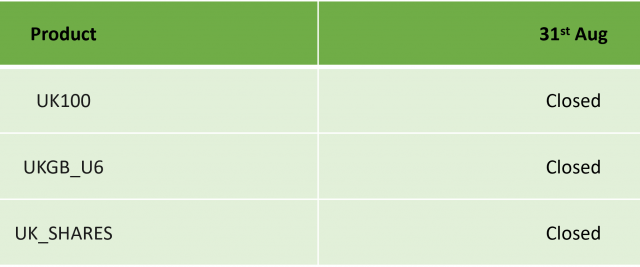

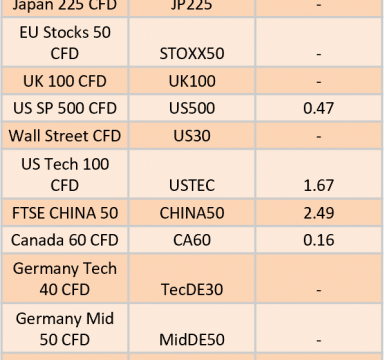

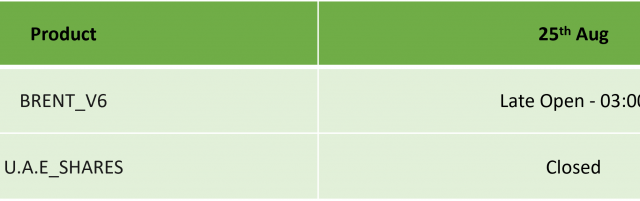

Prophet Muhammad’s Birthday Holiday Trading Schedule 2026

Dear Client, Please find our updated Trading schedule and general information related to the Prophet Muhammad’s Birthday Holiday on Tuesday, 25 August, 2026. Liquidity over the holidays is expected to be particularly…