General Market Analysis – 30/07/26

US Stocks Fall After Fed Hold and War Continues – Dow down 2% US equity markets came under heavy selling pressure overnight after the Federal Reserve left interest rates unchanged, with investors…

US Stocks Fall After Fed Hold and War Continues – Dow down 2% US equity markets came under heavy selling pressure overnight after the Federal Reserve left interest rates unchanged, with investors…

IC – Asia Fundamental Forecast | 30 July 2026 What happened in the U.S. session?The overnight U.S. session was dominated by the Federal Reserve’s decision to keep interest rates unchanged at 3.50%–3.75%,…

DXY (U.S. Dollar Index): Potential Direction: Bullish Overall momentum of the chart: Bearish The price has already bounced off the pivot and may continue its bullish move toward the 1st resistance…

Global Markets: Asian Stock Markets : Nikkei down 2.72%, Shanghai Composite down 0.53% Hang Seng up 1.27% ASX up 0.92% Commodities : Gold at $4,020.90 (-0.44%) Silver at $57.585 (0.11%), Brent Oil…

IC – Asia Fundamental Forecast | 29 July 2026 What happened in the U.S. session?Market participants largely refrained from making aggressive moves ahead of today’s highly anticipated FOMC interest rate decision, policy…

IC – Europe Fundamental Forecast | 29 July 2026 What happened in the Asia session?The Asia session was driven almost entirely by Australia’s softer-than-expected inflation report, which reduced expectations for additional RBA…

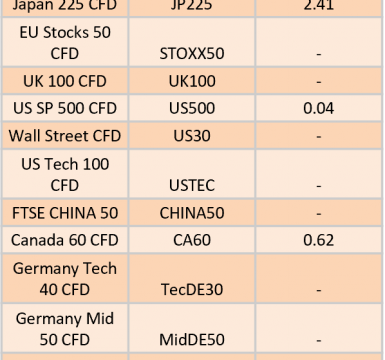

The post Ex-Dividend 30/07/2026 first appeared on IC Your Trading Edge | Official Blog.

US Stocks Mixed Ahead of Key Fed Call – Dow up 1% US equity markets delivered a mixed performance overnight as investors remained cautious ahead of today’s highly anticipated Federal Reserve interest…

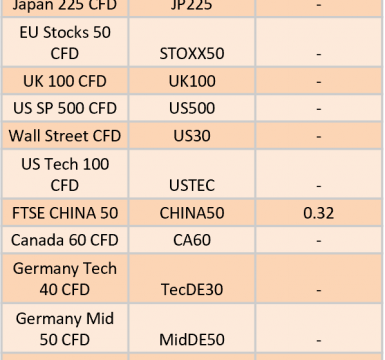

The post Ex-Dividend 29/07/2026 first appeared on IC Your Trading Edge | Official Blog.

IC – Europe Fundamental Forecast | 28 July 2026 What happened in the Asia session?Market attention was dominated by Reserve Bank of Australia (RBA) Governor Michele Bullock’s speech, while traders also continued…

Global Markets: Asian Stock Markets : Nikkei down 3.95%, Shanghai Composite down 0.98% Hang Seng down 0.31% ASX up 0.40% Commodities : Gold at $4,044.20 (-0.80%) Silver at $57.460 (-2.15%), Brent Oil…

DXY (U.S. Dollar Index): Potential Direction: Bearish Overall momentum of the chart: Bearish The price has already reacted off the pivot and may continue its bearish move toward the 1st support.…