Articles

EIA weekly crude oil inventories -3832K vs +447K expected

January 7, 2026 22:39 Forexlive Latest News Market News

- Prior was -1934K

- Gasoline +7702K vs +3186K exp

- Distillates +5594K vs +2109K exp

The private data released late yesterday showed:

- Crude -2.8m

- Gasoline +4.4m

- Distillates +4.9m

Given the private numbers, the official report isn’t a big surprise but it’s still bearish. Yes, there was a headline draw in crude but those are big builds in products that are going to weigh on crude demand going forward.

WTI crude oil is down 80-cents to $56.34 today. IT touched as low as $55.76 today, which is the lowest since Dec 17 and close to last year’s low of $55.00.

For background:

The EIA weekly crude oil report—formally the US Energy Information Administration’s “weekly petroleum status report”—is one of the most market-moving snapshots of near-term oil fundamentals. Released weekly, it estimates changes in US crude oil inventories (commercial stocks), often with special focus on the cushing, oklahoma delivery hub for wti, plus key balances like imports, exports, and refinery utilization. Traders also watch the supply side: estimated domestic crude production, adjustments tied to measurement/timing issues, and flows into or out of the strategic petroleum reserve when applicable.

Importantly, the report doesn’t just cover crude. It includes gasoline and distillate inventories, refinery runs, and “product supplied” figures that function as a real-time proxy for demand. Because the US is both a major producer and exporter, swings in net exports or refinery runs can dominate the weekly crude stock change, so markets look through the headline build/draw to the drivers underneath.

The numbers are estimates based on weekly surveys and statistical techniques, so they can be noisy and occasionally revised as more complete data arrives, but the report remains a key, high-frequency read on whether the physical market is tightening or loosening.

This article was written by Adam Button at investinglive.com.

US October factory orders -1.3% vs -1.2% expected

January 7, 2026 22:14 Forexlive Latest News Market News

- Prior was +0.2%

This is a badly dated report due to the US government shutdown.

The US factory orders report (officially “manufacturers’ shipments, inventories, and orders”) is a monthly census bureau release that tracks how much US manufacturers receive in new orders, ship out, and hold in inventories. markets watch it as a pulse on goods demand and the manufacturing pipeline, often splitting it into durable goods (long-lasting items like machinery, vehicles, and aircraft) and nondurable goods (short-lived items like food and chemicals). a key feature is that factory orders incorporates and finalizes the prior month’s advance durable goods report: the durable-goods totals and many major categories can be revised, sometimes meaningfully, as more complete company responses arrive. that matters because the headline durable-goods number often drives initial market moves. the factory orders release also adds the nondurable side and provides a fuller picture via shipments and inventories, helping investors gauge momentum, backlog dynamics, and inventory swings.

This article was written by Adam Button at investinglive.com.

December ISM services 54.5 vs 52.3 expected

January 7, 2026 22:14 Forexlive Latest News Market News

Highest reading since October 2024

- Business activity index 54.4 vs 52.6 prior

- Employment 52.0 vs 48.9

- New orders57.9 vs 52.9 prior

- Prices paid 64.3 vs 65.4 prior

- Supplier deliveries51.8 vs 54.1 prior

- Inventories54.1 vs 54.8 prior

- Backlog of orders 42.6 vs 49.1 prior

- New export orders 54.2 vs 48.7 prior

- Imports 50.3 vs 48.9 prior

- Inventory sentiment 54.1 54.8 prior

Justin wrote a great preview for this report earlier. There has been some recovery in this report since September but it’s generally been rangebound over the past two years.

Comments in the report:

- “We continue to experience higher prices, primarily due to the

impact of the administration’s trade and tariff policies. We are

disproportionately impacted by importing seafood from Southeast Asia and

coffee from South America.” [Accommodation & Food Services] - “In general, business is flat. Value brands are still experiencing

higher demand. But premium brands struggle to maintain market share.”

[Agriculture, Forestry, Fishing & Hunting] - “Rising labor and staffing shortages across facilities and auxiliary

services, increasing regulatory and compliance requirements within the

state, continued inflationary pressure on supplies and contracted

services, ongoing supply-chain variability for specialized equipment and

materials, heightened sustainability expectations and state-led

environmental initiatives, fluctuations in enrollment affecting

institutional budgets and purchasing volumes, and increased competition

and pricing volatility in the regional supplier market.” [Educational

Services] - “Overall, business is healthy, most of our purchasing is staying

consistent, and we are renewing most contracts as we head into the new

year.” [Finance & Insurance] - “Flu cases on the rise; the vaccine is not of much help this year.

Respiratory equipment and supplies are seeing a surge in demand.”

[Health Care & Social Assistance] - “Annual pricing markups from key service and data providers are

higher than they’ve been for many years — gradually drives costs up.”

[Information] - “Continuing uncertainty and apprehension regarding tariffs and the resulting impact on pricing.” [Public Administration]

- “We expect flat national home prices in 2026, with a forecast of a

0.5-percent increase and a plausible range from a decrease of 3.6

percent to a gain of 4.6 percent. Many metro areas across the country

are already posting year-over-year declines, making 2026 the most likely

year since 2010 for a modest national price dip.” [Real Estate, Rental

& Leasing] - “High business activity due to the holiday season.” [Transportation & Warehousing]

- “Year-over-year growth has been coming down for the last three

months. Most likely, the government shutdown was a contributor.”

[Wholesale Trade]

This article was written by Adam Button at investinglive.com.

JOLTS job openings for November 7.146M vs 7.600M estimate.

January 7, 2026 22:14 Forexlive Latest News Market News

-

Prior month revised: Job openings 7.449M (revised down -221K from 7.670M)

-

JOLTS job openings: 7.145M, that is down -885K YoY

-

Job openings rate: 4.3%, little changed

-

November hires were little changed, holding at 5.1M

-

The hires rate remained steady at 3.2%

-

Hires decreased in:

-

State & local government ex-education (-39K)

-

State & local government education (-31K)

-

-

Hires increased in:

-

Federal government (+11K)

-

-

No significant hiring shifts occurred across most major industries

-

In November, total separations were unchanged at 5.1M with a 3.2% rate

-

Total separations decreased in:

-

State & local government ex-education (-27K)

-

-

Quits were little changed at 3.2M with a 2.0% rate

-

Quits increased in:

-

Accommodation & food services (+208K)

-

-

Layoffs and discharges were little changed at 1.7M with a 1.1% rate

-

Layoffs and discharges decreased in:

-

Accommodation & food services (-107K)

-

Health care & social assistance (-52K)

-

State & local government ex-education (-26K)

-

-

Other separations were little changed at 232K, marking a series low

-

Establishment size:

-

1–9 employees and 5,000+ employees saw little or no change in job openings, hires, or separations

-

The quick takeaway:The November JOLTS report reinforces the theme of a cooling but still orderly labor market, with job openings holding at 7.146M but continuing their clear downtrend year-over-year, signaling reduced labor demand without a sharp deterioration.

Hires and total separations both stuck at 5.1M ironically underscore a labor market that is neither accelerating nor cracking (no hire/no fire). However, the quits rate at 2.0%—well below cycle highs—points to diminished worker bargaining power and less confidence in job switching.

Importantly for rates markets, layoffs remain contained and other separations hit a series low, arguing against imminent labor stress.

For traders, the data supports a “soft-landing” narrative, limiting urgency for aggressive Fed easing near term while keeping the door open for gradual policy normalization if disinflation continues—leaving USD and yields sensitive to upcoming inflation and payroll data rather than JOLTS alone.

Looking at yields:

- 2-year yield 3.465%, -0.8 basis points

- 10 year yield 4.151%, -2.7 basis points

- 30 year yield 4.837%, -2.9 basis points

This article was written by Greg Michalowski at investinglive.com.

ADP December national employment +41K vs +47K expected

January 7, 2026 20:30 Forexlive Latest News Market News

- Prior was -32K

- Goods-3K versus -19K last month

- Service +44K versus -13K last month

- small business +9K vs -120K prior (6 of the last 7 months have been negative)

- medium businesses +34K vs +51K last month

- large businesses +2K vs +39K last month

- Wages for job stayers +4.4% vs +4.5% last month

- Wages for job changers 6.6% vs 6.3% last month

The initial market reaction to the report has been mum but we’ve seen some small bids in bonds.

“Small establishments recovered from November job losses with positive end-of-year hiring, even as large

employers pulled back,” said Dr. Nela Richardson, chief economist, ADP

Sector changes.

- Education and health +39K vs +30K prior

- Leisure hospitality +24K vs +13K prior

- Trade transportation and utilities +11K vs +1K prior

- Financial activities +6K vs -9K prior

- Professional business services -29K vs- 26K prior

AI is coming for the ‘professional business services’ jobs first. As for much of the year, it’s been government-related healthcare jobs holding up while private sector jobs struggle.

The next Bureau of Labor Statistics (BLS) non-farm payrolls report (Employment Situation) is scheduled for Friday, January 9 at 8:30 am ET as we slowly catch up on economic data after the US government shutdown. The bad news is that there is already talk of another shutdown.

This article was written by Adam Button at investinglive.com.

investingLive European markets wrap: Dollar steady ahead of ADP, precious metals cool off

January 7, 2026 20:14 Forexlive Latest News Market News

Headlines:

- Friday could be an important day for silver: double top or new record highs?

- Big risks for gold on Friday with US NFP and US Supreme Court on the agenda

- Dollar hangs in the balance as Trump obsesses over Greenland next

- DAX 40 rises to new record highs amid positive risk sentiment, softer inflation data

- Latest Australian inflation data keeps February interest rate hike on the table

- Eurozone December preliminary CPI +2.0% vs +2.0% y/y expected

- Germany November retail sales -0.6% vs +0.2% m/m expected

- German construction activity returns to growth at end of 2025

- French consumer confidence rises slightly in December

- UK December construction PMI 40.1 vs 42.5 expected

- China gold reserves continue to climb, up for a 14th month running

Markets:

- USD mixed, overall FX little changed

- European equities lower; S&P 500 futures down 0.1%

- US 10-year yields down 3.7 bps to 4.141%

- Gold down 1.1% to $4,447.09

- WTI crude flat at $57.01

- Bitcoin down 1.4% to $91,948

There wasn’t too much in the headlines in European trading today. The handover from Asia saw a higher Australian dollar after the softer but stickier inflation data, reaffirming the potential for a rate hike by the RBA in February. However, those gains fizzled out during the session with AUD/USD dropping off from 0.6760 to 0.6730 levels currently to stay flattish on the day.

We also got the Eurozone inflation data for December and that continues to reaffirm the ECB’s position to keep on the sidelines for the most part. So, there’s nothing new on that front.

Instead, the most notable action is a bit of a breather in the hot start to the year for precious metals. Gold is down over 1% to $4,447 while silver is down over 3% to $78.55 on the day as the bulls hit pause.

This as the risk rally also starts to flatten out a bit with US futures and European indices posting slight losses on the day. The market attention now slowly shifts to US labour market data, with the main event of the week being the non-farm payrolls release on Friday.

In FX, major currencies weren’t up to much with the dollar holding in a smaller range and trading little changed across the board. The aussie was the only notable mover early on but as mentioned above, things just fizzled out after.

Besides that, there is still some eyes on geopolitical risks with Trump taking aim at Greenland next. So, that will be something to be mindful about in the weeks to come.

Otherwise, it’s on to the ADP roulette next.

This article was written by Justin Low at investinglive.com.

US ISM services set to reflect a slowdown in activity towards the end of last year

January 7, 2026 18:45 Forexlive Latest News Market News

The estimate is for the headline PMI reading to drop to 52.3, down from 52.6 in November. That will point to a further moderation in business activity to round up the year, as reflected in the S&P Global PMI report yesterday here. If the ISM print matches the estimate, that will be the softest reading since September last year.

Now, overall activity is still expected to remain in expansion territory. So, the reading is not going to point to major trouble but just some moderation in the growth momentum.

Looking at yesterday’s report by S&P Global, there are a couple of key downside points to note. For one, new orders were especially weak as new business

placed at services providers showed the smallest rise in some

20 months. That points to some softening in demand conditions and one that could extend into the new year.

The other key point is that employment conditions stagnated on the month, failing to rise for the first time since February. S&P Global noted that the fall is negligible but it does put an end to a nine-month sequence of continuous growth. Of note, cost concerns, budget constraints and the

downturn in demand growth were cited as reasons for the lackluster

trend in employment.

So, those are some things to watch out for when we get to the ISM report later.

Besides that, one of the more focal points will be the prices paid component – which fell quite sharply in November. In fact, the drop from 70.0 in October to 65.4 in November represents the largest in 21 months. That saw the component drop to its lowest since April but is still sitting well above historical levels.

What about December then?

MNI notes that the signal is a little more mixed based on regional Fed surveys. They note that Dallas was the only one of five Fed surveys to report a dip in prices paid from November to December. Meanwhile, New York and Philly reported noticeable upticks in prices paid pressures. At the balance, it points to a slightly higher prices paid gauge this time around.

So, that is likely to help deflect the sharp drop in November as prices stabilise in December; that is if things play out expectedly.

This article was written by Justin Low at investinglive.com.

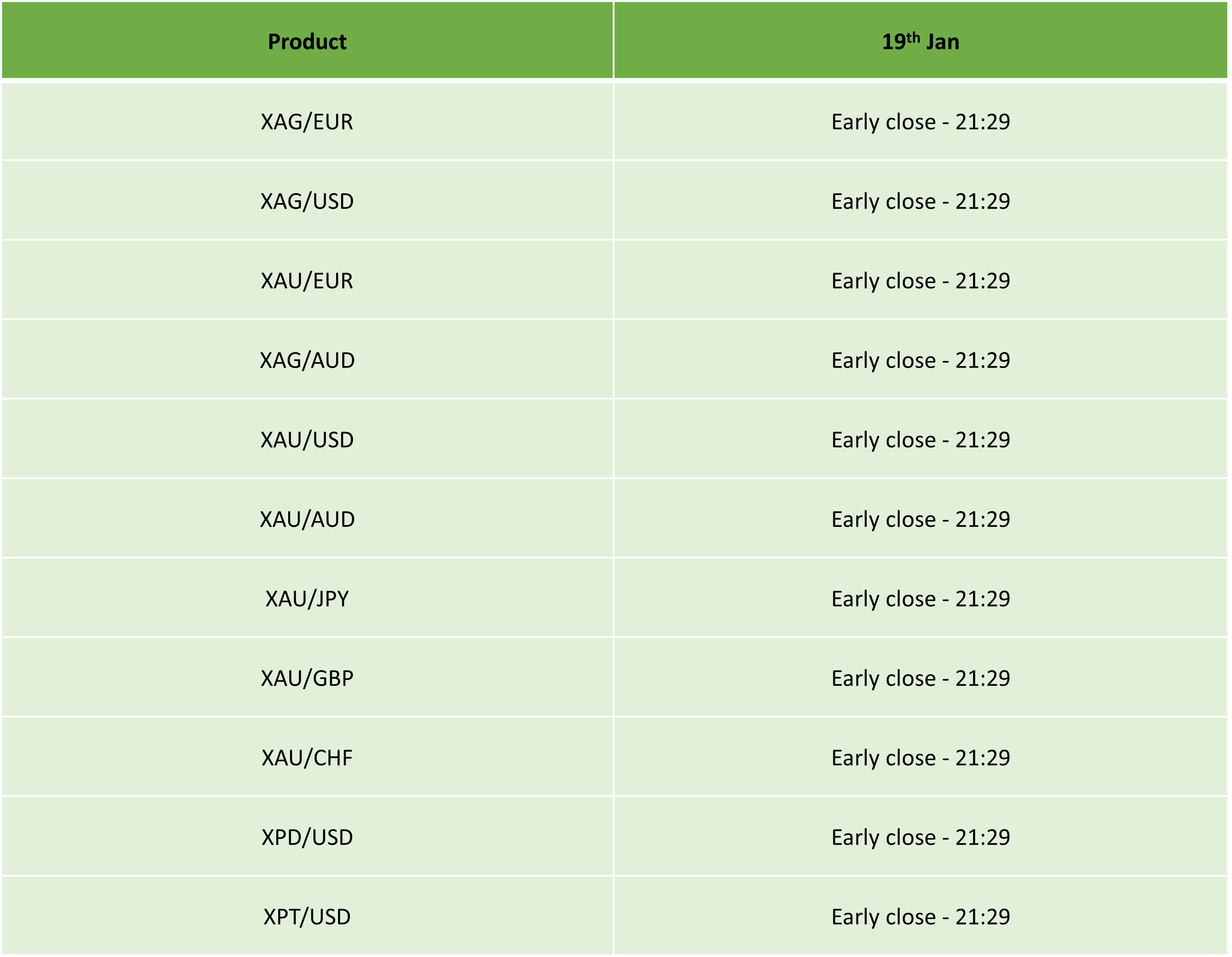

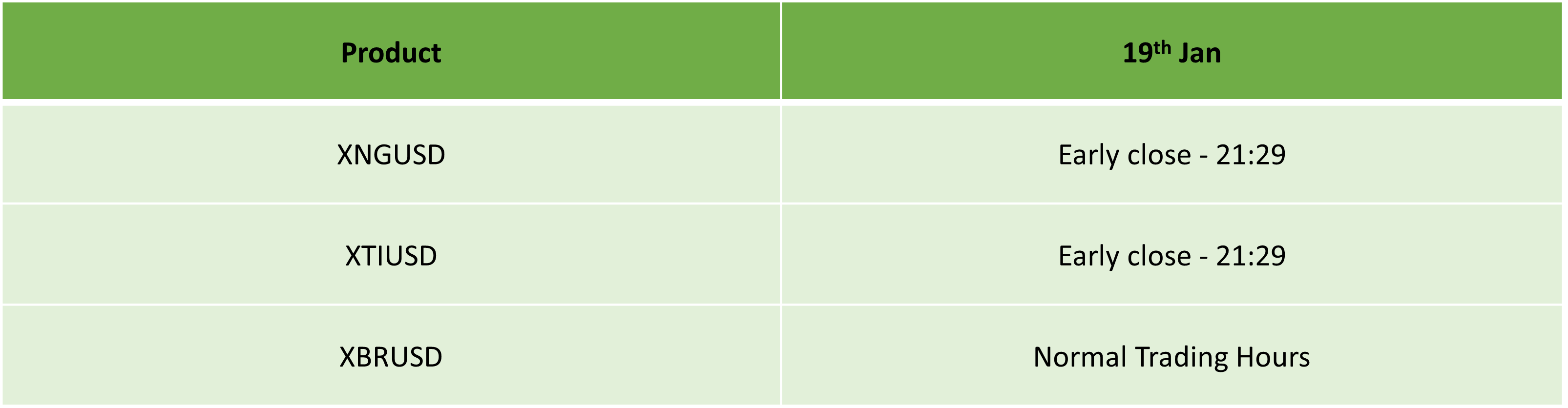

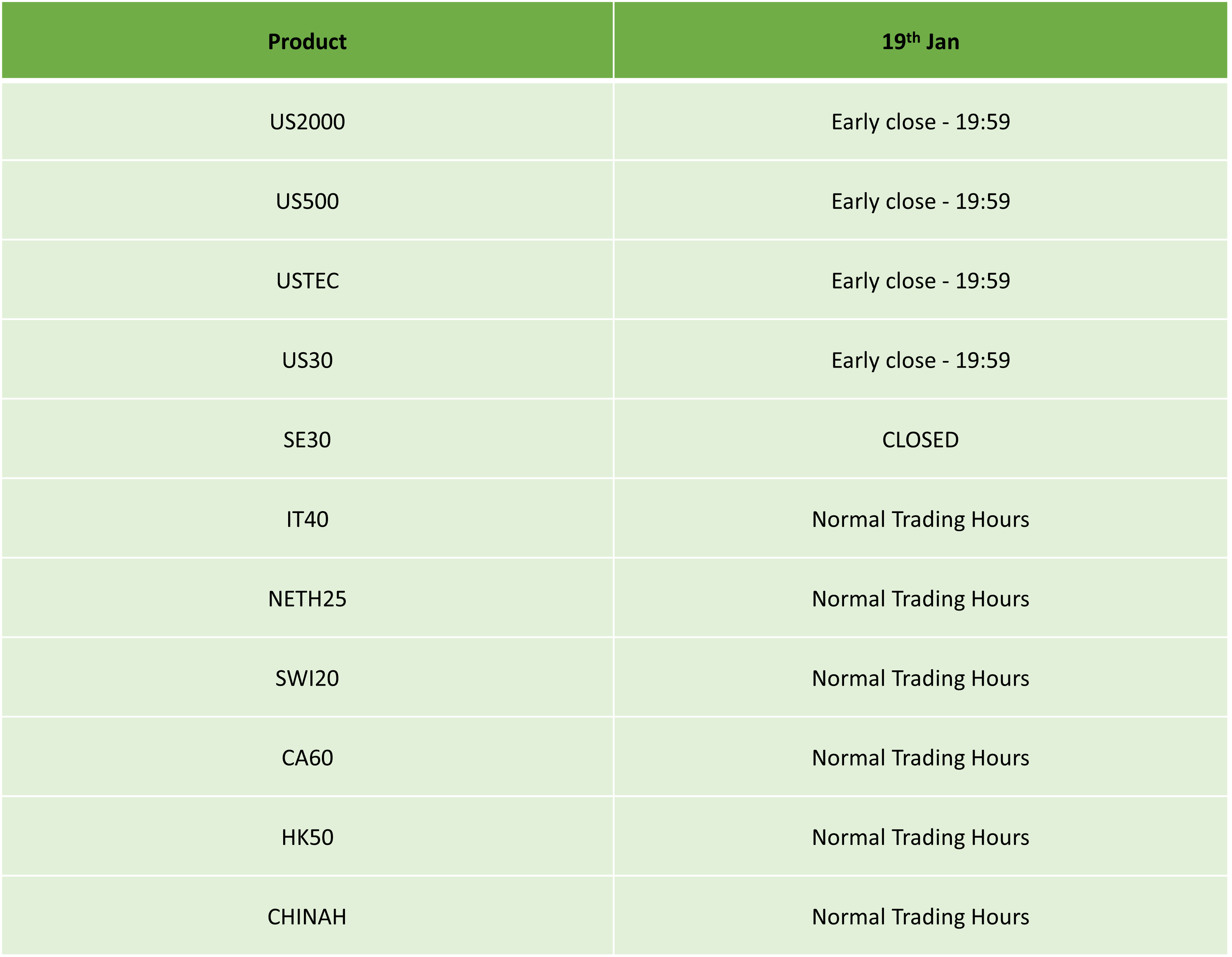

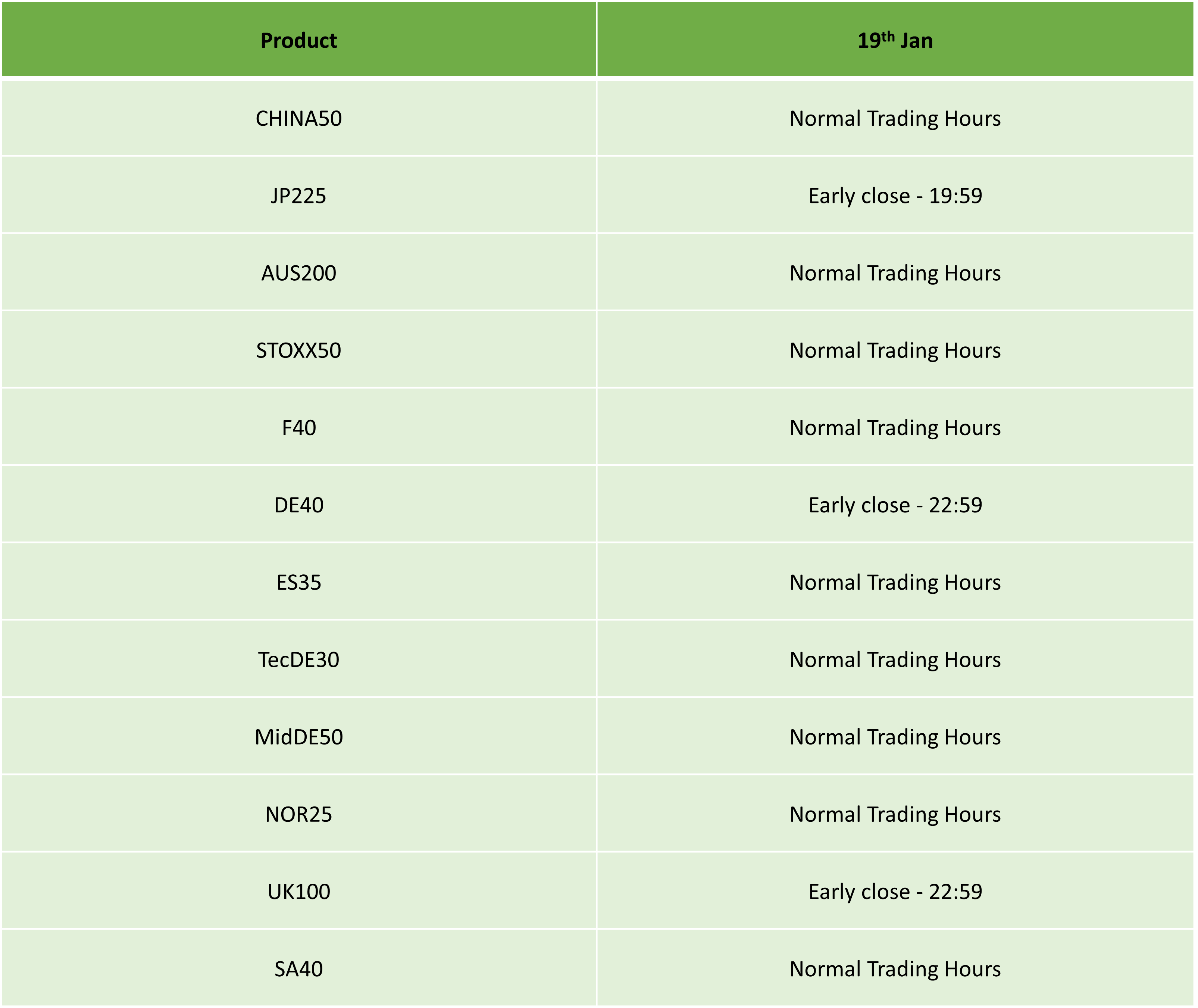

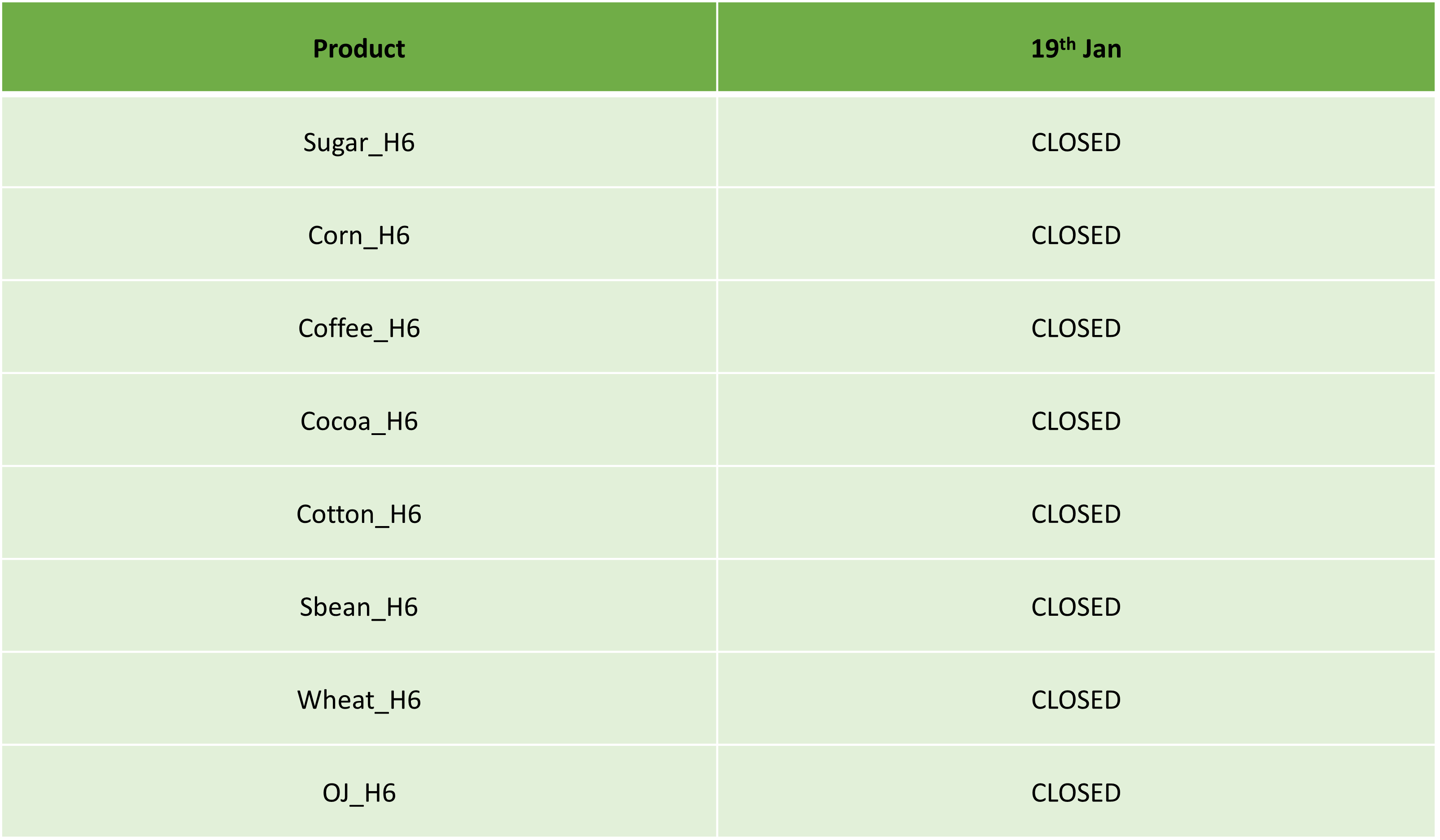

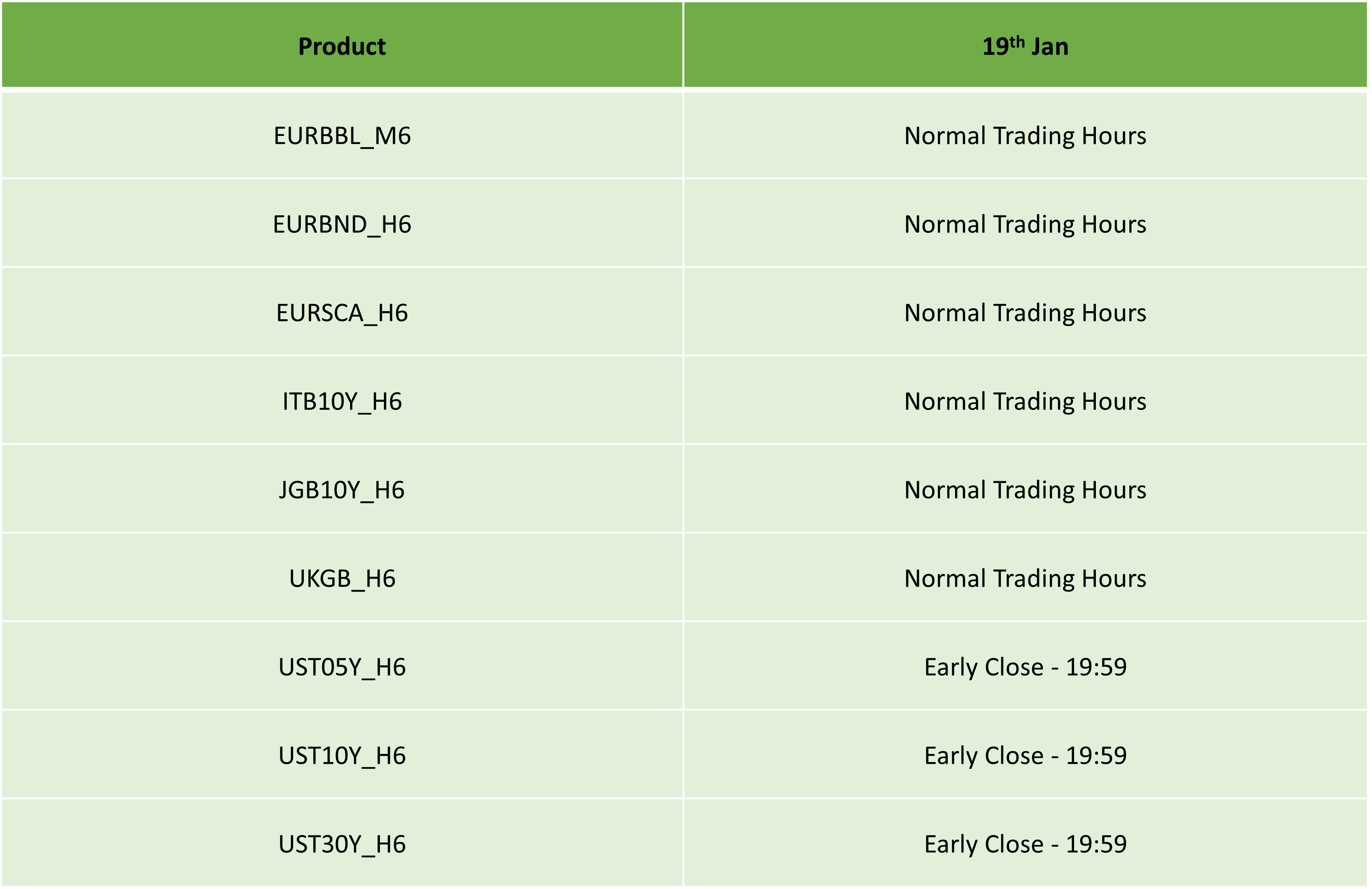

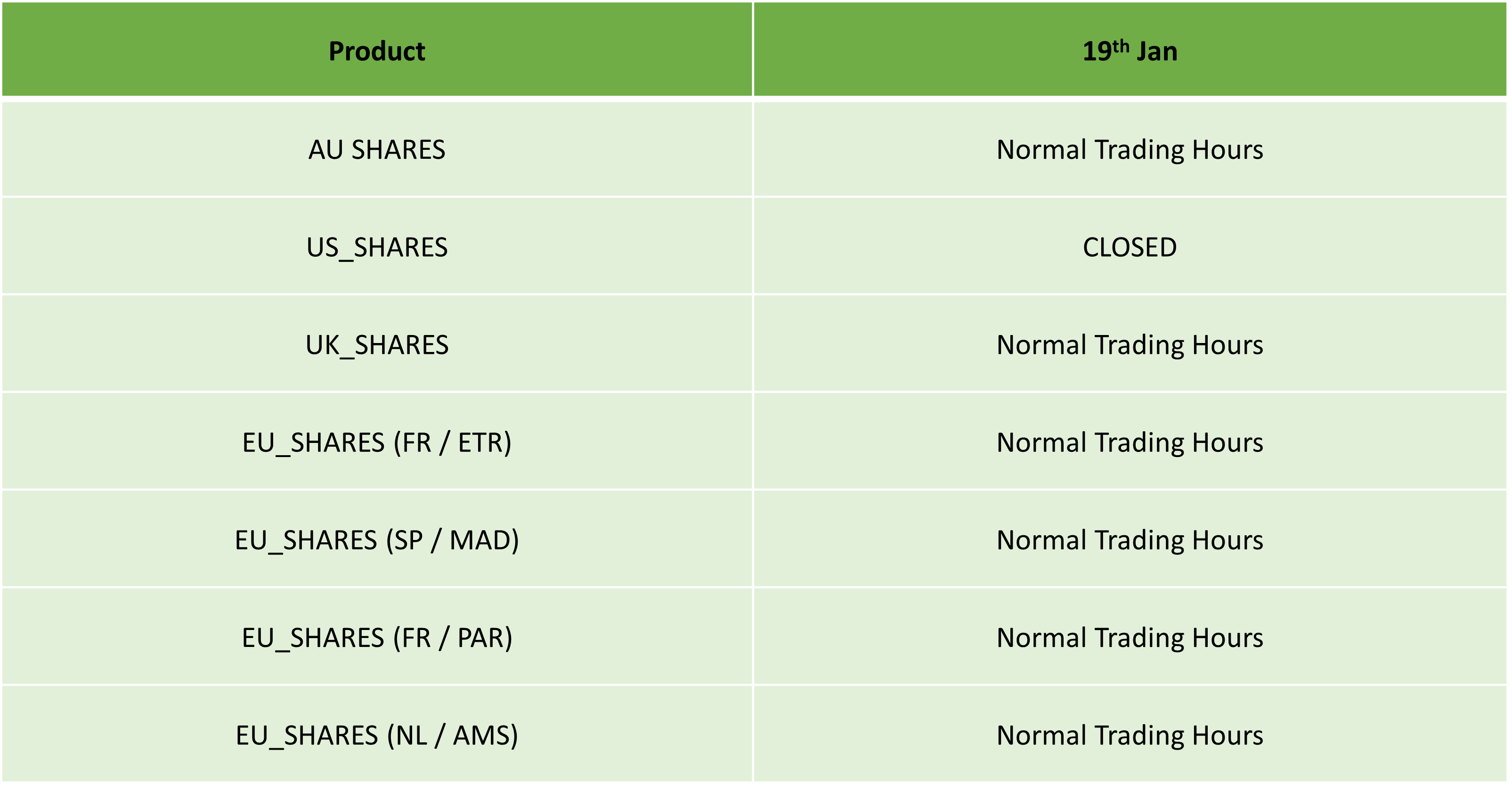

Martin Luther King Day Trading Schedule – 2026

January 7, 2026 18:39 ICMarkets Market News

Dear Client,

Please find our updated Trading schedule and general information related to the Martin Luther King Day on Monday, 19 January, 2026.

Liquidity over the holidays is expected to be particularly thin so please take the necessary precaution to ensure that you are not affected by increased volatility, spreads and intermittent pricing.

All times mentioned below are Platform time (GMT +2).

Forex & Crypto Pairs:

Precious Metals:

Spot Energies:

Indices:

Energy Futures:

Soft Commodities Futures:

Indices Futures:

Bonds Futures:

Equities:

Metal Futures:

Kind regards,

IC Markets Team.

The post Martin Luther King Day Trading Schedule – 2026 first appeared on IC Markets | Official Blog.

Eurozone December preliminary CPI +2.0% vs +2.0% y/y expected

January 7, 2026 17:14 Forexlive Latest News Market News

- Prior +2.1%

- Core CPI +2.3% vs +2.4% y/y expected

- Prior +2.4%

Headline annual inflation eased slightly to hit the 2% mark with core annual inflation also easing marginally. Still, it’s no time to celebrate just yet and the ECB knows that very well. Services inflation remains the key sticking point, coming in at 3.4% in December. That is slightly better than in November (3.5%) but remains well above what it was from the middle of last year (around 3.2%). On the month itself, services inflation moved up by 0.7%.

All of this continues to point towards the narrative that the ECB won’t feel the rush nor the pressure to act any time soon. That especially since the German economy is still flagging in the meantime while waiting for the fiscal kick with inflation pressures still largely persisting in the region’s largest economy.

So, carry on as you will as the ECB will be staying on the sidelines for the foreseeable future.

EUR/USD holds little changed on the day at 1.1686 with not much appetite among major currencies today. The dollar is pretty much trading flattish across the board as we await the US ADP employment change and ISM services PMI later in the day.

This article was written by Justin Low at investinglive.com.

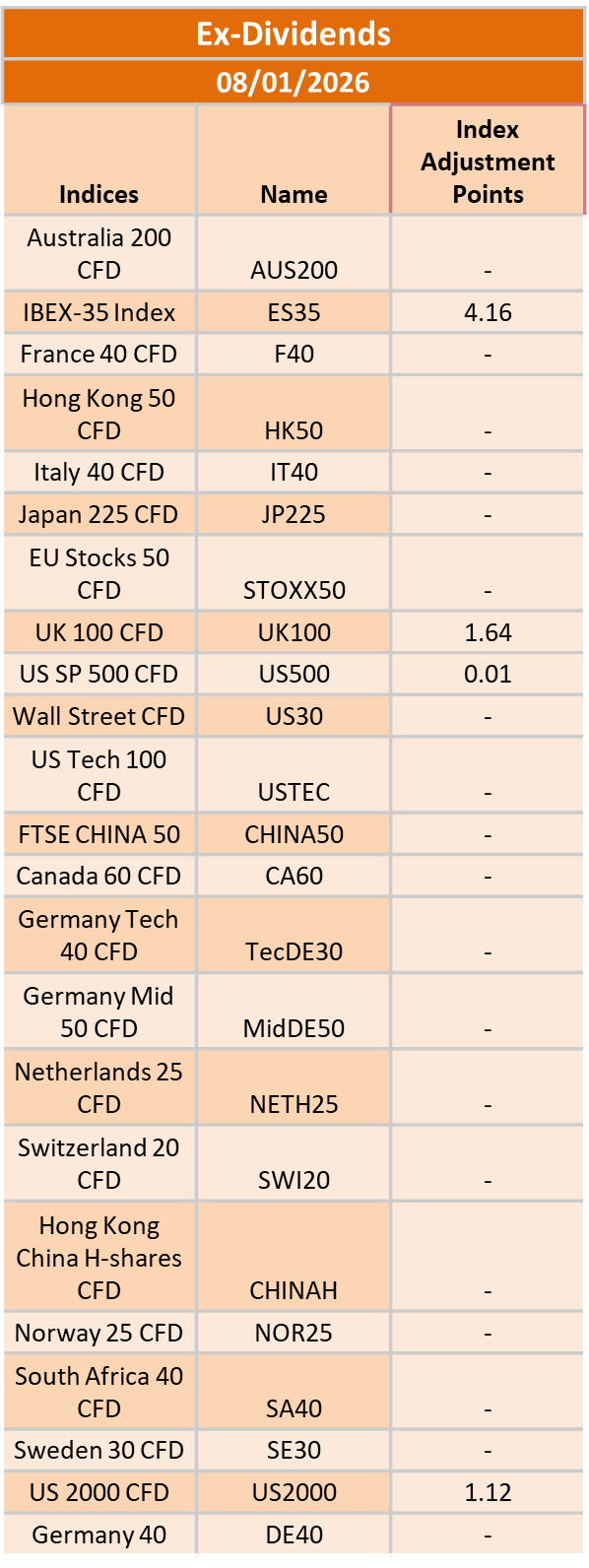

Ex-Dividend 08/01/2026

January 7, 2026 17:14 ICMarkets Market News

The post Ex-Dividend 08/01/2026 first appeared on IC Markets | Official Blog.

UK December construction PMI 40.1 vs 42.5 expected

January 7, 2026 16:39 Forexlive Latest News Market News

- Prior 39.4

The decline in UK construction activity was less pronounced in December but it’s still a terrible end to the year for the sector. There were sharp falls once again in housing, commercial and civil

engineering activity as incoming new work remains subdued. Civil engineering (32.9) was the weakest-performing category of

construction activity in December, and that is despite

recording a softer rate of contraction than in November. Meanwhile, both housing activity (33.5) and commercial

construction (42.0) decreased to the greatest extent since

May 2020. Ouch.

The only positive footnote is that business activity expectations rebounded to five-month high. But that’s about it.

S&P Global notes that:

“UK construction companies once again reported

challenging business conditions and falling workloads

in December, but the speed of the downturn moderated

from the five-and-a-half-year record seen in November.

Many firms cited subdued demand and fragile client

confidence. Despite a lifting of Budget-related

uncertainty, delayed spending decisions were still cited

as contributing to weak sales pipelines at the close of

the year.

“By sector, latest data indicated the fastest reductions

in housing and commercial construction since May 2020,

while civil engineering was the only segment to signal a

slower pace of decline than in the previous month.

“Total new orders nonetheless decreased to a much

lesser degree than in November, while business activity

expectations for the year ahead rebounded to a fivemonth high. Some survey respondents attributed greater

optimism to projections of rising infrastructure spending,

especially in the utilities sector. There were also hopes

that lower borrowing costs and easing inflationary

pressures could boost demand across the construction

sector.

“Supplier performance meanwhile improved for the

fifth month running, largely due to lower input buying.

This also contributed to a slowdown in purchasing price

inflation to its weakest since October 2024.”

This article was written by Justin Low at investinglive.com.

German construction activity returns to growth at end of 2025

January 7, 2026 15:45 Forexlive Latest News Market News

- Germany December construction PMI 50.3

- Prior 45.2

That’s some positive news at least for the German economy, with the jump higher here driven by a further increase in civil engineering activity. Of note, activity in this segment registered its strongest rate of expansion since March 2011. Besides that, the drag on total activity

from the housing sector eased considerably as work on residential projects fell at the slowest rate since March 2022. And adding to that, employment conditions also ticked up for a second month in a row.

All that being said, this is just one reading. Firms’ expectations towards activity in the year ahead remained subdued and that will keep any optimism towards the outlook more limited for now.

HCOB notes that:

“The construction sector experienced a surprisingly positive end to last year. For the first time since March 2022, the total

activity index has moved into expansion territory. This is partly thanks to a sharp boost in civil engineering. But it also seems

that sentiment in the previously battered residential construction sector is starting to turn. We may be seeing signs that the

housing sector is emerging from a deep recession, with activity now only edging down slightly. To keep things in

perspective, this is just one monthly figure, and the time series has shown big swings before. Still, the sharp rise in building

permits recently reported by the Federal Statistical Office gives hope that this isn’t just a one-off.

“The strong acceleration in civil engineering activity suggests that the infrastructure measures announced by the federal

government are finally moving into the implementation phase. This applies especially to transport infrastructure – roads,

bridges, and rail. Growth hiccups are still possible in civil engineering in 2026, but as the year progresses, the growth path

should stabilize as more projects get underway. This trend will likely mean that resources from less busy construction

segments will increasingly be deployed in civil engineering. Notably, employment in the construction sector has been rising

again for two months, after the last expansion nearly four years ago.

“Building continues to get more expensive. Construction costs rose a bit more sharply in December than in the previous

month. Combined with relatively high long-term interest rates, which is a key factor, especially for residential construction,

this acts as a dampener. And given the ECB’s communication, short-term rates aren’t expected to fall anytime soon, which

doesn’t help either.”

This article was written by Justin Low at investinglive.com.