03 September 2026 What happened in the Asia session?The Asia session was driven almost entirely by geopolitical headlines rather than scheduled economic data. Reports of upcoming…

DXY (U.S. Dollar Index): Potential Direction: Bearish Overall momentum of the chart: Bearish The price could see a short-term pullback toward the pivot before continuing its bearish move down toward the…

Global Markets: Asian Stock Markets : Nikkei down 1.16%, Shanghai Composite down 0.59% Hang Seng down 0.01% ASX down 0.14% Commodities : Gold at $4,121.67 (0.36%) Silver at $58.415 (1.09%), Brent Oil…

It was another very busy week for financial markets last week as the ongoing conflict in the Middle East continued to weigh on investor sentiment, as did continued concerns over tech company…

IC – Asia Fundamental Forecast | 03 August 2026 What happened in the U.S. session?The U.S. session overnight was characterized by a risk-on tone in equities following strong earnings from major technology…

The post Ex-Dividend 04/08/2026 first appeared on IC Your Trading Edge | Official Blog.

US Stocks Higher into Weekend – Nasdaq up 1%US equity markets finished the week on a strong footing on Friday as investors chose to focus on strong earnings numbers from some of…

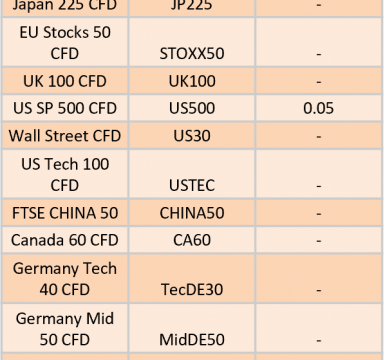

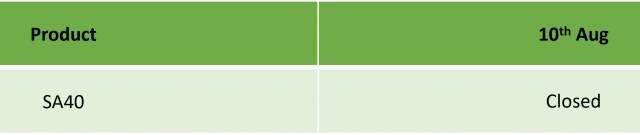

Dear Client, Please find our updated Trading schedule and general information related to the National Women’s Day Holiday on Monday, 10 August, 2026. Liquidity over the holidays is expected to be particularly…

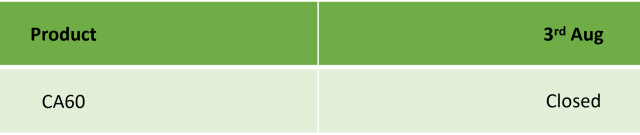

Dear Client, Please find our updated Trading schedule and general information related to the Canada Civic Holiday on Monday, 3 August, 2026. Liquidity over the holidays is expected to be particularly thin…

Dear Client, Please find our updated Trading schedule and general information related to the Mountain Day Holiday on Tuesday, 11 August, 2026. Liquidity over the holidays is expected to be particularly thin…

Kính gửi Quý khách hàng, Vui lòng tham khảo lịch giao dịch đã được cập nhật cùng các thông tin chung liên quan đến kỳ nghỉ lễ Ngày Phụ nữ Quốc gia…