Articles

IC Markets Global – Europe Fundamental Forecast | 18 December 2025

424685 December 18, 2025 16:00 ICMarkets Market News

IC Markets Global – Europe Fundamental Forecast | 18 December 2025

What happened in the Asia session?

During the Asia session, New Zealand’s robust Q3 GDP print of +1.1% q/q led the macroeconomic releases, outshining minor events like Japan’s bill auction, but failed to lift NZD/USD amid USD strength and global caution from Wall Street tech declines. Markets saw broad equity slips in Nikkei (-1.56%), Hang Seng, and Shanghai, with banks like DBS/OCBC bucking the trend on positive news, while Korea Zinc tanked 14%; forex pairs like NZD/USD and JPY yields reflected tempered reactions ahead of central bank moves.

What does it mean for the Europe & US sessions?

Traders should monitor key U.S. jobless claims data and regional manufacturing indexes releasing at 13:30 GMT, alongside the ECB’s interest rate decision at 14:15 GMT and press conference at 14:45 GMT, as European and U.S. sessions open amid recent market volatility from tech selloffs and Fed hawkishness. Asian stocks fell overnight due to tech pullbacks, with U.S. futures little changed ahead of inflation concerns, while European tariffs from U.S. policy strain growth forecasts.

The Dollar Index (DXY)

Key news events today

President Trump Speaks (2:00 am GMT)

CPI y/y (1:30 pm GMT)

Unemployment Claims (1:30 pm GMT

Philly Fed Manufacturing Index (1:30 pm GMT)

What can we expect from DXY today?

The US Dollar showed resilience in early trading, holding gains versus the yen and sterling amid positioning for central bank meetings, though it remained pressured by a year-long downtrend of over 9%, dovish Fed outlooks signalling more 2026 rate cuts, and anticipation of US inflation data alongside ECB and BOJ decisions.

Central Bank Notes:

- The Federal Open Market Committee (FOMC) is widely expected to lower the federal funds rate target range by 25 basis points to 3.50%–3.75% at its December 9–10, 2025, meeting, marking the third consecutive cut after the October reduction to 3.75%–4.00%

- The Committee continues to pursue maximum employment and 2% inflation goals, with the labour market showing further softening as the unemployment rate rose to 4.4% in September 2025 amid modest job gains.

- Officials note persistent downside risks to growth alongside resilient activity, with inflation easing to 3.0% year-over-year CPI in September but remaining elevated due to tariff effects; core PCE stands at around 2.8% as of October.

- Economic activity grew at a 3.8% annualised pace in Q2 2025 per revised estimates, though Q3 and Q4 face headwinds from trade tensions, fiscal restraint, and data disruptions like the government shutdown.

- September’s Summary of Economic Projections forecasts 2025 unemployment at a median 4.5%, with PCE inflation near 3.0% and core PCE at 3.1%, signalling a gradual disinflation path; updates expected on December 10 may adjust for higher unemployment and lower growth.

- The Committee maintained its data-dependent approach, noting a softening labour market and inflation above the 2% target, while deciding to lower the federal funds rate target range by 25 basis points to 3.50%-3.75%. Dissent persisted, with multiple members opposing the cut or advocating for a hold, reflecting divisions similar to recent meetings.

- The FOMC confirmed the conclusion of its quantitative tightening program effective December 1, 2025, with Treasury rolloff caps at $5 billion per month and agency MBS caps at $35 billion per month to ensure ample reserves and market stability.

- The next meeting is scheduled for 27 to 28 January 2026.

Next 24 Hours Bias

Medium Bearish

Gold (XAU)

Key news events today

President Trump Speaks (2:00 am GMT)

CPI y/y (1:30 pm GMT)

Unemployment Claims (1:30 pm GMT

Philly Fed Manufacturing Index (1:30 pm GMT)

What can we expect from Gold today?

Gold maintains upward momentum near $4,333, driven by investment flows, a softer dollar, and economic signals like US job data hinting at Fed easing, though technical overbought levels and post-festive import drops in key markets like India temper gains, positioning it for potential consolidation before further advances.

Next 24 Hours Bias

Medium Bullish

The Euro (EUR)

Key news events today

Main Refinancing Rate (1:15 pm GMT)

Monetary Policy Statement (1:15 pm GMT)

ECB Press Conference (1:45 pm GMT)

What can we expect from EUR today?

The euro experienced modest fluctuations against the US dollar, trading around the 1.1750 level amid anticipation for the European Central Bank’s monetary policy decision and upcoming US inflation data. ECB President Christine Lagarde has signalled potential upward revisions to Eurozone growth forecasts, reflecting economic resilience despite trade tensions, while investors scaled back expectations for further rate cuts in 2026.

Central Bank Notes:

- The Governing Council of the ECB is widely expected to keep the three key interest rates unchanged at its 17–18 December 2025 meeting, maintaining the main refinancing rate at 2.15%, the marginal lending facility at 2.40% and the deposit facility at 2.00%. This would reflect policymakers’ assessment that the current policy stance remains broadly consistent with medium‑term price stability, while inflation hovers close to the 2% target and the economy expands at a modest pace. Market pricing and recent ECB commentary suggest a high “option value” in staying on hold, with no clear pre‑set path for the next move amid two‑sided risks around growth and inflation.

- Recent indicators point to broadly stable price dynamics around the ECB’s target. Headline HICP inflation is projected to hover near 2% through late 2025, with earlier energy‑related disinflation largely behind and food price pressures contained compared with previous years. Services and wage inflation remain somewhat firmer than anticipated, but the trend is one of gradual moderation, consistent with a scenario in which inflation stabilises around but not persistently above 2% over the medium term.

- Eurosystem staff projections to be released in December are expected to show only small revisions from the September exercise, maintaining a profile of headline inflation close to 2% in 2025, dipping slightly below in 2026, and returning near target in 2027. Soft producer prices, fading pipeline cost pressures, and anchored long‑term inflation expectations limit upside risks, though officials continue to flag uncertainty from geopolitical tensions, commodity price shocks,s and fiscal policy choices.

- Euro area GDP growth remains subdued but resilient, with most forecasters and survey‑based indicators pointing to an expansion around 1 — 1.25% in 2025 and 2026, followed by a similar pace into 2027. PMIs and confidence surveys suggest activity has stabilised after earlier weakness, with modest support from public investment and improving external demand offsetting soft private consumption and investment.

- The labour market remains tight in aggregate, with unemployment rates close to multi‑decade lows and participation relatively high, even as job creation has slowed from its earlier peak. Real income growth has turned slightly positive again as inflation normalises, underpinning household spending, while financing conditions, though tighter than in the pre‑hiking era, remain consistent with a gradual expansion in credit to households and firms.

- Business sentiment is mixed, reflecting uncertainty around global trade, the policy outlook in the United States, and the potential impact of future tariff or industrial policy shifts. At the same time, easing supply‑chain costs and a relatively competitive euro exchange rate versus major trading partners provide support to manufacturing and export‑oriented sectors at the margin.

- The Governing Council is expected to reiterate that future decisions will remain data-dependent and taken meeting by meeting, based on an integrated assessment of the inflation outlook, the dynamics of underlying inflation, and the strength of monetary policy transmission. Officials have recently stressed that both further hikes and eventual cuts remain contingent on incoming data, implying no commitment to a particular path and a readiness to adjust if inflation or growth diverge materially from baseline projections.

- Balance sheet normalisation is set to continue gradually and predictably, with the stock of assets under the APP and PEPP declining as reinvestments have already been halted or scaled back in line with prior guidance. The ECB is expected to confirm that the current pace of portfolio runoff remains appropriate, supporting a slow withdrawal of monetary accommodation without disrupting market functioning.

- The next meeting is on 4 to 5 January 2026

Next 24 Hours Bias

Medium Bullish

The Swiss Franc (CHF)

Key news events today

No major news event

What can we expect from CHF today?

The Swiss franc (CHF) remains strong against major currencies today, Thursday, December 18, 2025, holding near multi-year highs amid safe-haven demand and anticipation of the Swiss National Bank’s (SNB) policy meeting concluding today. USD/CHF traded around 0.7946 yesterday, reflecting a slight dip but ongoing CHF appreciation of 0.62% over the past month and 11.82% year-over-year, driven by global uncertainties including US trade tensions and softer dollar sentiment post-Fed decisions.

Central Bank Notes:

- At its 11 December 2025 monetary policy assessment, the Swiss National Bank (SNB) is widely expected to leave the policy rate unchanged at 0%, extending the pause that began in September as the Governing Board judges that current settings are sufficient to keep inflation near, but still below, its target while avoiding an unnecessary move into negative rates.

- Recent data show that the tentative rebound in Swiss inflation has stalled, with headline CPI easing from 0.1% year‑on‑year in October to 0.0% in November and core inflation slipping to about 0.4%, reinforcing the view that underlying price pressures remain very weak and that deflation risks, while contained, have not fully disappeared.

- The SNB’s conditional inflation forecast is likely to remain close to the September projections, with inflation still seen averaging roughly 0.2% in 2025, 0.5% in 2026, and 0.7% in 2027 under an unchanged policy rate path, though the latest CPI prints argue for a slightly lower near‑term profile and keep open the option of renewed easing if activity or prices weaken further.

- The global backdrop has deteriorated further, as continuing U.S. tariff actions and softer external demand weigh on world trade, while uncertainty in key European and U.S. markets for Swiss exports persists, leaving the SNB cautious about the growth outlook despite Switzerland’s relatively resilient domestic demand.

- Business and labour-market sentiment in export‑oriented manufacturing remains subdued, with firms reporting pressure on margins from the still‑strong franc and softer foreign orders, although the broader economy is still expected to grow at around 1–1.5% in 2025 and unemployment only drifting up gradually from low levels.

- The SNB continues to stress its willingness to act if deflation risks re‑emerge, reiterating that it can ease policy through renewed rate cuts or targeted foreign‑exchange intervention if necessary, while also highlighting its commitment to transparent communication, including the publication of detailed minutes from recent assessments and ongoing dialogue with international partners on FX policy

The next meeting is on 19 March 2026.

Next 24 Hours Bias

Medium Bullish

The Pound (GBP)

Key news events today

ECB Press Conference (12:00 pm GMT)

ECB Press Conference (12:00 pm GMT)

Official Bank Rate (12:00 pm GMT)

BOE Gov Bailey Speaks (12:30 pm GMT)

What can we expect from GBP today?

The pound sterling weakened against the dollar to about 1.3398, driven by yesterday’s softer-than-expected UK inflation at 3.2% cementing bets for a Bank of England rate cut to 3.75% today amid stagnant growth and rising unemployment, yet showed signs of intraday resilience with limited selling pressure and forecasts holding steady near 1.34 short-term.

Central Bank Notes:

- The Bank of England’s Monetary Policy Committee (MPC) will meet on 18 December 2025, with the current Bank Rate standing at 4.00 per cent after being held in a close 5–4 vote at the 5 November meeting. Market pricing and analyst commentary point to a high risk of a 25‑basis‑point cut to 3.75 per cent, but this remains conditional on incoming inflation and labour‑market data, so the December note should be treated as pre‑decision guidance rather than an ex‑post summary.

- The BoE is expected to leave its quantitative tightening (QT) framework broadly unchanged through year‑end, maintaining the lower reduction pace in gilt holdings that was set earlier in 2025. Official communications still characterise the existing QT path as consistent with a restrictive stance, with policymakers stressing that balance‑sheet reduction will remain gradual and sensitive to market‑liquidity conditions.

- Headline CPI inflation eased to 3.6 per cent year‑on‑year in October 2025, down from 3.8 per cent in September, helped by softer energy and goods prices, though it remains almost twice the 2 per cent target. Underlying inflation pressures, particularly in services, have continued to moderate only slowly, so the MPC’s central projection still envisages inflation moving closer to, but not yet reaching, 3 per cent over the course of 2026, contingent on further normalisation in energy and wage dynamics.

- UK economic activity remains weak heading into the December meeting, with the labour market showing further signs of slackening. The unemployment rate has risen toward just above 5 per cent on the latest three‑month figures to October, while overall regular pay growth has slowed to around the mid‑4 per cent range, reinforcing the view that domestic cost pressures are gradually easing.

- External conditions continue to cloud the outlook, with fragile global growth and fluctuating commodity prices contributing to bouts of financial‑market volatility. The MPC has highlighted that renewed global energy or food price shocks could temporarily slow the pace of disinflation, but such risks are currently judged unlikely to derail the medium‑term downward trajectory for inflation if domestic demand stays subdued.

- The balance of risks around the inflation outlook remains finely poised. Downside risks are linked to persistently weak domestic demand and rising unemployment, while upside risks come from still‑elevated inflation expectations, sticky services inflation, and the possibility that structural changes in the labour market leave less slack than conventional indicators suggest.

- Overall, the MPC’s stance going into December is restrictive but increasingly open to a gradual easing cycle, with any rate cuts expected to be measured and data‑dependent. Policymakers have reiterated that the Bank Rate will need to stay in restrictive territory until they are confident inflation is on a sustainable path back to the 2 per cent target, and they have signalled that the profile of cuts, once started, is likely to be shallow rather than rapid.

- The next meeting is on 5 February 2026.

Next 24 Hours Bias

Medium Bullish

The Canadian Dollar (CAD)

Key news events today

What can we expect from CAD today?

The Canadian dollar (CAD) showed mild strength on December 18, 2025, with the USD/CAD exchange rate dipping slightly to 1.3784, reflecting a 0.01% decline from the prior session. This was built on recent gains amid mixed U.S. labour data and broader market dynamics, including steady oil prices that support the commodity-linked currency.

Central Bank Notes:

- The Governing Council left the target for the overnight rate unchanged at 2.25% at its 10 December 2025 meeting, in line with market expectations and signalling that the earlier easing cycle has likely concluded. The Bank noted that while global tariff tensions and trade uncertainty persist, the external backdrop has stabilised somewhat, reducing the need for additional insurance cuts even as world trade remains fragile.

- The Council acknowledged that uncertainty around U.S. trade policy and tariffs continues to weigh on business sentiment, but recent data show Canadian manufacturing and goods exports holding up better than anticipated. Surveys cited by the Bank suggest export order books have stopped deteriorating, with firms reporting some rebuilding of backlogs despite still‑cautious capital spending plans.

- Canada’s economy rebounded more strongly than expected in the third quarter, with real GDP expanding at an annualised pace of about 2.6% after a 1.8% contraction in Q2, largely on the back of higher crude exports and government spending. Monthly data show output rising 0.2% in September, though flash estimates point to a softer start to Q4 as some sectors give back earlier gains.

- Service sector activity has firmed, with indicators showing the services PMI back above the 50 threshold and broadening gains in business and professional services. However, consumer-facing categories remain mixed, as still‑elevated price levels and only modest real income growth keep a lid on discretionary spending even as tourism and technology‑related services expand.

- Housing markets have continued to stabilise, with national resale activity and prices edging higher through the autumn alongside the earlier decline in borrowing costs. The Bank noted that while some major urban centres are seeing renewed price pressures, tighter underwriting standards and still‑high affordability constraints are expected to cap the pace of any rebound.

- Headline CPI inflation eased to 2.2% year over year in October and is estimated to have remained near that rate in November, keeping it slightly above the 2% target but comfortably within the 1%–3% control range. Core measures have drifted lower, with CPI‑median and CPI‑trim around 3% or below, reinforcing the assessment that underlying price pressures are gradually moderating even as gasoline and some shelter components remain volatile.

- The Governing Council reiterated that the current policy rate is “about the right level” to keep inflation close to target while supporting the economy through a period of structural adjustment, and it signalled a shift away from near‑term easing expectations. While the Bank did not rule out future adjustments, officials stressed that, barring a material downside surprise to growth or inflation, further rate cuts are unlikely before 2026, and attention is now focused on the durability of the recovery and the evolution of core inflation.

- The next meeting is on 28 January 2026.

Next 24 Hours Bias

Medium Bullish

Oil

Key news events today

No major news event

What can we expect from Oil today?

Oil prices experienced volatility amid geopolitical tensions overshadowing supply glut concerns. West Texas Intermediate (WTI) crude hovered around $56-$57 per barrel after climbing over 1% earlier in the week, while Brent traded above $60. President Donald Trump’s blockade of sanctioned Venezuelan oil tankers sparked a rally, with WTI rising 1.75% to $56.92 in Asian trading as markets reacted to restricted exports. Geopolitical risks extended to Russia, where stalled Ukraine peace talks limited potential supply increases from stored Russian oil.

Next 24 Hours Bias

Medium Bearish

The post IC Markets Global – Europe Fundamental Forecast | 18 December 2025 first appeared on IC Markets | Official Blog.

IC Markets Global – Asia Fundamental Forecast | 18 December 2025

424684 December 18, 2025 16:00 ICMarkets Market News

IC Markets Global – Asia Fundamental Forecast | 18 December 2025

What happened in the U.S. session?

The overnight U.S. session featured a cautious but not panicked tone, with traders rotating between sectors and asset classes rather than making outright directional bets; energy, dollar pairs, front‑end Treasuries, and precious metals were the most sensitive instruments to the latest mix of labor data, Fed expectations, and Venezuelan supply headlines.

What does it mean for the Asia Session?

Asian traders face a relatively quiet local data calendar during the day but a heavy global risk window in the evening Asia time, centred on the Bank of England and European Central Bank rate decisions plus US November CPI, core inflation, and jobless‑claims data, all of which can sharply move GBP, EUR, USD, and global risk assets. At the same time, positioning ahead of Friday’s closely watched Bank of Japan meeting, where markets increasingly price a possible 25 bp hike, keeps JPY and regional equities sensitive to any policy leaks or guidance, arguing for tight intraday risk limits, careful use of stops, and awareness of lower liquidity into the overlapping London–New York sessions.

The Dollar Index (DXY)

Key news events today

President Trump Speaks (2:00 am GMT)

CPI y/y (1:30 pm GMT)

Unemployment Claims (1:30 pm GMT)

Philly Fed Manufacturing Index (1:30 pm GMT)

What can we expect from DXY today?

Today’s dollar trade on Wednesday is characterized by consolidation near two‑month lows within a broader downtrend driven by softer U.S. data and firm expectations of further Fed rate cuts. The currency continues to underperform against higher‑yielding and risk‑sensitive peers such as the Australian and New Zealand dollars, while traditional safe‑havens like the yen and Swiss franc remain supported following the recent Fed‑induced slide.

Central Bank Notes:

- The Federal Open Market Committee (FOMC) is widely expected to lower the federal funds rate target range by 25 basis points to 3.50%–3.75% at its December 9–10, 2025, meeting, marking the third consecutive cut after the October reduction to 3.75%–4.00%

- The Committee continues to pursue maximum employment and 2% inflation goals, with the labor market showing further softening as the unemployment rate rose to 4.4% in September 2025 amid modest job gains.

- Officials note persistent downside risks to growth alongside resilient activity, with inflation easing to 3.0% year-over-year CPI in September but remaining elevated due to tariff effects; core PCE stands at around 2.8% as of October.

- Economic activity grew at a 3.8% annualized pace in Q2 2025 per revised estimates, though Q3 and Q4 face headwinds from trade tensions, fiscal restraint, and data disruptions like the government shutdown.

- September’s Summary of Economic Projections forecasts 2025 unemployment at a median 4.5%, with PCE inflation near 3.0% and core PCE at 3.1%, signaling a gradual disinflation path; updates expected on December 10 may adjust for higher unemployment and lower growth.

- The Committee maintained its data-dependent approach, noting a softening labor market and inflation above the 2% target, while deciding to lower the federal funds rate target range by 25 basis points to 3.50%-3.75%. Dissent persisted, with multiple members opposing the cut or advocating for a hold, reflecting divisions similar to recent meetings.

- The FOMC confirmed the conclusion of its quantitative tightening program effective December 1, 2025, with Treasury rolloff caps at $5 billion per month and agency MBS caps at $35 billion per month to ensure ample reserves and market stability.

- The next meeting is scheduled for 27 to 28 January 2026.

Next 24 Hours Bias

Medium Bearish

Gold (XAU)

Key news events today

President Trump Speaks (2:00 am GMT)

CPI y/y (1:30 pm GMT)

Unemployment Claims (1:30 pm GMT

Philly Fed Manufacturing Index (1:30 pm GMT)

What can we expect from Gold today?

Gold remains firmly bid into Thursday, consolidating above 4,300 USD/oz and trading within striking distance of its October record high as traders price in a softer Federal Reserve trajectory, a weaker dollar, and a cooling US labor market that together support robust safe‑haven demand. Technical and forecast commentary points to an intraday range roughly in the mid‑4,200s to mid‑4,400s, with buyers continuing to defend key support zones and momentum indicators still aligned with an upward trend unless macro data or Fed guidance surprise materially in the opposite direction.

Next 24 Hours Bias

Strong Bullish

The Australian Dollar (AUD)

Key news events today

No major news event

What can we expect from AUD today?

The Australian Dollar is consolidating just above 0.66 against the US Dollar today, Thursday 18 December 2025, after pulling back from recent highs near 0.6685 as the post‑Fed rate‑cut rally pauses. With no major local releases on the docket, AUD moves are being driven mainly by global risk sentiment and positioning ahead of key US data, while underlying support comes from improved terms of trade and expectations that the RBA will lag the Fed in any easing cycle, leaving the currency modestly stronger on a 1‑month and 12‑month horizon even as near‑term price action looks range‑bound.

Central Bank Notes:

- The Reserve Bank of Australia held its cash rate steady at 3.60% at the November 2025 policy meeting, adopting a cautious tone amid a surprise uptick in inflation data for the September quarter. This marks the fourth consecutive pause since the 25 basis point cut in August. The Board attributed some of the inflation rise to temporary factors like higher petrol prices and council rates, but noted signs of more persistent pressures from consumer demand.

- Policymakers emphasized vigilance on inflation, with trimmed mean inflation expected to remain elevated in the near term before nearing the 2–3% target midpoint by mid-2027. Recent data showed underlying inflation staying above target until at least the second half of 2026, prompting upward revisions to forecasts. Capacity pressures are seen as slightly more pronounced than previously assessed, delaying any easing.

- Headline CPI for the September quarter exceeded expectations, driven partly by temporary items, while underlying measures signal ongoing stickiness. The shift to monthly CPI reporting, with the first full edition in November 2025, will enhance real-time inflation monitoring. Housing and services remain resilient contributors to price pressures.

- Domestic demand shows firmness in services alongside below-trend growth elsewhere, with capacity pressures not expected to ease significantly. The labor market is gradually softening, with unemployment projected to stabilize around 4.4%, though wage growth and productivity dynamics keep unit labor costs a concern. Household spending faces headwinds from high borrowing costs.

- Global risks include geopolitical tensions and commodity volatility, set against modestly revised-up world growth outlooks. The Board describes its policy as mildly restrictive and data-dependent, balancing inflation control with employment goals. No rate hike was considered despite the inflation surprise.

- Monetary policy remains mildly restrictive to address lingering price stability risks amid household and global vulnerabilities. Communications reaffirm the dual mandate of 2–3% inflation and full employment, with readiness to adjust based on incoming data.

- Market expectations point to the cash rate holding through early 2026, with a possible modest cut to 3.3% mid-year if inflation eases as forecast. The new monthly CPI data will be key for timely insights.

- Monetary policy remains mildly restrictive, balancing progress on price stability against vulnerabilities in household demand and global outlook. Board communications reaffirm a dual mandate: price stability and full employment, while underscoring readiness to respond should risks materialize sharply.

- Analysts generally expect the cash rate to remain at current levels through early 2026, with only modest cuts possible later in the year if inflation moderates. The new monthly CPI release (first full edition Nov 2025) will be watched closely for timely signals on price trends.

- The next meeting is on 2 to 3 February 2026.

Next 24 Hours Bias

Medium Bullish

The Kiwi Dollar (NZD)

Key news events today

No major news event

What can we expect from NZD today?

The New Zealand dollar is in a holding pattern near 0.58 against the US dollar: it retains a modest bullish bias thanks to a softer greenback and the perception that the RBNZ is on pause, but domestic headwinds (wider external deficit, sluggish growth) and lingering China uncertainty are preventing a sustained breakout. Traders are watching global risk sentiment and upcoming US releases for the next catalyst, with near‑term expectations centred on continued range‑bound trade rather than a decisive new trend leg.

Central Bank Notes:

- The Monetary Policy Committee (MPC) left the Official Cash Rate (OCR) unchanged at 2.25% at its 26 November 2025 meeting, following the widely anticipated 25-basis-point reduction from 2.50%, and signaled that policy is now firmly in stimulatory territory while keeping the option of further easing on the table if needed.

- The decision was again reached by consensus, with members judging that the cumulative 325 basis points of easing over the past year warranted a period of assessment, even as several emphasized a willingness to cut further should incoming data point to a more protracted downturn or renewed disinflationary pressures.

- Headline consumer price inflation is projected to hover near 3% in late 2025 before gradually easing toward the 2% midpoint of the 1–3% target band through 2026, supported by contained inflation expectations around 2.3% over the two-year horizon and an expected pickup in spare capacity.

- The MPC noted that domestic demand remains subdued but shows tentative signs of stabilisation, with softer household spending and construction only partially offset by improving services activity; nevertheless, policymakers still expect services inflation to ease as wage growth moderates and the labour market loosens further over the coming year.

- Financial conditions continue to ease as wholesale and retail borrowing rates reprice to the lower OCR, contributing to gradually rising mortgage approvals and improving housing-related sentiment, although broader business credit growth remains patchy and sensitive to uncertainty about the durability of the recovery.

- Recent data confirm that GDP momentum is weak but not deteriorating as sharply as earlier in 2025, with high-frequency indicators pointing to a shallow recovery from a low base and ongoing headwinds from elevated living costs and fragile confidence weighing on discretionary consumption and investment.

- The MPC reiterated that external risks remain skewed to the downside, particularly from softer Chinese demand and uncertainty around United States trade policy, but noted that a lower New Zealand dollar continues to provide some offset via improved export competitiveness and support for tradables inflation.

- Looking ahead to early 2026, the Committee maintained a mild easing bias, indicating that a further cut toward 2.00–2.10% cannot be ruled out if activity fails to gain traction or if inflation undershoots projections, but current forecasts envisage the OCR remaining near 2.25% for an extended period provided inflation converges toward target and the recovery proceeds broadly as expected.

- The next meeting is on 18 February 2026.

Next 24 Hours Bias

Medium Bullish

The Japanese Yen (JPY)

Key news events today

No major news event

What can we expect from JPY today?

The yen is caught between cyclical support from an expected BoJ rate hike and structural headwinds from Japan’s fiscal expansion, entrenched carry trades, and still‑wide rate differentials. Near‑term direction is likely to be driven by the combination of BoJ communication on Friday and US inflation and labor data, with a clearly hawkish BoJ plus softer US prints needed to unlock any sustained downside in USD/JPY from the mid‑150s.

Central Bank Notes:

- The Policy Board of the Bank of Japan will meet on 18–19 December with markets almost fully pricing a 25-basis-point hike, which would raise the short-term policy rate from 0.50% to around 0.75%, as the bank moves further away from its ultra-loose stance while stressing that any tightening will remain gradual and data-dependent.

- The BOJ is expected to continue guiding the uncollateralized overnight call rate in a narrow band around the new policy rate, near 0.75%, while signaling that the pace and timing of any additional hikes will depend on how past increases affect bank lending, corporate financing conditions, and overall economic activity.

- The quarterly path of JGB purchases remains on a pre-announced, gradual taper: outright purchases are being reduced by about ¥400 billion per quarter through March 2026, then by roughly ¥200 billion per quarter from April to June 2026, with the bank still aiming for JGB purchases to settle near ¥2 trillion in Q1 2027 and retaining flexibility to adjust the pace if market functioning or yield volatility deteriorate.

- Japan’s economy has softened in the near term, with Q3 2025 GDP contracting at an annualized pace of about 2.3% as weaker residential investment and external demand weighed on activity, even as business sentiment in manufacturing has recently improved to a roughly four-year high.

- Core consumer inflation (excluding fresh food) accelerated to around 3.0% year-on-year in October, up from 2.9% in September and remaining above the BOJ’s 2% target, while the “core-core” measure excluding both fresh food and energy rose to about 3.1%, underscoring persistent underlying price pressures.

- In the very near term, some input-cost pressures are easing as earlier import price surges fade, but services inflation linked to labor shortages, along with steady wage gains, continues to support broader price momentum; firms’ and households’ medium-term inflation expectations remain anchored slightly above 2%, keeping short-term inflation risks tilted to the upside.

- For the coming quarters, the BOJ assesses that real growth will likely run below potential as the economy digests tighter financial conditions and past yen depreciation, though accommodative real rates, positive real wage growth, and improving corporate sentiment should help sustain a modest recovery in private consumption and business investment.

- Over the medium term, as overseas demand stabilizes and domestic labor markets remain tight, the BOJ expects wage settlements and inflation expectations to keep core inflation on a gradual upward trajectory around or slightly above 2%, providing room for further cautious rate normalization as long as financial conditions remain supportive and the recovery is not derailed.

- The next meeting is scheduled for 22 to 23 January 2026.

Next 24 Hours Bias

Medium Bearish

Oil

Key news events today

No major news event

What can we expect from Oil today?

Brent and WTI are trading around the low‑60s and high‑50s per barrel, respectively, with prices stabilizing after a modest rebound but still sitting near multi‑month lows due to a growing expectation of oversupply into 2026. Ongoing OPEC+ production increases, ample supply from sanctioned producers, and weakening demand signals from China are keeping the market skewed bearish despite occasional geopolitical flare‑ups.

Next 24 Hours Bias

Medium Bearish

The post IC Markets Global – Asia Fundamental Forecast | 18 December 2025 first appeared on IC Markets | Official Blog.

Thursday 18th December 2025: Asian Markets Slide as Tech Weakness and Inflation Caution Weigh on Sentiment

424682 December 18, 2025 15:39 ICMarkets Market News

Global Markets:

- Asian Stock Markets : Nikkei down -1.24%, Shanghai Composite up 0.16%, Hang Seng down -0.50% ASX down -0.19%

- Commodities : Gold at $4,363.35 (-0.23%), Silver at $66.605 (-0.46%), Brent Oil at $60.05 (0.62%), WTI Oil at $56.20 (0.70%)

- Rates : US 10-year yield at 4.140, UK 10-year yield at 4.4800, Germany 10-year yield at 2.8642

News & Data:

- (USD) Crude Oil Inventories -1.3M to -2.4M expected

Markets Update:

Asian markets are trading mostly lower on Thursday, tracking broadly negative cues from Wall Street overnight, as renewed concerns over lofty technology stock valuations weighed on sentiment following a sharp decline in the tech-heavy Nasdaq. Investors across the region remained cautious and refrained from taking major positions ahead of the release of key U.S. consumer price inflation data later in the day, which could influence expectations for the future path of interest rates. Asian markets had closed mixed in the previous session.

The Australian share market is modestly lower, extending losses for a fourth consecutive session. The benchmark S&P/ASX 200 has slipped well below the 8,600 level, dragged down by weakness in gold miners and technology stocks, even as performance across other sectors remains mixed. Major miners are showing selective strength, while oil stocks are trading unevenly. Technology shares are broadly under pressure, and gold miners are mostly lower amid soft bullion prices. Among individual stocks, Boss Energy has plunged sharply after flagging significant deviations from earlier forecasts for its Honeymoon project. The Australian dollar is hovering near US$0.660.

Japan’s market is also sharply lower, reversing the previous day’s gains, with losses led by index heavyweights and technology shares. Banking stocks are mixed, while exporters and industrial names are mostly weaker. Elsewhere in Asia, South Korea is down more than 1 percent, while most other regional markets are modestly lower or flat.

On Wall Street, U.S. stocks fell sharply, led by heavy losses in technology shares, while European markets ended mixed. Oil prices rebounded after geopolitical developments involving Venezuela boosted supply concerns.

Upcoming Events:

- 01:30 PM GMT – USD CPI y/y

- 01:30 PM GMT – USD Unemployment Claims

The post Thursday 18th December 2025: Asian Markets Slide as Tech Weakness and Inflation Caution Weigh on Sentiment first appeared on IC Markets | Official Blog.

Thursday 18th December 2025: Technical Outlook and Review

424669 December 18, 2025 15:39 ICMarkets Market News

DXY (U.S. Dollar Index):

Potential Direction: Bearish

Overall momentum of the chart: Bearish

The price could see a short-term pullback toward the pivot before continuing its bearish move down toward the 1st support.

Pivot: 98.77

Supporting reasons: Identified as a pullback resistance, where selling pressures could intensify and potentially cap any upward retracement.

1st support: 97.97

Supporting reasons: Identified as an overlap support that aligns with the 161.8% Fibonacci extension, indicating a potential area where the price could again stabilize.

1st resistance: 99.06

Supporting reasons: Identified as a pullback resistance, indicating a potential area that could halt any further upward movement

EUR/USD:

Potential Direction: Bullish

Overall momentum of the chart: Bearish

The price has already bounced off the pivot and may continue its bullish move toward the 1st resistance

Pivot: 1.1710

Supporting reasons: Identified as a pullback support, where renewed buying pressure could emerge to push the price higher.

1st support: 1.1644

Supporting reasons: Identified as a pullback support, indicating a potential level where the price could stabilize once again.

1st resistance: 1.1810

Supporting reasons: Identified as a swing high resistance that aligns closely with the 100% Fibonacci projection, indicating a potential level that could cap further upward movement.

EUR/JPY:

Potential Direction: Bullish

Overall momentum of the chart: Bullish

The price could see a short-term pullback toward the pivot before rising again toward the 1st resistance.

Pivot: 181.69

Supporting reasons: Identified as a pullback support that aligns with the 50% Fibonacci retracement, where renewed buying pressure could emerge to push the price higher.

1st support: 179.92

Supporting reasons: Identified as a pullback support, indicating a potential area where the price could again stabilize.

1st resistance: 183.02

Supporting reasons: Identified as a swing high resistance, indicating a potential level that could cap further upward movement.

EUR/GBP:

Potential Direction: Bullish

Overall momentum of the chart: Bullish

The price could see a short-term pullback toward the pivot before rising again toward the 1st resistance.

Pivot: 0.8749

Supporting reasons: Identified as a pullback support, where renewed buying pressure could emerge to push the price higher.

1st support: 0.8722

Supporting reasons: Identified as a multi-swing low support, indicating a potential area where the price could stabilize once more.

1st resistance: 0.8799

Supporting reasons: Identified as an overlap resistance, indicating a potential level that could cap further upward movement.

GBP/USD:

Potential Direction: Bullish

Overall momentum of the chart: Bullish

The price could see a short-term pullback toward the pivot before rising again toward the 1st resistance.

Pivot: 1.3294

Supporting reasons: Identified as a pullback support, where renewed buying pressure could emerge to push the price higher.

1st support: 1.3216

Supporting reasons: Identified as a pullback support, indicating a potential area where the price could stabilize once more.

1st resistance: 1.3452

Supporting reasons: Identified as a swing high resistance, indicating a potential level that could halt further upward movement.

GBP/JPY:

Potential Direction: Bullish

Overall momentum of the chart: Bullish

The price has already bounced off the pivot and may continue its bullish move toward the 1st resistance

Pivot: 207.17

Supporting reasons: Identified as an overlap resistance that aligns with the 50% Fibonacci retracement, where selling pressures could intensify and potentially cap any upward retracement

1st support: 205.32

Supporting reasons: Identified as an overlap support, indicating a potential level where the price could stabilize once more.

1st resistance: 208.94

Supporting reasons: Identified as a swing high resistance, indicating a potential level that could halt further upward movement.

USD/CHF:

Potential Direction: Bearish

Overall momentum of the chart: Bearish

The price could see a short-term pullback toward the pivot before continuing its bearish move down toward the 1st support.

Pivot: 0.7987

Supporting reasons: Identified as a pullback resistance, where selling pressures could intensify and potentially cap any upward retracement.

1st support: 0.7926

Supporting reasons: Identified as a pullback support that aligns with the 78.6% Fibonacci retracement, indicating a potential level where the price could stabilize once again.

1st resistance: 0.8028

Supporting reasons: Identified as a pullback resistance, indicating a potential level that could cap further upward movement.

USD/JPY:

Potential Direction: Bearish

Overall momentum of the chart: Bullish

The price has already reacted off the pivot and may continue its bearish move toward the 1st support.

Pivot: 155.79

Supporting reasons: Identified as an overlap resistance, where selling pressures could intensify and potentially cap any upward retracement

1st support: 154.44

Supporting reasons: Identified as an overlap support, indicating a strong area where buyers might return, and the price could stabilize once again.

1st resistance: 156.95

Supporting reasons: Identified as a swing high resistance. This level represents the next key area where upward movement could be capped amid increased selling pressure

USD/CAD:

Potential Direction: Bearish

Overall momentum of the chart: Bearish

The price could see a short-term pullback toward the pivot before continuing its bearish move down toward the 1st support.

Pivot: 1.3810

Supporting reasons: Identified as a pullback resistance, where selling pressures could intensify and potentially cap any upward retracement.

1st support: 1.3728

Supporting reasons: Identified as a swing low support, indicating a key level where the price could stabilize once more.

1st resistance: 1.3889

Supporting reasons: Identified as a pullback resistance, making it a possible target for bullish advances and a level where some sellers could return to cap gains

AUD/USD:

Potential Direction: Bearish

Overall momentum of the chart: Bullish

The price could see a short-term pullback toward the pivot before continuing its bearish move down toward the 1st support.

Pivot: 0.6622

Supporting reasons: Identified as a pullback resistance, where selling pressures could intensify and potentially cap any upward retracement.

1st support: 0.6572

Supporting reasons: Identified as a pullback support that aligns with the 38.6% Fibonacci retracement, this area has provided strong support historically and may attract buying interest for a potential short-term bounce

1st resistance: 0.6684

Supporting reasons: Identified as an overlap resistance, indicating a potential area that could halt any further upward movement.

NZD/USD

Potential Direction: Bearish

Overall momentum of the chart: Bullish

The price has already reacted off the pivot and may continue its bearish move toward the 1st support.

Pivot: 0.5796

Supporting reasons: Identified as an overlap resistance, where selling pressures could intensify and potentially cap any upward retracement.

1st support: 0.5743

Supporting reasons: Identified as a pullback support that aligns with the 38.2% Fibonacci retracement, this area has provided strong support historically and may attract buying interest for a potential short-term bounce

1st resistance: 0.5831

Supporting reasons: Identified as a swing high resistance, indicating a potential area that could halt any further upward movement.

US30 (DJIA):

Potential Direction: Bearish

Overall momentum of the chart: Bullish

The price could see a short-term pullback toward the pivot before continuing its bearish move down toward the 1st support.

Pivot: 48,009.51

Supporting reasons: Identified as a pullback resistance, where selling pressures could intensify and potentially cap any upward retracement.

1st support: 47,386.97

Supporting reasons: Identified as a pullback support, suggesting a potential area where the price could stabilize once again.

1st resistance: 48,879.50

Supporting reasons: Identified as a swing high resistance, indicating a potential area that could halt any further upward movement.

DE40 (DAX):

Potential Direction: Bullish

Overall momentum of the chart: Bullish

The price could see a short-term pullback toward the pivot before continuing its bearish move down toward the 1st support.

Pivot: 23,945.80

Supporting reasons: Identified as a pullback resistance, where selling pressures could intensify and potentially cap any upward retracement.

1st support: 23,488.00

Supporting reasons: Identified as a pullback support, indicating a key level where the price could stabilize once more.

1st resistance: 24,444.50

Supporting reasons: Identified as a swing high resistance that aligns with the 100% Fibonacci projection, indicating a potential area that could halt any further upward movement.

US500 (S&P 500):

Potential Direction: Bearish

Overall momentum of the chart: Bullish

The price could see a short-term pullback toward the pivot before continuing its bearish move down toward the 1st support.

Pivot: 6,773.23

Supporting reasons: Identified as a pullback resistance, where selling pressures could intensify and potentially cap any upward retracement.

1st support: 6,673.25

Supporting reasons: Identified as an overlap support that aligns with the 61.8% Fibonacci retracement, indicating a potential level where the price could stabilize once again.

1st resistance: 6,828.80

Supporting reasons: Identified as a pullback resistance, indicating a potential area that could halt any further upward movement.

BTC/USD (Bitcoin):

Potential Direction: Bearish

Overall momentum of the chart: Bearish

The price has already reacted off the pivot and may continue its bearish move toward the 1st support.

Pivot: 88,893.73

Supporting reasons: Identified as an overlap resistance, where selling pressures could intensify and potentially cap any upward retracement.

1st support: 81,604.89

Supporting reasons: Identified as a swing low support, indicating a potential level where the price could stabilize once more.

1st resistance: 94,626.23

Supporting reasons: Identified as an overlap resistance that aligns with the 50% Fibonacci retracement, indicating a potential area that could halt any further upward movement.

ETH/USD (Ethereum):

Potential Direction: Bearish

Overall momentum of the chart: Bullish

The price has already reacted off the pivot and may continue its bearish move toward the 1st support.

Pivot: 3,014.29

Supporting reasons: Identified as an overlap resistance, where selling pressures could intensify and potentially cap any upward retracement.

1st support: 2,740.05

Supporting reasons: Identified as a swing low support, indicating a potential level where the price could stabilize once more.

1st resistance: 3,206.26

Supporting reasons: Identified as a pullback resistance, indicating a potential area that could halt any further upward movement.

WTI/USD (Oil):

Potential Direction: Bearish

Overall momentum of the chart: Bullish

The price could see a short-term pullback toward the pivot before continuing its bearish move down toward the 1st support.

Pivot: 57.33

Supporting reasons: Identified as a pullback resistance, where selling pressures could intensify and potentially cap any upward retracement.

1st support: 55.04

Supporting reasons: Identified as a swing low support that aligns with the 161.8%% Fibonacci extension and the 100% Fibonacci projection, indicating a key level where the price could stabilize once more.

1st resistance: 58.55

Supporting reasons: Identified as a pullback resistance, indicating a potential area that could halt any further upward movement.

XAU/USD (GOLD):

Potential Direction: Bullish

Overall momentum of the chart: Bullish

The price could see a short-term pullback toward the pivot before rising again toward the 1st resistance.

Pivot: 4,255.04

Supporting reasons: Identified as a pullback support, where renewed buying pressure could emerge to push the price higher.

1st support: 4,145.75

Supporting reasons: Identified as a pullback support, indicating a key level where the price could stabilize once more.

1st resistance: 4,366.45

Supporting reasons: Identified as a swing high resistance that aligns with the 161.8% Fibonacci extension, indicating a potential area that could halt any further upward movement.

The accuracy, completeness and timeliness of the information contained on this site cannot be guaranteed. IC Markets Global does not warranty, guarantee or make any representations, or assume any liability regarding financial results based on the use of the information in the site.

News, views, opinions, recommendations and other information obtained from sources outside of www.icmarkets.com, used in this site are believed to be reliable, but we cannot guarantee their accuracy or completeness. All such information is subject to change at any time without notice. IC Markets Global assumes no responsibility for the content of any linked site.

The fact that such links may exist does not indicate approval or endorsement of any material contained on any linked site. IC Markets Global is not liable for any harm caused by the transmission, through accessing the services or information on this site, of a computer virus, or other computer code or programming device that might be used to access, delete, damage, disable, disrupt or otherwise impede in any manner, the operation of the site or of any user’s software, hardware, data or property.

The post Thursday 18th December 2025: Technical Outlook and Review first appeared on IC Markets | Official Blog.

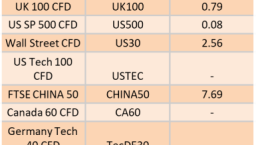

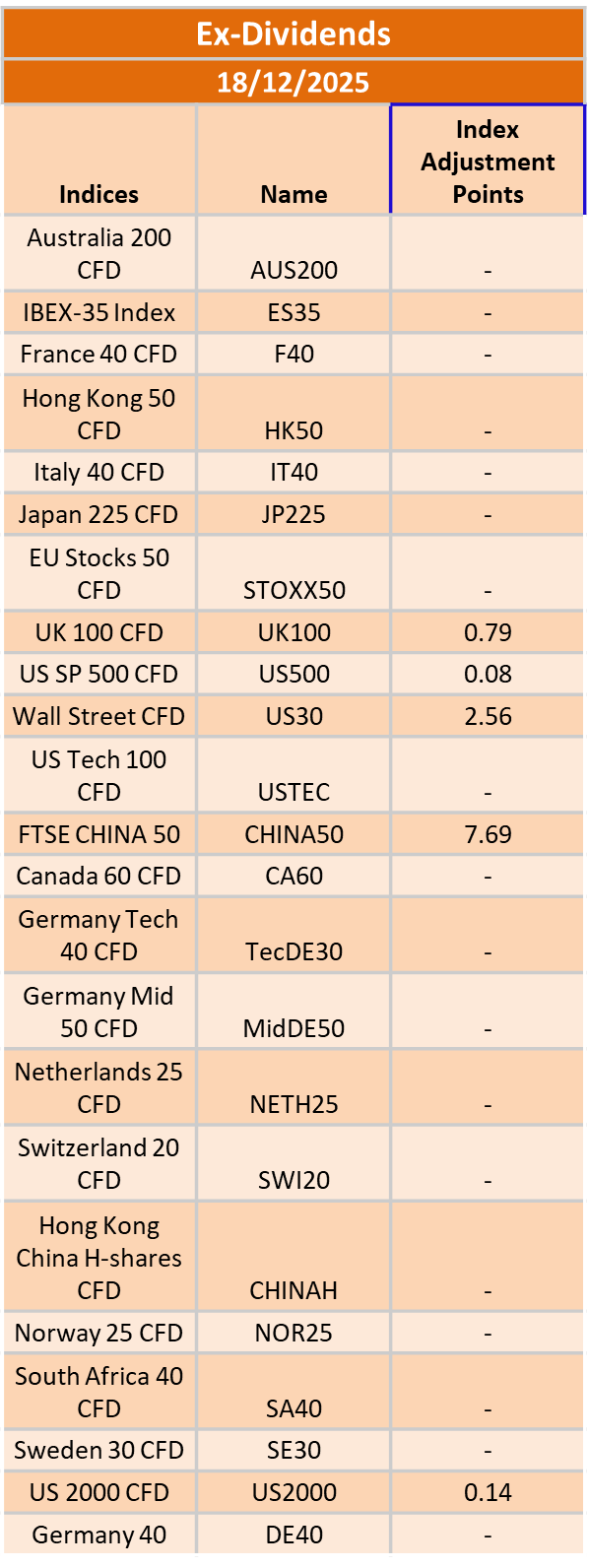

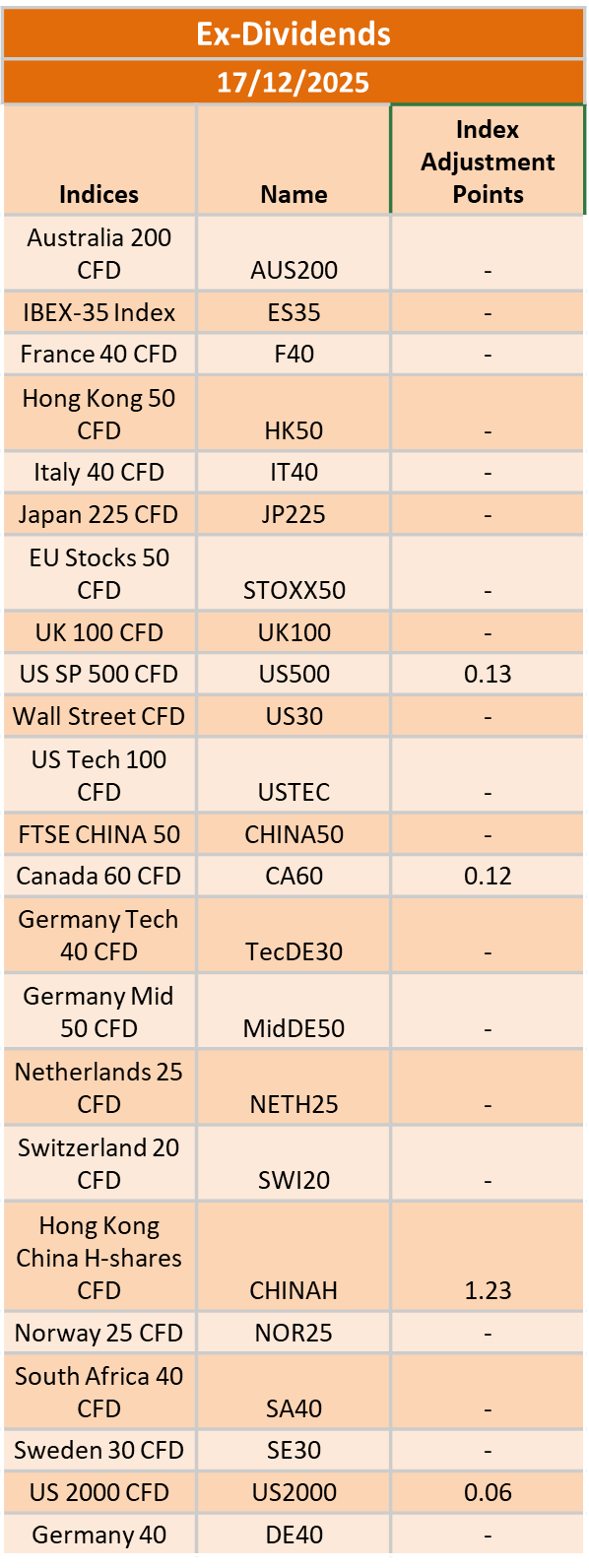

Ex-Dividend 18/12/2025

424663 December 18, 2025 10:39 ICMarkets Market News

The post Ex-Dividend 18/12/2025 first appeared on IC Markets | Official Blog.

General Market Analysis – 17/12/25

424648 December 17, 2025 17:00 ICMarkets Market News

US Stocks Mixed After Employment Update – Dow off 0.6%

US equity markets were mixed overnight as investors worked through delayed employment data released following the government shutdown, which delivered conflicting signals on labour market momentum. The Dow Jones fell 0.62% to close at 48,114, while the S&P 500 eased 0.24% to 6,800. In contrast, the Nasdaq edged 0.23% higher to finish at 23,111. Non-Farm Payrolls data had slumped sharply in October during the height of the shutdown before rebounding strongly in November to exceed most expectations. The DXY slipped 0.10% on the day to 98.21, having initially dropped harder on the initial data. In rates markets, the 2-year Treasury yield fell 1.4 basis points to 3.487%, while the 10-year lost 2.7 basis points to move back down to 4.145%. Oil prices took another step lower to hit levels not seen for nearly five years. Brent dropped 2.82% to $58.85 a barrel, while WTI slid 2.90% to $55.19. Markets continue to price in persistent oversupply into next year, while growing optimism around a potential peace agreement in Ukraine added further downside pressure. Gold was little changed on the session, easing 0.06% to $4,302.32 an ounce, though the metal continues to find solid support on dips amid the current macro environment.

Market Remains More Dovish than the Fed

Global markets remain much more dovish than the Fed in current conditions, with the overall market pricing in 58 basis points of rate cuts from the world’s biggest central bank in 2026, while the clear message from Jerome Powell was that the FOMC has just one 25 basis point cut on the calendar in the coming 12 months. Last night’s data had the market pricing in a chance of a hold in January more strongly, up to 75% from 70% before the numbers, but it is the divergence further out that could see moves in the market. Of course, a lot of the longer-dated market pricing has a new Chairman factored in who is likely to be more dovish, in line with the President’s wishes, so that situation is likely to add volatility in the coming months. We have key CPI data out tomorrow, and that could be telling for the shorter term, as we have clear indications from FOMC members that they consider inflation to be too sticky at the moment. If CPI remains at elevated levels, it could push those rate cut expectations further down the curve.

Quieter Calendar Day Ahead for Traders

Looking ahead, it is a relatively quiet day on the macroeconomic calendar today, though traders will be monitoring price action following the US overnight session and key data updates from there. There is little on the calendar in the Asian session today; however, UK markets will be back in focus early in the European session with key CPI data due out. Expectations are for a 3.5% year-on-year print, which is still high, just a day ahead of the crucial Bank of England rate call tomorrow. Germany’s IFO Business Climate survey is due out later in the session (exp. 88.2), but expect that UK data to dominate. In the US session, we have the usual weekly crude oil inventory data (exp. -2.4 mio) scheduled, but expect comments from Fed members Waller, Williams, and Bostic to move markets as we progress through the session.

The post General Market Analysis – 17/12/25 first appeared on IC Markets | Official Blog.

Wednesday 17th December 2025: Technical Outlook and Review

424630 December 17, 2025 16:39 ICMarkets Market News

DXY (U.S. Dollar Index):

Potential Direction: Bearish

Overall momentum of the chart: Bearish

The price could see a short-term pullback toward the pivot before continuing its bearish move down toward the 1st support.

Pivot: 98.77

Supporting reasons: Identified as a pullback resistance, where selling pressures could intensify and potentially cap any upward retracement.

1st support: 97.97

Supporting reasons: Identified as an overlap support that aligns with the 161.8% Fibonacci extension, indicating a potential area where the price could again stabilize.

1st resistance: 99.06

Supporting reasons: Identified as a pullback resistance, indicating a potential area that could halt any further upward movement

EUR/USD:

Potential Direction: Bullish

Overall momentum of the chart: Bearish

The price could see a short-term pullback toward the pivot before rising again toward the 1st resistance.

Pivot: 1.1710

Supporting reasons: Identified as a pullback support, where renewed buying pressure could emerge to push the price higher.

1st support: 1.1644

Supporting reasons: Identified as a pullback support, indicating a potential level where the price could stabilize once again.

1st resistance: 1.1810

Supporting reasons: Identified as a swing high resistance that aligns closely with the 100% Fibonacci projection, indicating a potential level that could cap further upward movement.

EUR/JPY:

Potential Direction: Bullish

Overall momentum of the chart: Bullish

The price could see a short-term pullback toward the pivot before rising again toward the 1st resistance.

Pivot: 181.69

Supporting reasons: Identified as a pullback support that aligns with the 50% Fibonacci retracement, where renewed buying pressure could emerge to push the price higher.

1st support: 179.92

Supporting reasons: Identified as a pullback support, indicating a potential area where the price could again stabilize.

1st resistance: 183.02

Supporting reasons: Identified as a swing high resistance, indicating a potential level that could cap further upward movement.

EUR/GBP:

Potential Direction: Bullish

Overall momentum of the chart: Bullish

The price could see a short-term pullback toward the pivot before rising again toward the 1st resistance.

Pivot: 0.8749

Supporting reasons: Identified as a pullback support, where renewed buying pressure could emerge to push the price higher.

1st support: 0.8722

Supporting reasons: Identified as a multi-swing low support, indicating a potential area where the price could stabilize once more.

1st resistance: 0.8799

Supporting reasons: Identified as an overlap resistance, indicating a potential level that could cap further upward movement.

GBP/USD:

Potential Direction: Bullish

Overall momentum of the chart: Bullish

The price could see a short-term pullback toward the pivot before rising again toward the 1st resistance.

Pivot: 1.3353

Supporting reasons: Identified as a pullback support, where renewed buying pressure could emerge to push the price higher.

1st support: 1.3287

Supporting reasons: Identified as an overlap support, indicating a potential area where the price could stabilize once more.

1st resistance: 1.3452

Supporting reasons: Identified as a swing high resistance, indicating a potential level that could halt further upward movement.

GBP/JPY:

Potential Direction: Bullish

Overall momentum of the chart: Bullish

The price has already bounced off the pivot and may continue its bullish move toward the 1st resistance

Pivot: 207.17

Supporting reasons: Identified as an overlap resistance that aligns with the 50% Fibonacci retracement, where selling pressures could intensify and potentially cap any upward retracement

1st support: 205.32

Supporting reasons: Identified as an overlap support, indicating a potential level where the price could stabilize once more.

1st resistance: 208.94

Supporting reasons: Identified as a swing high resistance, indicating a potential level that could halt further upward movement.

USD/CHF:

Potential Direction: Bearish

Overall momentum of the chart: Bearish

The price could see a short-term pullback toward the pivot before continuing its bearish move down toward the 1st support.

Pivot: 0.7987

Supporting reasons: Identified as a pullback resistance, where selling pressures could intensify and potentially cap any upward retracement.

1st support: 0.7926

Supporting reasons: Identified as a pullback support that aligns with the 78.6% Fibonacci retracement, indicating a potential level where the price could stabilize once again.

1st resistance: 0.8028

Supporting reasons: Identified as a pullback resistance, indicating a potential level that could cap further upward movement.

USD/JPY:

Potential Direction: Bearish

Overall momentum of the chart: Bullish

The price has already reacted off the pivot and may continue its bearish move toward the 1st support.

Pivot: 155.34

Supporting reasons: Identified as an overlap resistance, where selling pressures could intensify and potentially cap any upward retracement

1st support: 153.75

Supporting reasons: Identified as a swing low support that aligns closely with the 127.2% Fibonacci projection, indicating a strong area where buyers might return, and the price could stabilize once again.

1st resistance: 156.95

Supporting reasons: Identified as a swing high resistance. This level represents the next key area where upward movement could be capped amid increased selling pressure

USD/CAD:

Potential Direction: Bearish

Overall momentum of the chart: Bearish

The price could see a short-term pullback toward the pivot before continuing its bearish move down toward the 1st support.

Pivot: 1.3810

Supporting reasons: Identified as a pullback resistance, where selling pressures could intensify and potentially cap any upward retracement.

1st support: 1.3728

Supporting reasons: Identified as a swing low support, indicating a key level where the price could stabilize once more.

1st resistance: 1.3889

Supporting reasons: Identified as a pullback resistance, making it a possible target for bullish advances and a level where some sellers could return to cap gains

AUD/USD:

Potential Direction: Bullish

Overall momentum of the chart: Bullish

The price could see a short-term pullback toward the pivot before rising again toward the 1st resistance.

Pivot: 0.6622

Supporting reasons: Identified as an overlap support that aligns with the 23.6% Fibonacci retracement, where renewed buying pressure could emerge to push the price higher.

1st support: 0.6572

Supporting reasons: Identified as a pullback support that aligns with the 38.6% Fibonacci retracement, this area has provided strong support historically and may attract buying interest for a potential short-term bounce

1st resistance: 0.6684

Supporting reasons: Identified as an overlap resistance that aligns with the 161.8% Fibonacci extension, indicating a potential area that could halt any further upward movement.

NZD/USD

Potential Direction: Bearish

Overall momentum of the chart: Bullish

The price has already reacted off the pivot and may continue its bearish move toward the 1st support.

Pivot: 0.5796

Supporting reasons: Identified as an overlap resistance, where selling pressures could intensify and potentially cap any upward retracement.

1st support: 0.5743

Supporting reasons: Identified as a pullback support that aligns with the 38.2% Fibonacci retracement, this area has provided strong support historically and may attract buying interest for a potential short-term bounce

1st resistance: 0.5831

Supporting reasons: Identified as a swing high resistance, indicating a potential area that could halt any further upward movement.

US30 (DJIA):

Potential Direction: Bullish

Overall momentum of the chart: Bullish

The price could see a short-term pullback toward the pivot before rising again toward the 1st resistance.

Pivot: 48,000

Supporting reasons: Identified as a pullback support that aligns with the 61.8% Fibonacci retracement, where renewed buying pressure could emerge to push the price higher.

1st support: 47,372.40

Supporting reasons: Identified as a pullback support, suggesting a potential area where the price could stabilize once again.

1st resistance: 48,879.50

Supporting reasons: Identified as a swing high resistance, indicating a potential area that could halt any further upward movement.

DE40 (DAX):

Potential Direction: Bullish

Overall momentum of the chart: Bullish

The price could see a short-term pullback toward the pivot before rising again toward the 1st resistance.

Pivot: 23,945.80

Supporting reasons: Identified as a pullback support, where renewed buying pressure could emerge to push the price higher.

1st support: 23,488.00

Supporting reasons: Identified as a pullback support, indicating a key level where the price could stabilize once more.

1st resistance: 24,444.50

Supporting reasons: Identified as a swing high resistance that aligns with the 100% Fibonacci projection, indicating a potential area that could halt any further upward movement.

US500 (S&P 500):

Potential Direction: Bullish

Overall momentum of the chart: Bullish

The price could see a short-term pullback toward the pivot before rising again toward the 1st resistance.

Pivot: 6,773.23

Supporting reasons: Identified as a pullback support that aligns with the 38.2% Fibonacci retracement, where renewed buying pressure could emerge to push the price higher.

1st support: 6,673.25

Supporting reasons: Identified as an overlap support that aligns with the 61.8% Fibonacci retracement, indicating a potential level where the price could stabilize once again.

1st resistance: 6,920.20

Supporting reasons: Identified as a swing high resistance, indicating a potential area that could halt any further upward movement.

BTC/USD (Bitcoin):

Potential Direction: Bearish

Overall momentum of the chart: Bearish

The price could see a short-term pullback toward the pivot before continuing its bearish move down toward the 1st support.

Pivot: 88,893.73

Supporting reasons: Identified as a pullback resistance, where selling pressures could intensify and potentially cap any upward retracement.

1st support: 81,604.89

Supporting reasons: Identified as a swing low support, indicating a potential level where the price could stabilize once more.

1st resistance: 94,626.23

Supporting reasons: Identified as an overlap resistance that aligns with the 50% Fibonacci retracement, indicating a potential area that could halt any further upward movement.

ETH/USD (Ethereum):

Potential Direction: Bearish

Overall momentum of the chart: Bullish

The price could see a short-term pullback toward the pivot before continuing its bearish move down toward the 1st support.

Pivot: 3,180.10

Supporting reasons: Identified as an overlap resistance, where selling pressures could intensify and potentially cap any upward retracement.

1st support: 2,904.01

Supporting reasons: Identified as an overlap support that aligns with the 61.8% Fibonacci projection, indicating a potential level where the price could stabilize once more.

1st resistance: 3,404.43

Supporting reasons: Identified as an overlap resistance, indicating a potential area that could halt any further upward movement.

WTI/USD (Oil):

Potential Direction: Bearish

Overall momentum of the chart: Bullish

The price could see a short-term pullback toward the pivot before continuing its bearish move down toward the 1st support.

Pivot: 57.33

Supporting reasons: Identified as a pullback resistance, where selling pressures could intensify and potentially cap any upward retracement.

1st support: 55.04

Supporting reasons: Identified as a swing low support that aligns with the 161.8%% Fibonacci extension and the 100% Fibonacci projection, indicating a key level where the price could stabilize once more.

1st resistance: 58.55

Supporting reasons: Identified as a pullback resistance, indicating a potential area that could halt any further upward movement.

XAU/USD (GOLD):

Potential Direction: Bullish

Overall momentum of the chart: Bullish

The price could see a short-term pullback toward the pivot before rising again toward the 1st resistance.

Pivot: 4,255.04

Supporting reasons: Identified as a pullback support, where renewed buying pressure could emerge to push the price higher.

1st support: 4,145.75

Supporting reasons: Identified as a pullback support, indicating a key level where the price could stabilize once more.

1st resistance: 4,366.45

Supporting reasons: Identified as a swing high resistance that aligns with the 161.8% Fibonacci extension, indicating a potential area that could halt any further upward movement.

The accuracy, completeness and timeliness of the information contained on this site cannot be guaranteed. IC Markets Global does not warranty, guarantee or make any representations, or assume any liability regarding financial results based on the use of the information in the site.

News, views, opinions, recommendations and other information obtained from sources outside of www.icmarkets.com, used in this site are believed to be reliable, but we cannot guarantee their accuracy or completeness. All such information is subject to change at any time without notice. IC Markets Global assumes no responsibility for the content of any linked site.

The fact that such links may exist does not indicate approval or endorsement of any material contained on any linked site. IC Markets Global is not liable for any harm caused by the transmission, through accessing the services or information on this site, of a computer virus, or other computer code or programming device that might be used to access, delete, damage, disable, disrupt or otherwise impede in any manner, the operation of the site or of any user’s software, hardware, data or property.

The post Wednesday 17th December 2025: Technical Outlook and Review first appeared on IC Markets | Official Blog.

IC Markets Global – Asia Fundamental Forecast | 17 December 2025

424629 December 17, 2025 16:39 ICMarkets Market News

IC Markets Global – Asia Fundamental Forecast | 17 December 2025

What happened in the U.S. session?

Overnight U.S. trading was dominated by macro signals that the economy is cooling but not collapsing: the November jobs report showed rising unemployment alongside modest job creation, and flash PMIs pointed to the slowest business‑activity growth in six months. This mix pushed investors into a more defensive stance, softening the dollar, nudging Treasury yields lower, and weighing on major equity indices, while safe‑haven assets like gold and, to a lesser degree, high‑quality bonds saw support.

What does it mean for the Asia Session?

Across the Asian Wednesday session and into Europe, the focus is on a dense UK and Eurozone inflation docket, the German Ifo survey, and Indonesia’s policy decision, all of which will shape moves in GBP, EUR, and regional EM FX. As the trading day rolls into New York, attention shifts to multiple Fed speeches, U.S. mortgage statistics, and DOE inventory releases that can sway U.S. yields, the dollar, and crude benchmarks.

The Dollar Index (DXY)

Key news events today

FOMC Member Waller Speaks (1:15 pm GMT)

What can we expect from DXY today?

Today’s dollar trade on Wednesday is characterized by consolidation near two‑month lows within a broader downtrend driven by softer U.S. data and firm expectations of further Fed rate cuts. The currency continues to underperform against higher‑yielding and risk‑sensitive peers such as the Australian and New Zealand dollars, while traditional safe‑havens like the yen and Swiss franc remain supported following the recent Fed‑induced slide.

Central Bank Notes:

- The Federal Open Market Committee (FOMC) is widely expected to lower the federal funds rate target range by 25 basis points to 3.50%–3.75% at its December 9–10, 2025, meeting, marking the third consecutive cut after the October reduction to 3.75%–4.00%

- The Committee continues to pursue maximum employment and 2% inflation goals, with the labor market showing further softening as the unemployment rate rose to 4.4% in September 2025 amid modest job gains.

- Officials note persistent downside risks to growth alongside resilient activity, with inflation easing to 3.0% year-over-year CPI in September but remaining elevated due to tariff effects; core PCE stands at around 2.8% as of October.

- Economic activity grew at a 3.8% annualized pace in Q2 2025 per revised estimates, though Q3 and Q4 face headwinds from trade tensions, fiscal restraint, and data disruptions like the government shutdown.

- September’s Summary of Economic Projections forecasts 2025 unemployment at a median 4.5%, with PCE inflation near 3.0% and core PCE at 3.1%, signaling a gradual disinflation path; updates expected on December 10 may adjust for higher unemployment and lower growth.

- The Committee maintained its data-dependent approach, noting a softening labor market and inflation above the 2% target, while deciding to lower the federal funds rate target range by 25 basis points to 3.50%-3.75%. Dissent persisted, with multiple members opposing the cut or advocating for a hold, reflecting divisions similar to recent meetings.

- The FOMC confirmed the conclusion of its quantitative tightening program effective December 1, 2025, with Treasury rolloff caps at $5 billion per month and agency MBS caps at $35 billion per month to ensure ample reserves and market stability.

- The next meeting is scheduled for 27 to 28 January 2026.

Next 24 Hours Bias

Medium Bearish

Gold (XAU)

Key news events today

FOMC Member Waller Speaks (1:15 pm GMT)

What can we expect from Gold today?

Gold is consolidating just above the 4,300 USD/oz area today, holding near recent record territory after this year’s powerful precious‑metals rally. Price action is relatively contained as traders balance ongoing support from low real yields and geopolitical risks against profit‑taking near all‑time highs and event risk around upcoming Federal Reserve decisions.

Next 24 Hours Bias

Strong Bullish

The Australian Dollar (AUD)

Key news events today

No major news event

What can we expect from AUD today?

The Australian Dollar is trading slightly weaker but not collapsing, as mixed domestic data, soft Chinese momentum, and a tentative global risk tone offset support from relatively high Australian rates and a hawkish RBA. AUD/USD remains confined to a tight range near 0.66–0.67, with markets looking to forthcoming Australian figures and major U.S. data to determine whether the next leg is a break lower toward 0.6550 or a recovery back toward recent highs.

Central Bank Notes:

- The Reserve Bank of Australia held its cash rate steady at 3.60% at the November 2025 policy meeting, adopting a cautious tone amid a surprise uptick in inflation data for the September quarter. This marks the fourth consecutive pause since the 25 basis point cut in August. The Board attributed some of the inflation rise to temporary factors like higher petrol prices and council rates, but noted signs of more persistent pressures from consumer demand.

- Policymakers emphasized vigilance on inflation, with trimmed mean inflation expected to remain elevated in the near term before nearing the 2–3% target midpoint by mid-2027. Recent data showed underlying inflation staying above target until at least the second half of 2026, prompting upward revisions to forecasts. Capacity pressures are seen as slightly more pronounced than previously assessed, delaying any easing.

- Headline CPI for the September quarter exceeded expectations, driven partly by temporary items, while underlying measures signal ongoing stickiness. The shift to monthly CPI reporting, with the first full edition in November 2025, will enhance real-time inflation monitoring. Housing and services remain resilient contributors to price pressures.

- Domestic demand shows firmness in services alongside below-trend growth elsewhere, with capacity pressures not expected to ease significantly. The labor market is gradually softening, with unemployment projected to stabilize around 4.4%, though wage growth and productivity dynamics keep unit labor costs a concern. Household spending faces headwinds from high borrowing costs.

- Global risks include geopolitical tensions and commodity volatility, set against modestly revised-up world growth outlooks. The Board describes its policy as mildly restrictive and data-dependent, balancing inflation control with employment goals. No rate hike was considered despite the inflation surprise.