Articles

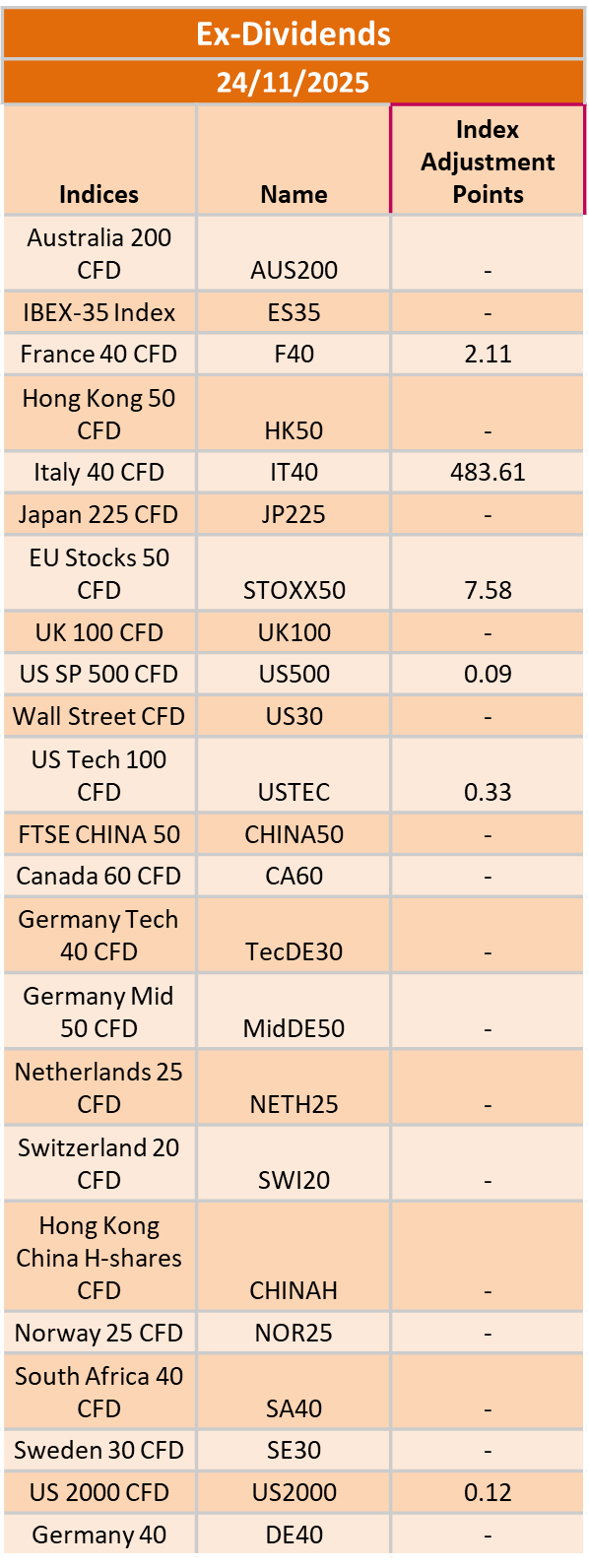

Ex-Dividend 24/11/2025

423767 November 21, 2025 17:14 ICMarkets Market News

The post Ex-Dividend 24/11/2025 first appeared on IC Markets | Official Blog.

Friday 21th November 2025: Asian Markets Tumble as Rate Cut Hopes Fade and Tech Sell-Off Deepens

423766 November 21, 2025 17:00 ICMarkets Market News

Global Markets:

- Asian Stock Markets : Nikkei down -2.17%, Shanghai Composite down -1.88%, Hang Seng down -2.16% ASX down -1.40%

- Commodities : Gold at $4,055.56 (-0.09%), Silver at $94.530 (-1.55%), Brent Oil at $62.58 (-1.26%), WTI Oil at $58.18 (-1.39%)

- Rates : US 10-year yield at 4.094, UK 10-year yield at 4.5890, Germany 10-year yield at 2.7194

News & Data:

- (USD) Non-Farm Employment Change 119K to 53K expected

- (USD) Unemployment Rate 4.4% to 4.3% expected

Markets Update:

Asian stock markets are sharply lower on Friday, tracking the negative cues from Wall Street as investors dial back expectations for a U.S. Fed rate cut in December. The long-delayed September jobs report showed higher unemployment alongside stronger-than-expected job growth, prompting fresh concerns about inflation and monetary policy. Fears of an AI-driven valuation bubble also continue to weigh on sentiment. This follows a mostly higher finish for Asian markets on Thursday.

In Australia, the S&P/ASX 200 has reversed the prior session’s gains and is trading well below 8,450, dragged down by broad weakness in mining, energy and technology stocks. Major miners such as BHP, Rio Tinto and Fortescue are all sharply lower, while tech names like Block and Zip are also under pressure. Banks and gold miners are seeing notable declines as well. Shares of Accent Group and Lovisa are tumbling after disappointing updates. Economic data was more upbeat, with Australia’s services and manufacturing PMIs improving in November.

Japan’s Nikkei 225 is also sharply lower, falling more than 2 percent as heavyweight tech stocks slump. SoftBank and Advantest are among the biggest laggards, while automakers Toyota and Honda are posting modest gains. Inflation data for October met expectations, while the country’s trade deficit narrowed slightly.

Elsewhere, markets in South Korea, Taiwan, China and Hong Kong are firmly lower, while Wall Street ended Thursday deep in the red as major U.S. indices reversed early gains and finished near session lows.

Upcoming Events:

- 02:45 PM GMT – USD Flash Manufacturing PMI

- 02:45 PM GMT – USD Flash Services PMI

The post Friday 21th November 2025: Asian Markets Tumble as Rate Cut Hopes Fade and Tech Sell-Off Deepens first appeared on IC Markets | Official Blog.

General Market Analysis – 21/11/25

423765 November 21, 2025 17:00 ICMarkets Market News

US Equities Drop Again After Employment Data – Nasdaq down 2.15%

US stocks slid again in yesterday’s session, with all three major indices finishing firmly in the red. The pullback came as the initial boost from Nvidia’s upbeat earnings faded and investors refocused on the mixed September jobs report, which showed stronger headline job creation but an unwelcome rise in the unemployment rate. The Dow Jones dropped 0.84% to close at 45,752, while the S&P 500 fell 1.56% to 6,538, and the Nasdaq led the declines with a 2.15% fall to 22,078. Treasury yields fell after the numbers, with the 2-year yield dropping 5.9 basis points to 3.533%, and the 10-year slipping 5.2 basis points to 4.084%. Despite lower yields, the US dollar remained firm, with the DXY edging up 0.05% to 100.23, keeping it near its strongest levels of the year. Commodities were weaker across the board. Brent fell 0.58% to US$63.13, while WTI crude declined 0.83% to US$58.76, as ongoing US diplomatic pressure for progress in the Russia–Ukraine conflict continued to weigh on sentiment. Gold had a rare quiet day, inching up just 0.02% to US$4,077.19 by the NY close, marking one of its most range-bound sessions in weeks.

Mixed Employment Data Locks in Live December Fed Meeting

The first US employment numbers for a couple of months came in mixed overnight, with the headline Non-Farms employment change printing at +119k, smashing expectations, which had been around the +60k mark. However, the Average Hourly Earnings number came in at 0.2% against an expected 0.3%, and the Unemployment Rate jumped to 4.4%. We had mixed reactions across financial markets, with Treasury yields pulling back after the data and stocks slumping, while the dollar held its ground against the majors to push toward annual highs. Fed rate-cut expectations had dipped to around 30% on the previous day, but they have blipped up to near 40%, which means that the Fed meeting in December at the moment falls very much in the “live” category. We will have more data following in the coming weeks, but if we see more mixed messages from the figures, then expect a very turbulent market day on December 10th.

Busy Day to End the Trading Week

It shapes up as a busy end to the trading week, with a heavy run of data scheduled across the European and US sessions and several central bank speakers expected to provide further clues on policy direction. The Asian session is relatively quiet, but the data starts to come thick and fast as soon as London comes in. There are a raft of Flash Services and Manufacturing PMI numbers due out today, with data from France, Germany, the EU, the UK, and the US all likely to move markets. The London session also sees the release of the latest UK Retail Sales data (exp. -0.1% m/m). The New York session also sees Retail Sales numbers out of Canada, with the market expecting the headline to show a 0.7% month-on-month decline and the Core data a 0.5% pullback. We also hear from several central bankers during the course of the latter two sessions, with the SNB’s Martin Schlegel and the ECB’s Christine Lagarde featuring earlier in the day, and Fed members Barr, Miran, Jefferson, and Logan all speaking later on.

The post General Market Analysis – 21/11/25 first appeared on IC Markets | Official Blog.

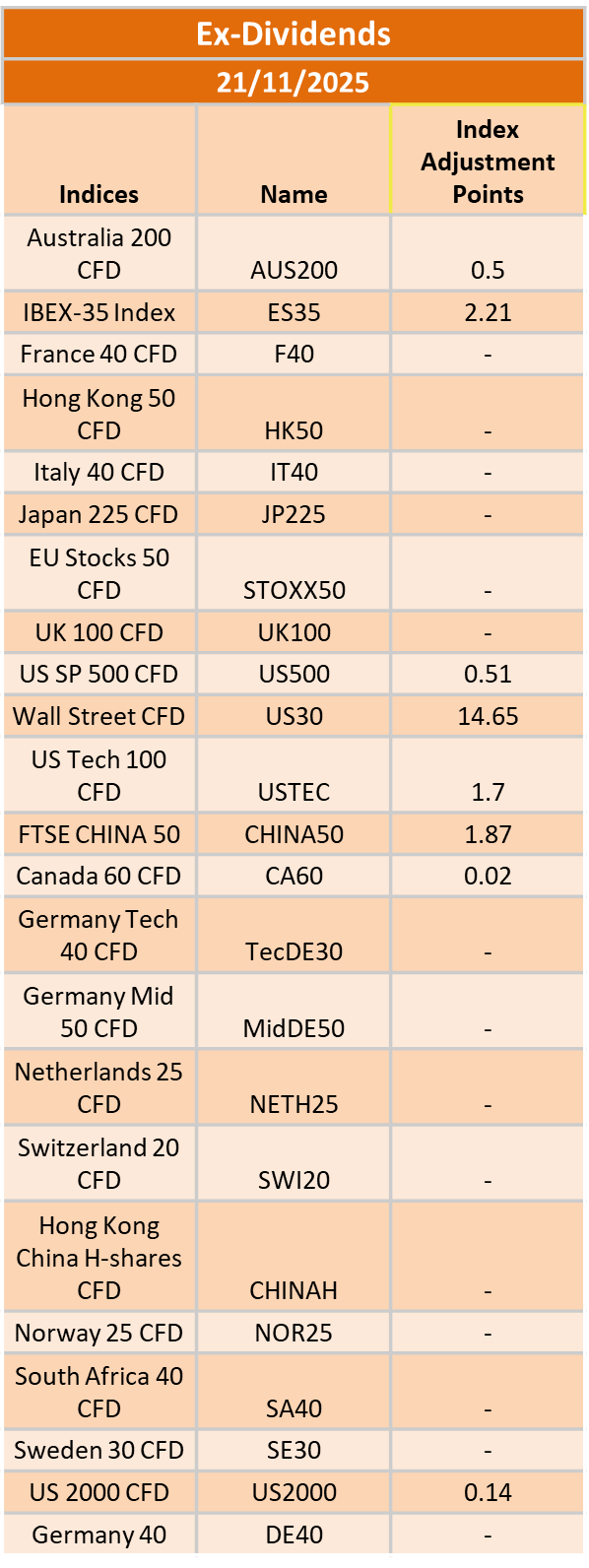

Ex-Dividend 21/11/2025

423722 November 20, 2025 17:00 ICMarkets Market News

The post Ex-Dividend 21/11/2025 first appeared on IC Markets | Official Blog.

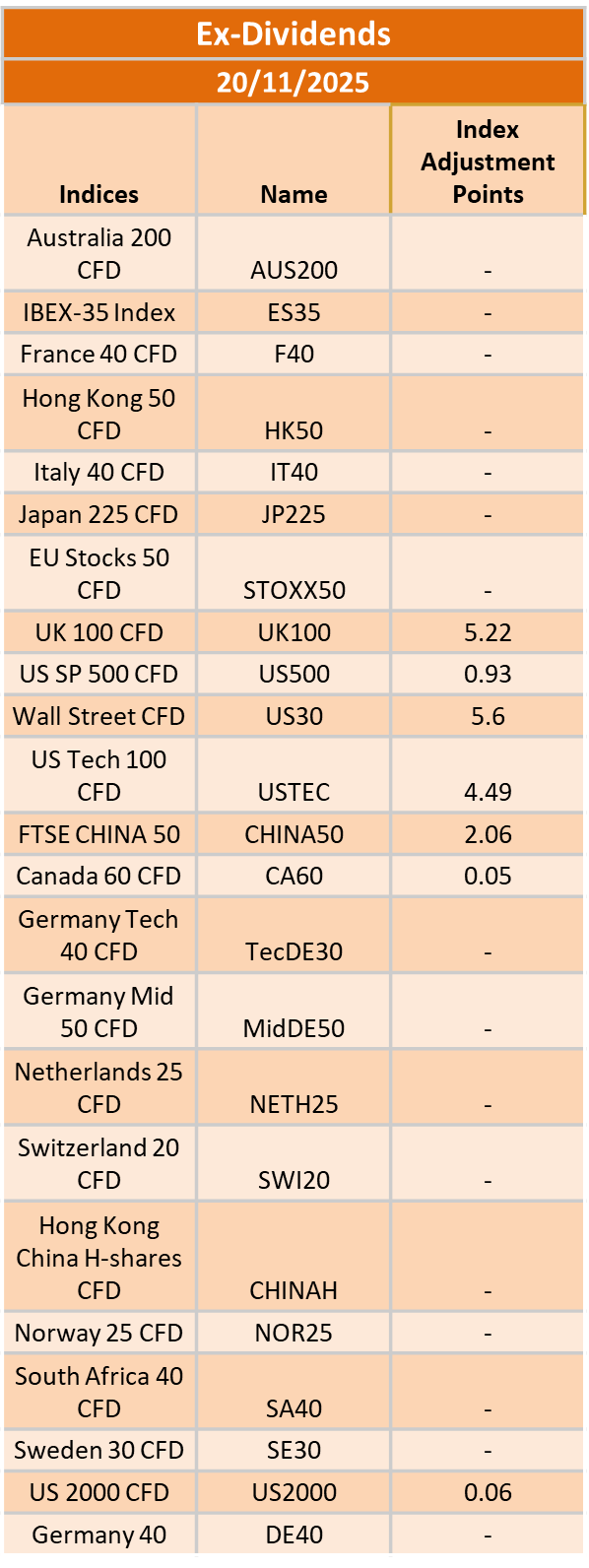

General Market Analysis – 20/11/25

423721 November 20, 2025 16:00 ICMarkets Market News

US Stocks Push Higher Ahead of Nvidia and Jobs Data – Nasdaq up 0.6%

US stocks pulled back some of their recent losses in choppy trading yesterday, with the Dow finishing up 0.10% at 46,138, the S&P 500 rising 0.38% to 6,642, and the Nasdaq gaining 0.59% to 22,564. Investors are likely to find further support today following a strong post-close earnings update from Nvidia, which helped sentiment in tech-heavy sectors. The US dollar surged 0.58% to 100.13 after more hawkish FOMC meeting minutes, while Treasury yields also climbed, the 2-year up 1.9 basis points to 3.592% and the 10-year rising 2.3 basis points to 4.137%. In commodities, oil prices retreated on news of a renewed US push to negotiate an end to the Russia–Ukraine conflict; Brent closed down 1.85% at $63.66 and WTI fell 2.14% to $59.58. Gold, meanwhile, edged 0.26% higher to $4,077.98 as investors awaited fresh US labour market data.

US Jobs Numbers to Dominate Markets

The long-delayed US employment figures for September are at last due to be released later today, and traders are expecting to see plenty of moves in the market around the event. Jobs numbers over the US summer had deteriorated significantly, which had led to a much more dovish Fed and had elevated investor hopes for further rate cuts to stimulate the economy. However, the US government shutdown, which commenced on October 1, delayed the release of the tier 1 data until today, and although we have seen a 25-basis point cut in the interim period, market pricing and last night’s Fed meeting minutes have now reduced the likelihood of a further cut in December to 32%—having stood at 95% a month ago. A much weaker-than-expected print compared with the anticipated 60k increase could really put the cat amongst the pigeons and see further sharp corrections in the market. Whatever the result, most traders are expecting plenty of volatility around the release.

Non-Farms Day – At Last!

Today brings the long-awaited Non-Farm Payrolls report, with September data arriving 48 days late. There is little on the event calendar in the first couple of sessions of the day, although Chinese Loan Prime Rate updates could move markets in the unlikely event that there is a surprise. However, it is a different story once New York opens. Traders are bracing for heightened volatility as we get our first tier-one look at US employment data in weeks; the headline Non-Farms Employment Change is expected to come in around the +60k mark, with the Unemployment Rate remaining steady at 4.3% and the Average Hourly Earnings printing at +0.3% again. Existing home sales data (exp. 4.08mio) will also be released later in the session, but expect the jobs numbers to dominate sentiment into the close.

The post General Market Analysis – 20/11/25 first appeared on IC Markets | Official Blog.

Thursday 20th November 2025: Technical Outlook and Review

423706 November 20, 2025 15:39 ICMarkets Market News

DXY (U.S. Dollar Index):

Potential Direction: Bullish

Overall momentum of the chart: Bearish

The price could see a short-term pullback toward the pivot before rising again toward the 1st resistance.

Pivot: 99.80

Supporting reasons: Identified as a pullback support, where renewed buying pressure could emerge to push the price higher.

1st support: 99.35

Supporting reasons: Identified as an overlap support, indicating a potential area where the price could again stabilize.

1st resistance: 100.35

Supporting reasons: Identified as a swing high resistance, indicating a potential area that could halt any further upward movement

EUR/USD:

Potential Direction: Bearish

Overall momentum of the chart: Bearish

The price could see a short-term pullback toward the pivot before continuing its bearish move down toward the 1st support.

Pivot: 1.1569

Supporting reasons: Identified as a pullback resistance, where selling pressures could intensify and potentially cap any upward retracement.

1st support: 1.1527

Supporting reasons: Identified as an overlap support that aligns with the 61.8% Fibonacci retracement, indicating a potential level where the price could stabilize once again.

1st resistance: 1.1623

Supporting reasons: Identified as a pullback resistance, indicating a potential level that could cap further upward movement.

EUR/JPY:

Potential Direction: Bullish

Overall momentum of the chart: Bullish

The price could see a short-term pullback toward the pivot before rising again toward the 1st resistance.

Pivot: 179.93

Supporting reasons: Identified as a pullback support, where renewed buying pressure could emerge to push the price higher.

1st support: 178.67

Supporting reasons: Identified as a pullback support, indicating a potential area where the price could again stabilize.

1st resistance: 181.87

Supporting reasons: Identified as a resistance that is supported by the 200% Fibonacci extension, indicating a potential level that could cap further upward movement.

EUR/GBP:

Potential Direction: Bullish

Overall momentum of the chart: Bullish

The price could see a short-term pullback toward the pivot before rising again toward the 1st resistance.

Pivot: 0.8817

Supporting reasons: Identified as a pullback support, where renewed buying pressure could emerge to push the price higher.

1st support: 0.8751

Supporting reasons: Identified as an overlap support, indicating a potential area where the price could stabilize once more.

1st resistance: 0.8865

Supporting reasons: Identified as a swing high resistance, indicating a potential level that could cap further upward movement.

GBP/USD:

Potential Direction: Bearish

Overall momentum of the chart: Bullish

The price could see a short-term pullback toward the pivot before continuing its bearish move down toward the 1st support.

Pivot: 1.3096

Supporting reasons: Identified as a pullback resistance, where selling pressures could intensify and potentially cap any upward retracement.

1st support: 1.3012

Supporting reasons: Identified as a swing low support, indicating a potential area where the price could stabilize once more.

1st resistance: 1.3212

Supporting reasons: Identified as a swing high resistance, indicating a potential level that could halt further upward movement.

GBP/JPY:

Potential Direction: Bullish

Overall momentum of the chart: Bullish

The price could see a short-term pullback toward the pivot before rising again toward the 1st resistance.

Pivot: 204.01

Supporting reasons: Identified as an overlap support, where renewed buying pressure could emerge to push the price higher.

1st support: 203.20

Supporting reasons: Identified as a pullback support, indicating a potential level where the price could stabilize once more.

1st resistance: 205.28

Supporting reasons: Identified as a resistance that is supported by the 161.8% Fibonacci extension, indicating a potential level that could halt further upward movement.

USD/CHF:

Potential Direction: Bullish

Overall momentum of the chart: Bearish

The price could see a short-term pullback toward the pivot before rising again toward the 1st resistance.

Pivot: 0.7994

Supporting reasons: Identified as a pullback support, where renewed buying pressure could emerge to push the price higher.

1st support: 0.7892

Supporting reasons: Identified as a swing low support, indicating a potential level where the price could stabilize once again.

1st resistance: 0.8067

Supporting reasons: Identified as an overlap resistance, indicating a potential level that could cap further upward movement.

USD/JPY:

Potential Direction: Bullish

Overall momentum of the chart: Bullish

The price could see a short-term pullback toward the pivot before rising again toward the 1st resistance.

Pivot: 155.02

Supporting reasons: Identified as an overlap support, where renewed buying pressure could emerge to push the price higher.

1st support: 154.08

Supporting reasons: Identified as an overlap support, indicating a strong area where buyers might return, and the price could stabilize once again.

1st resistance: 157.34

Supporting reasons: Identified as a resistance that is supported by the 161.8% Fibonacci extension. This level represents the next key area where upward movement could be capped amid increased selling pressure

USD/CAD:

Potential Direction: Bullish

Overall momentum of the chart: Bearish

The price has already bounced off the pivot and may continue its bullish move toward the 1st resistance

Pivot: 1.3986

Supporting reasons: Identified as an overlap support, where renewed buying pressure could emerge to push the price higher.

1st support: 1.3907

Supporting reasons: Identified as an overlap support, indicating a key level where the price could stabilize once more.

1st resistance: 1.4073

Supporting reasons: Identified as a pullback resistance, making it a possible target for bullish advances and a level where some sellers could return to cap gains

AUD/USD:

Potential Direction: Bearish

Overall momentum of the chart: Bullish

The price has already reacted off the pivot and may continue its bearish move toward the 1st support

Pivot: 0.6513

Supporting reasons: Identified as an overlap resistance that aligns with the 50% Fibonacci retracement, where selling pressures could intensify and potentially cap any upward retracement

1st support: 0.6447

Supporting reasons: Identified as a swing low support, this area has provided strong support historically and may attract buying interest for a potential short-term bounce

1st resistance: 0.6575

Supporting reasons: Identified as an overlap resistance, indicating a potential area that could halt any further upward movement.

NZD/USD

Potential Direction: Bearish

Overall momentum of the chart: Bullish

The price has already reacted off the pivot and may continue its bearish move toward the 1st support

Pivot: 0.5636

Supporting reasons: Identified as a pullback resistance, where selling pressures could intensify and potentially cap any upward retracement

1st support: 0.5585

Supporting reasons: Identified as a support that is supported by the 127.2% Fibonacci extension, this area has provided strong support historically and may attract buying interest for a potential short-term bounce

1st resistance: 0.5687

Supporting reasons: Identified as an overlap resistance, indicating a potential area that could halt any further upward movement.

US30 (DJIA):

Potential Direction: Bearish

Overall momentum of the chart: Bullish

The price could see a short-term pullback toward the pivot before continuing its bearish move down toward the 1st support.

Pivot: 46,458.40

Supporting reasons: Identified as a pullback resistance, where selling pressures could intensify and potentially cap any upward retracement.

1st support: 45,767.10

Supporting reasons: Identified as an overlap support that aligns with the 100% Fibonacci projection, suggesting a potential area where the price could stabilize once again.

1st resistance: 47,020.30

Supporting reasons: Identified as a pullback resistance, indicating a potential area that could halt any further upward movement.

DE40 (DAX):

Potential Direction: Bearish

Overall momentum of the chart: Bullish

The price could see a short-term pullback toward the pivot before continuing its bearish move down toward the 1st support.

Pivot: 23,429.48

Supporting reasons: Identified as a pullback resistance, where selling pressures could intensify and potentially cap any upward retracement.

1st support: 22,803.77

Supporting reasons: Identified as a support that is supported by the 161.8% Fibonacci extension, indicating a key level where the price could stabilize once more.

1st resistance: 23,940.12

Supporting reasons: Identified as an overlap resistance, indicating a potential area that could halt any further upward movement.

US500 (S&P 500):

Potential Direction: Bullish

Overall momentum of the chart: Bullish

The price could fall toward the pivot and could make a short-term pullback toward this level before rising again toward the 1st resistance.

Pivot: 6,675.17

Supporting reasons: Identified as a pullback support, where renewed buying pressure could emerge to push the price higher.

1st support: 6,588.42

Supporting reasons: Identified as a swing low support, indicating a potential level where the price could stabilize once again.

1st resistance: 6,744.27

Supporting reasons: Identified as a pullback resistance, indicating a potential area that could halt any further upward movement.

BTC/USD (Bitcoin):

Potential Direction: Bearish

Overall momentum of the chart: Bullish

The price could see a short-term pullback toward the pivot before continuing its bearish move down toward the 1st support.

Pivot: 98,751.49

Supporting reasons: Identified as a pullback resistance, where selling pressures could intensify and potentially cap any upward retracement.

1st support: 88,804.26

Supporting reasons: Identified as an overlap support, indicating a potential level where the price could stabilize once more.

1st resistance: 105,022.58

Supporting reasons: Identified as an overlap resistance, indicating a potential area that could halt any further upward movement.

ETH/USD (Ethereum):

Potential Direction: Bearish

Overall momentum of the chart: Bullish

The price could see a short-term pullback toward the pivot before continuing its bearish move down toward the 1st support.

Pivot: 3,200.23

Supporting reasons: Identified as an overlap resistance, where selling pressures could intensify and potentially cap any upward retracement.

1st support: 2,667.60

Supporting reasons: Identified as a support that is supported by the 161.8% Fibonacci extension, indicating a potential level where the price could stabilize once more.

1st resistance: 3,666.28

Supporting reasons: Identified as an overlap resistance, indicating a potential area that could halt any further upward movement.

WTI/USD (Oil):

Potential Direction: Bullish

Overall momentum of the chart: Bullish

The price has already bounced off the pivot and may continue its bullish move toward the 1st resistance

Pivot: 59.08

Supporting reasons: Identified as an overlap support, where renewed buying pressure could emerge to push the price higher.

1st support: 57.72

Supporting reasons: Identified as a pullback support, indicating a key level where the price could stabilize once more.

1st resistance: 61.12

Supporting reasons: Identified as an overlap resistance, indicating a potential area that could halt any further upward movement.

XAU/USD (GOLD):

Potential Direction: Bearish

Overall momentum of the chart: Bullish

The price could see a short-term pullback toward the pivot before continuing its bearish move down toward the 1st support.

Pivot: 4,111.13

Supporting reasons: Identified as a pullback resistance that aligns closely with the 50% Fibonacci retracement, where selling pressures could intensify and potentially cap any upward retracement.

1st support: 4,010.48

Supporting reasons: Identified as an overlap support, indicating a key level where the price could stabilize once more.

1st resistance: 4,217.81

Supporting reasons: Identified as an overlap resistance, indicating a potential area that could halt any further upward movement.

The accuracy, completeness and timeliness of the information contained on this site cannot be guaranteed. IC Markets Global does not warranty, guarantee or make any representations, or assume any liability regarding financial results based on the use of the information in the site.

News, views, opinions, recommendations and other information obtained from sources outside of www.icmarkets.com, used in this site are believed to be reliable, but we cannot guarantee their accuracy or completeness. All such information is subject to change at any time without notice. IC Markets Global assumes no responsibility for the content of any linked site.

The fact that such links may exist does not indicate approval or endorsement of any material contained on any linked site. IC Markets Global is not liable for any harm caused by the transmission, through accessing the services or information on this site, of a computer virus, or other computer code or programming device that might be used to access, delete, damage, disable, disrupt or otherwise impede in any manner, the operation of the site or of any user’s software, hardware, data or property.

The post Thursday 20th November 2025: Technical Outlook and Review first appeared on IC Markets | Official Blog.

IC Markets – Asia Fundamental Forecast | 20 November 2025

423705 November 20, 2025 15:39 ICMarkets Market News

IC Markets – Asia Fundamental Forecast | 20 November 2025

What happened in the U.S. session?

Overnight U.S. session developments were driven by earnings anticipation, shifting Fed rate cut probabilities, and steady macroeconomic releases, with major indexes, tech stocks, and the U.S. dollar most impacted. Defensive market tone persists as investors rotate away from technology and high-valuation sectors toward safer assets.The U.S. dollar is supported, gold sees modest safe-haven demand, and equities recover slightly but remain vulnerable to data and earnings surprises.

What does it mean for the Asia Session?

Traders should be prepared for elevated volatility, pay close attention to the aftermath of US macro data, and assess local economic signals for sector and regional plays. Thursday’s moves could lay the groundwork for broader trends heading into late November. The US dollar is holding up, especially against the Japanese yen and commodity currencies, while Asian indices are vulnerable to risk-off flows. Safe-haven demand is evident, with increased flows into gold and the yen as traders digest US policy uncertainty and shifting global growth forecasts.

The Dollar Index (DXY)

Key news events today

Average Hourly Earnings m/m (1:30 pm GMT)

Non-Farm Employment Change (1:30 pm GMT)

Unemployment Rate (1:30 pm GMT)

Philly Fed Manufacturing Index (1:30 pm GMT)

Unemployment Claims (Tentative)

Existing Home Sales (3:00 pm GMT)

What can we expect from DXY today?

The US dollar’s outlook remains mixed, with recent economic releases signaling stabilization. At the same time, ongoing government data recovery and cautious Federal Reserve policy keep traders on alert for volatility and shifting trends in forex and broader markets. In the forex markets, the dollar reached new highs against the yen earlier this week but then steadied as traders awaited the release of US jobs data. Against the euro, the dollar is consolidating after recent gains as the EUR/USD moves within a developing correction, with technical bias for a short-term bearish move, followed by a rebound.

Central Bank Notes:

- The Federal Open Market Committee (FOMC) voted, by majority, to lower the federal funds rate target range by 25 basis points to 3.75% — 4.00% at its October 28–29, 2025, meeting, marking the second consecutive cut following the 25 basis points reduction in September.

- The Committee maintained its long-term objectives of maximum employment and 2% inflation, noting that the labor market continues to soften, with modest job creation and an unemployment rate edging higher. In comparison, inflation remains above target at around 3.0%.

- Policymakers highlighted ongoing downside risks to economic growth, tempered by signs of resilient economic activity. September’s consumer price index (CPI) came in slightly below expectations at 3.0% year-over-year, easing inflationary pressure but still warranting vigilance amid tariff-driven price effects.

- Economic activity expanded modestly in the third quarter, with GDP growth estimates around 1.0% annualized; however, uncertainty remains elevated amid persistent global trade tensions and the U.S. government shutdown, which is impacting data availability.

- The updated Summary of Economic Projections anticipates an unemployment rate averaging approximately 4.5% for 2025, with headline and core personal consumption expenditures (PCE) inflation projections remaining near 3.0%, indicating a slow easing path ahead.

- The Committee emphasized its flexible, data-dependent approach and underscored that future policy adjustments will be guided by incoming labor market and inflation data. As in prior meetings, there was dissent, including one member advocating a more aggressive 50-basis-point cut.

- The FOMC announced the planned conclusion of its balance sheet reduction (quantitative tightening) program, intending to cease runoff in the near term to maintain market stability. Treasury redemption caps will remain steady at $5 billion per month, and agency mortgage-backed securities caps will remain at $35 billion.

- The next meeting is scheduled for 9 to 10 December 2025.

Next 24 Hours Bias

Weak Bullish

Gold (XAU)

Key news events today

Average Hourly Earnings m/m (1:30 pm GMT)

Non-Farm Employment Change (1:30 pm GMT)

Unemployment Rate (1:30 pm GMT)

Philly Fed Manufacturing Index (1:30 pm GMT)

Unemployment Claims (Tentative)

Existing Home Sales (3:00 pm GMT)

What can we expect from Gold today?

Gold remains strong near its recent highs, with the potential for further moderate gains into the end of November. If US macroeconomic data remains mixed and inflationary/geopolitical concerns persist. A strong US dollar or hawkish Federal Reserve message could trigger short-term corrections, but the prevailing trend continues to favor buying on dips unless major support levels are breached.

Next 24 Hours Bias

Weak Bullish

The Australian Dollar (AUD)

Key news events today

No major news event

What can we expect from AUD today?

The Australian Dollar is trading cautiously near recent lows, with the RBA holding rates steady and signaling no urgent policy moves. Market focus remains on technical barriers and future macro data, with expectations skewed toward continued range trading unless significant external shocks or surprises in Australian figures occur.

Central Bank Notes:

- The Reserve Bank of Australia held its cash rate steady at 3.60% at the November policy meeting, citing persistent inflationary pressures and lingering uncertainties in both domestic and global outlooks. This is the third consecutive pause following the cut in August.

- Policymakers remain alert to renewed inflation momentum. After a temporary uptick in September’s CPI, trimmed mean inflation for Q3 stands at 3.0%, above the intended 2–3% band. The RBA now anticipates that core inflation will stay above target until at least mid-2026, delaying any hopes of further easing.

- Headline CPI climbed by 3.2% in the year to September 2025, driven by resilient housing (+2.5%) and insurance costs, while discretionary goods inflation is subdued. The transition to monthly CPI reporting from November will improve the accuracy of inflation tracking.

- Domestic demand remains firm, particularly in services and housing, while manufacturing and discretionary retail continue to lag. Household incomes have stabilized, but high borrowing costs and elevated rents are constraining consumption and risking a slowdown in Q1 2026.

- Labor market tightness persists, though job growth has moderated. Underutilization edged higher. Wage growth is plateauing, but weak productivity is keeping unit labor costs elevated—a medium-term risk that remains central to the Board’s narrative.

- The RBA highlights geopolitical tensions and volatile commodity markets as primary global risks, against a backdrop of modest upward revisions to world growth forecasts. The Board stresses that its stance remains “cautious and data-dependent,” with ongoing vigilance on inflation, labor, and spending trends.

- Monetary policy remains mildly restrictive, balancing progress on price stability against vulnerabilities in household demand and global outlook. Board communications reaffirm a dual mandate: price stability and full employment, while underscoring readiness to respond should risks materialize sharply.

- Analysts generally expect the cash rate to remain at current levels through early 2026, with only modest cuts possible later in the year if inflation moderates. The new monthly CPI release (first full edition Nov 2025) will be watched closely for timely signals on price trends.

- The next meeting is on 9 December 2025.

Next 24 Hours Bias

Medium Bearish

The Kiwi Dollar (NZD)

Key news events today

No major news event

What can we expect from NZD today?

The New Zealand Dollar (NZD) weakened further, reaching multi-month lows against the US Dollar (USD), as traders priced in expectations for an imminent interest rate cut from the Reserve Bank of New Zealand (RBNZ) and responded to ongoing declines in key export commodity prices. The NZD/USD pair traded near 0.5666, attempting a minor bullish correction but remaining in a short-term bearish trend. All gains made earlier in 2025 have now been erased, and analysts expect continued pressure unless there is a strong reversal in market sentiment or economic data surprises.

Central Bank Notes:

- The Monetary Policy Committee (MPC) agreed to cut the Official Cash Rate (OCR) by 50 basis points to 2.50% on 8 October 2025, exceeding market expectations for a smaller 25-basis-point reduction and signaling a stronger commitment to reviving growth.

- The decision was reached by consensus, marking a shift from previous split votes, and reflected policymakers’ shared view that sustained economic weakness and persistent disinflationary pressures required a more front-loaded policy response.

- Annual consumer price inflation stood at 2.7% in the June quarter and is seen nearing 3% for the September quarter—above the 2% midpoint but within the 1–3% target range. Despite high near-term readings, the MPC projects inflation will return toward 2% by the first half of 2026 as spare capacity and moderating tradables curb price momentum.

- Policymakers acknowledged that domestic demand remains weak, with household spending, business investment, and construction activity under pressure. While still elevated, services inflation is expected to ease gradually as wage growth slows and unemployment edges higher.

- Financial conditions have eased with expectations as wholesale and retail borrowing rates adjust to lower policy settings. Bank lending data indicate a modest uptick in mortgage approvals, though broader credit demand remains subdued.

- GDP growth stalled in the middle of 2025, with high-frequency indicators showing continued weakness into the third quarter. A combination of elevated costs for essentials and falling savings continues to restrain household consumption, while global trade frictions weigh on business sentiment.

- The MPC noted that global uncertainty—particularly from US trade regulation changes and soft Chinese demand—continues to pose downside risks to export sectors, though these are partly offset by a weaker New Zealand dollar improving competitiveness.

- Subject to data confirming a sustained soft patch in activity and moderating inflation pressures, the MPC signaled further scope to reduce the OCR toward 2.25% at its next meeting on 26 November 2025, consistent with current market and Westpac forecasts.

- The next meeting is on 26 November 2025.

Next 24 Hours Bias

Medium Bearish

The Japanese Yen (JPY)

Key news events today

No major news events

What can we expect from JPY today?

The Japanese yen remains under heavy downward pressure, prompting heightened vigilance from policymakers. Large fiscal stimulus expectations, persistent yield differentials, and the prospect of market intervention are shaping yen volatility. The USD/JPY trend is bullish, but risks of abrupt moves remain if authorities signal or execute intervention.

Central Bank Notes:

- The Policy Board of the Bank of Japan met on 30–31 October and, by a clear majority vote, decided to maintain its key monetary policy approach for the upcoming period.

- The BOJ will continue to encourage the uncollateralized overnight call rate to remain at around 0.5%, in line with the prior stance.

- The gradual quarterly reduction in monthly outright purchases of Japanese Government Bonds (JGBs) remains intact, with amounts unchanged from the previous schedule. Purchases are set to decrease by about ¥400 billion per quarter through March 2026, shifting to about ¥200 billion per quarter from April to June 2026, and targeting a ¥2 trillion purchase level for Q1 2027. The bank reaffirmed its intention to maintain flexibility, with readiness to respond if market conditions warrant an adjustment.

- Japan’s economy continues to show moderate recovery, primarily led by solid capital expenditures, although export growth and corporate activity remain restrained by external demand uncertainty and the ongoing effects of U.S. trade policies.

- Annual headline inflation (excluding fresh food) accelerated to 2.9% year-on-year in September, marking the first uptick in four months and staying above the BOJ’s 2% target. Broad-based inflation persists, with food and energy cost pressures, but wage growth continues to support household consumption. Input cost pressures from the earlier surge in imports eased slightly.

- Short-term inflation momentum could moderate as food-price hikes ease, though rent, healthcare, and service-sector price increases tied to labor shortages provide support. Firms and households maintain a gradual upward drift in inflation expectations.

- For the near term, BOJ projects growth below trend as external demand stays subdued and corporate investment plans remain cautious. Still, accommodative financial conditions and steady gains in real labor income will underpin domestic consumption.

- Over the medium term, as overseas economies recover and trade conditions normalize, Japan’s growth potential should improve. Persistent labor market tightness, higher wage settlements, and rising medium- to long-term inflation expectations are expected to keep core inflation on a gradual upward trajectory, converging toward the 2% price stability target later in the forecast horizon.

- The next meeting is scheduled for 18 to 19 December 2025.

Next 24 Hours Bias

Medium Bearish

Oil

Key news events today

No major news event

What can we expect from Oil today?

The oil market remains pressured by oversupply, weak demand, and growing inventories, with only temporary support from intermittent geopolitical threats. Any substantial price recovery will require a clear shift in supply-demand fundamentals or much stronger economic growth globally. WTI crude oil futures dropped about 3% to around $59 per barrel, reflecting a steep decline after news reports indicated the US is proposing new diplomatic initiatives to end the Russia-Ukraine conflict, which could further ease geopolitical risk premiums.

Next 24 Hours Bias

Weak Bearish

The post IC Markets – Asia Fundamental Forecast | 20 November 2025 first appeared on IC Markets | Official Blog.

IC Markets – Europe Fundamental Forecast | 20 November 2025

423704 November 20, 2025 15:14 ICMarkets Market News

IC Markets – Europe Fundamental Forecast | 20 November 2025

What happened in the Asia session?

Today’s Asia session was marked by caution as investors weighed Nvidia’s earnings, watched shifts in inflation and policy across the region, and braced for delayed U.S. macro data releases. The most notable market moves were in Asian technology equities, the Japanese yen’s continued weakness, and stabilization in gold amid broad-based uncertainty. Rising Japanese bond yields and modest moves in crude further highlighted lingering risk aversion tied to fiscal and global macro pressures.

What does it mean for the Europe & US sessions?

Today’s trading sessions in Europe and the US face significant catalysts from delayed US economic data releases, particularly the critical September jobs report. Market sentiment improved following Nvidia’s strong earnings that allayed AI bubble fears, though broader concerns remain about economic momentum given mixed signals from manufacturing data, weakening oil demand, and cautious consumer behavior across major economies.

The Dollar Index (DXY)

Key news events today

Non-Farm Employment Change (1:30 pm GMT)

Unemployment Rate (1:30 pm GMT)

Philly Fed Manufacturing Index (1:30 pm GMT)

Unemployment Claims (Tentative)

Existing Home Sales (3:00 pm GMT)

What can we expect from DXY today?

The US dollar strengthened significantly amid growing uncertainty about Federal Reserve rate cuts, with the delayed September jobs report adding to market volatility. Fed minutes revealed deep divisions among policymakers about December policy, cooling expectations for further easing, and providing support for the greenback. The dollar’s rally pressured major currencies, particularly the euro and sterling, while weighing on gold and risk assets.

Central Bank Notes:

- The Federal Open Market Committee (FOMC) voted, by majority, to lower the federal funds rate target range by 25 basis points to 3.75% — 4.00% at its October 28–29, 2025, meeting, marking the second consecutive cut following the 25 basis points reduction in September.

- The Committee maintained its long-term objectives of maximum employment and 2% inflation, noting that the labor market continues to soften, with modest job creation and an unemployment rate edging higher. In comparison, inflation remains above target at around 3.0%.

- Policymakers highlighted ongoing downside risks to economic growth, tempered by signs of resilient economic activity. September’s consumer price index (CPI) came in slightly lower than expected at 3.0% year-over-year, easing inflation pressure but still warranting vigilance given tariff-driven price effects.

- Economic activity expanded modestly in the third quarter, with GDP growth estimates around 1.0% annualized; however, uncertainty remains elevated amid persistent global trade tensions and the U.S. government shutdown, which is impacting data availability.

- The updated Summary of Economic Projections anticipates an unemployment rate averaging approximately 4.5% for 2025, with headline and core personal consumption expenditures (PCE) inflation projections remaining near 3.0%, indicating a slow easing path ahead.

- The Committee emphasized its flexible, data-dependent approach and underscored that future policy adjustments will be guided by incoming labor market and inflation data. As in prior meetings, there was dissent, including one member advocating a more aggressive 50-basis-point cut.

- The FOMC announced the planned conclusion of its balance sheet reduction (quantitative tightening) program, intending to cease runoff in the near term to maintain market stability. Treasury redemption caps will remain steady at $5 billion per month, and agency mortgage-backed securities caps will remain at $35 billion.

- The next meeting is scheduled for 9 to 10 December 2025.

Next 24 Hours Bias

Medium Bearish

Gold (XAU)

Key news events today

Non-Farm Employment Change (1:30 pm GMT)

Unemployment Rate (1:30 pm GMT)

Philly Fed Manufacturing Index (1:30 pm GMT)

Unemployment Claims (Tentative)

Existing Home Sales (3:00 pm GMT)

What can we expect from Gold today?

Gold faces a critical juncture on Thursday, November 20, 2025, as markets await the delayed September US jobs report that could significantly influence Federal Reserve policy expectations and gold’s near-term direction. The precious metal is caught between competing forces: a strengthening dollar and higher real yields creating downward pressure versus persistent safe-haven demand from geopolitical tensions, equity market weakness, and structural central bank buying providing support.

Next 24 Hours Bias

Weak Bullish

The Euro (EUR)

Key news events today

No major news event

What can we expect from EUR today?

The Euro faces a challenging environment, with technical weakness, US Dollar strength, and cautious market positioning ahead of key US employment data dominating the narrative. While the ECB maintains that inflation has returned to target and the eurozone economy shows resilience, persistent risks from trade tensions, geopolitical uncertainty, and Germany’s ambitious fiscal expansion continue to weigh on sentiment.

Central Bank Notes:

- The Governing Council of the ECB kept the three key interest rates unchanged at its 30 October 2025 meeting. The main refinancing rate remains at 2.15%, the marginal lending facility at 2.40%, and the deposit facility at 2.00%. This decision reflects policymakers’ assessment that the current monetary stance remains consistent with medium-term price stability, while incoming data confirm a gradual return of inflation towards the target.

- Recent indicators point to stable price dynamics. Headline inflation remains near the 2% mark, with energy prices contained and food inflation easing slightly after earlier supply bottlenecks. Wage growth continues to moderate, contributing to the slowdown in domestic cost pressures. The ECB reiterated its commitment to a data-driven, meeting-by-meeting approach and emphasized flexibility amid uncertain global financial conditions.

- Eurosystem staff projections have not been materially altered since September. Headline inflation averages remain at 2.0% for 2025, 1.8% for 2026, and 2.0% for 2027. Recent softening in producer prices and subdued pipeline pressures suggest limited upside risks to inflation, though geopolitical tensions and potential commodity shocks continue to pose uncertainties to the outlook.

- Euro area GDP growth remains on track with earlier forecasts, projected at 1.1% for 2025, 1.1% for 2026, and 1.4% for 2027. Forward-looking indicators, including PMIs and industrial sentiment surveys, signal some stabilization in activity following weakness in the third quarter. Public investment and recovering export activity are expected to offset softer private sector demand in the near term.

- The labor market remains resilient, with unemployment rates at multi-decade lows and participation rates strong. Real income growth continues to support household spending, even as consumption growth normalizes from earlier highs. Financing conditions remain favorable, aided by stable banking sector liquidity and improved credit demand among small and medium-sized firms.

- Business sentiment remains mixed, reflecting lingering uncertainty over global trade policy and the path of US tariffs. However, easing supply chain costs and improved export competitiveness due to softer exchange rates are providing some relief to manufacturing and external-oriented sectors.

- The Governing Council reaffirmed that future decisions will depend on an integrated assessment of incoming data—covering inflation trends, financial conditions, and the state of policy transmission. The Council emphasized that no pre-set path for rates exists; keeping all options open should the economic outlook shift markedly.

- Balance sheet reduction continues smoothly, with holdings under the APP and PEPP declining as reinvestments have ceased. The ECB confirmed that the pace of portfolio runoff remains in line with its previously communicated normalization plan, supporting a gradual withdrawal of monetary accommodation in a predictable manner.

- The next meeting is on 17 to 18 December 2025

Next 24 Hours Bias

Weak Bearish

The Swiss Franc (CHF)

Key news events today

No major news event

What can we expect from CHF today?

The Swiss franc faces mixed pressures as of November 20, 2025. While Switzerland’s Q3 economic contraction of 0.5%—the first since 2023—and the resolution of the U.S. tariff dispute (reduced from 39% to 15%) have created headwinds for the currency, safe-haven demand continues to support the franc at elevated levels near multi-year highs. USD/CHF has recovered above 0.80 as the dollar strengthens on reduced Fed rate cut expectations, with the pair testing resistance at 0.8030.

Central Bank Notes:

- The SNB maintained its key policy rate at 0% during its meeting on 25 September 2025, pausing a sequence of six consecutive rate cuts as inflation stabilized and the Swiss franc remained firm.

- Recent data showed a modest rebound in inflation, with Swiss consumer prices rising 0.2% year-on-year in August after staying above zero for three consecutive months; this helped alleviate fears of deflation that were mounting earlier in the year.

- The conditional inflation forecast remains broadly unchanged from June: headline inflation is expected to average 0.2% in 2025, 0.5% in 2026, and 0.7% in 2027. The risk of a negative rate move has diminished for now, but the SNB retains flexibility should inflationary pressures weaken again.

- The global economic outlook has deteriorated further, weighed down by heightened trade tensions—especially with the U.S.—and ongoing uncertainty in key Swiss export markets.

- Swiss GDP growth moderated in Q2 after a strong Q1 boosted by front-loaded U.S. exports. The SNB expects growth to slow and remain subdued, with forecasted GDP expansion between 1% and 1.5% in both 2025 and 2026.

- Labor market sentiment in the Swiss industrial sector has softened on concerns over export competitiveness and potential adjustments to production, but the overall growth outlook stays broadly unchanged

- The SNB reiterated its readiness to respond as needed if deflation risks re-emerge, emphasizing its commitment to medium-term price stability and a robust, transparent communication policy, with the introduction of more detailed monetary policy minutes beginning in October.

- The next meeting is on 11 December 2025.

Next 24 Hours Bias

Weak Bullish

The Pound (GBP)

Key news events today

No major news event

What can we expect from GBP today?

The British pound faced a challenging session as stronger-than-expected UK inflation data (2.3% vs. 2.2% forecast) initially supported sterling but failed to deliver sustained gains. GBP/USD traded around 1.2650-1.2680, unable to break above 1.2700 resistance, while technical indicators point to further downside risks. The hotter inflation print, particularly the 3.3% core CPI reading, reinforces the Bank of England’s cautious approach to rate cuts, with markets now pricing an 82.8% probability of no change in December..

Central Bank Notes:

- The Bank of England’s Monetary Policy Committee (MPC) met on 6 November 2025 and voted by a majority of 7–2 to keep the Bank Rate unchanged at 4.00 percent for a second consecutive meeting. The decision reflects the Committee’s cautious approach as inflation remains above target, but underlying economic momentum continues to weaken. Two members maintained their votes for a 25-basis-point cut, citing further signs of labor-market softening and weak business sentiment.

- The BOE adjusted its guidance on quantitative tightening (QT), maintaining the reduced pace established in September. The planned reduction of UK government bond holdings remains at £67.5 billion over the next 12 months, leaving the current gilt balance near £550 billion. Policymakers described the recalibrated QT path as “appropriate for current market conditions,” emphasizing the importance of liquidity management amid heightened volatility.

- Headline inflation moderated slightly to 3.6 percent in October from 3.8 percent previously, driven by easing food and transport prices. However, core inflation has shown only gradual progress, holding near 3.9 percent. The MPC noted that services inflation and administered energy costs continue to exert pressure, highlighting the challenge of achieving the 2 percent target sustainably. The Committee’s latest projections see inflation falling toward 3 percent by mid-2026, with further downside expected if energy and wage dynamics continue to normalize.

- Economic activity remains subdued. Estimates place Q3 GDP growth close to zero, with both business output and consumer spending restrained. The unemployment rate has edged up to 4.8 percent, while pay growth cooled to just under 5 percent year-on-year. MPC members acknowledged that pay settlements are weakening further, signaling an easing in labor cost pressures as demand softens. Surveys from the manufacturing and services sectors suggest muted hiring intentions through year-end.

- International factors continue to complicate the policy outlook. Fluctuating oil prices—partly linked to renewed Middle East tensions—alongside fragile global demand have contributed to higher market volatility. The MPC reiterated that external shocks, including global food and energy disruptions, could temporarily slow the disinflation path but remain unlikely to derail the medium-term moderation in prices.

- The Committee assessed risks around inflation as balanced. Downside risks arise from sluggish domestic growth and declining real income momentum, while upside risks remain tied to elevated inflation expectations and stubborn services inflation. Policymakers emphasized the need for patience, maintaining that any rate cuts ahead of clear inflation progress could undermine confidence in policy credibility.

- The MPC’s overall stance remains restrictive but increasingly balanced, with future moves expected to follow a cautious, data-driven trajectory. The Committee reaffirmed that monetary policy will stay tight until there is compelling evidence that inflation is returning to the 2 percent target on a durable basis.

- The next meeting is on 18 December 2025.

Next 24 Hours Bias

Medium Bearish

The Canadian Dollar (CAD)

Key news events today

No major news event

What can we expect from CAD today?

The Canadian dollar (loonie) is experiencing notable weakness with USD/CAD trading around the 1.4040-1.4060 range, representing approximately 0.40-0.50% depreciation versus the previous session. On November 19, the pair climbed to 1.4059, marking CAD weakness following the cancellation of key U.S. employment data. The loonie has now depreciated 0.65% over the past 12 months.

Central Bank Notes:

- The Council noted that U.S. tariff tensions have eased slightly following early progress in bilateral discussions, though the external trade environment remains fragile. Businesses continue to hold back on long-term investment, with the Bank highlighting that sustained clarity on U.S. trade policy is needed to restore confidence.

- The Bank acknowledged that uncertainty persists despite the softer U.S. tone, as incoming data show limited improvement in export orders. The manufacturing sector has stabilized but remains below pre-2024 output levels, reflecting weak global demand and cautious corporate spending.

- Canada’s economy showed tentative signs of recovery in early Q4, with GDP estimated to expand by 0.3% in October after two quarters of contraction. Mining and energy activity strengthened modestly, aided by steady crude demand, while goods exports posted a fractional gain.

- Service sector growth remained uneven, supported mainly by tourism-related and technology services. However, retail spending and household consumption were subdued, constrained by slower job creation and lingering consumer caution. The Bank judged overall momentum as fragile but improving marginally.

- Housing activity showed modest reacceleration in major urban markets as mortgage rates stabilized near record lows. Nonetheless, affordability pressures and stricter lending standards continue to cap overall resale volumes, leading to only a gradual recovery in the housing sector.

- Headline CPI inflation rose to 2.1% in October, reaching the Bank’s target for the first time in six months. Higher energy prices and a modest uptick in food and shelter costs drove the increase. Core inflation measures remained stable, suggesting underlying price pressures are contained.

- The Governing Council reiterated its data-dependent stance, indicating that the current policy rate remains appropriate amid tentative growth and balanced inflation risks. Officials noted that while additional stimulus is not ruled out, the emphasis has shifted toward monitoring the sustainability of the recovery rather than immediate rate adjustments.

- The next meeting is on 17 to 18 December 2025.

Next 24 Hours Bias

WeaK Bearish

Oil

Key news events today

No major news event

What can we expect from Oil today?

Thursday marked a critical juncture for oil markets as multiple forces converged. Prices stabilized in the $59-64 range for WTI and Brent, respectively, following earlier declines driven by peace negotiation prospects between Ukraine and Russia. The approaching November 21 sanctions deadline on Rosneft and Lukoil significantly disrupted Russian oil flows, with Asian buyers cutting purchases by up to two-thirds and Russian revenues falling to 2.5-year lows.

Next 24 Hours Bias

Weak Bearish

The post IC Markets – Europe Fundamental Forecast | 20 November 2025 first appeared on IC Markets | Official Blog.

Thursday 20th November 2025: Asian Markets Surge on Tech Rally and Cooling Fed Rate-Cut Expectations

423703 November 20, 2025 15:14 ICMarkets Market News

Global Markets:

- Asian Stock Markets : Nikkei up 2.40%, Shanghai Composite up 0.38%, Hang Seng up 0.09% ASX up 1.18%

- Commodities : Gold at $4,068.29 (-0.35%), Silver at $50.905 (0.13%), Brent Oil at $63.66 (0.24%), WTI Oil at $59.42 (0.29%)

- Rates : US 10-year yield at 4.136, UK 10-year yield at 4.6010, Germany 10-year yield at 2.7103

News & Data:

- (USD) Trade Balance -59.6B to -61.3B expected

- (USD) Crude Oil Inventories -3.4M to -1.3M expected

Markets Update:

Asian markets are trading broadly higher on Thursday, lifted by strong overnight gains on Wall Street, where technology stocks rallied after upbeat earnings from Nvidia renewed confidence in the AI-driven trade. Bargain hunting also continued following recent market weakness, reversing Wednesday’s mostly lower close across Asia.

Minutes from the US Federal Reserve’s late-October policy meeting showed policymakers held “strongly differing views” on the interest rate outlook. While most members agreed rates would eventually need to be cut, several did not see another 25-basis-point reduction as likely at the December meeting. Many suggested rates may remain unchanged for the rest of the year. According to the CME FedWatch Tool, there is now a 32.8 percent chance of a December rate cut, sharply lower than nearly 94 percent a month ago.

The Australian market is sharply higher, with the S&P/ASX 200 reclaiming the 8,500 level amid gains across most sectors, led by technology. Major miners are advancing, while energy stocks lag due to weaker crude oil prices. Tech names such as Block, Xero and Zip are posting strong gains. The Aussie dollar is trading at $0.648.

Japan’s Nikkei 225 is surging more than 3 percent, snapping a four-day losing streak, boosted by exporters and tech stocks including SoftBank, Advantest and Tokyo Electron. The yen is trading in the lower 157 range.

Elsewhere, markets in South Korea, Taiwan, China and Hong Kong are higher. On Wall Street, major indexes ended modestly positive, while crude oil fell on renewed oversupply concerns.

Upcoming Events:

- 01:30 PM GMT – USD Average Hourly Earnings m/m

- 01:30 PM GMT – USD Non-Farm Employment Change

- 01:30 PM GMT – USD Unemployment Rate

The post Thursday 20th November 2025: Asian Markets Surge on Tech Rally and Cooling Fed Rate-Cut Expectations first appeared on IC Markets | Official Blog.

Trade the Euro on the Delayed Non-Farm Payrolls

423679 November 19, 2025 20:00 ICMarkets Market News

At long last, the US government is back in action, and the market will get its first major jobs data update in the New York trading session on Thursday. There has been a lot of volatility in Federal Reserve rate cut expectations in the last couple of weeks, with the market initially pricing in strongly a further 25-basis point cut from the FOMC in December, before the data vacuum weighed enough on sentiment to more than halve those expectations. Currently, the market is pricing in a 47% chance that the Fed will cut 25 basis points against 53% on a hold. These expectations could change dramatically if we see Thursday’s Non-Farm Payroll data come in significantly off expectations.

The market is pricing in the headline NFP number to come in around +60k for the month of September, with the Unemployment Rate remaining steady at 4.3% and the Average Hourly Earnings number coming in at a 0.3% month-on-month increase. Traders are expecting the impact of this data to be exacerbated due to the long delay and data vacuum that we have experienced, so anything much weaker than expected should see Fed rate cut expectations jump and the dollar fall, while an against-trend higher print should knock out the December cut and see the dollar rally strongly.

The Euro is set up nicely ahead of the data release, with technical levels close on both sides that should lead to good trading opportunities. It is currently sitting in the middle of the range on the Daily chart, with good trendline support coming in around 1.1535 and resistance around 1.1630. Results +/- 30k on the Non-Farm headline number should see these levels tested, with higher misses likely to lead to good break trade opportunities.

Resistance 2: 1.1655 – November High

Resistance 1: 1.1630 – Trendline Resistance

Support 1: 1.1535 – Trendline Support

Support 2: 1.1468 – November Low

he accuracy, completeness and timeliness of the information contained on this site cannot be guaranteed. IC Markets Global does not warranty, guarantee or make any representations, or assume any liability regarding financial results based on the use of the information in the site.

News, views, opinions, recommendations and other information obtained from sources outside of www.icmarkets.com, used in this site are believed to be reliable, but we cannot guarantee their accuracy or completeness. All such information is subject to change at any time without notice. IC Markets Global assumes no responsibility for the content of any linked site.

The fact that such links may exist does not indicate approval or endorsement of any material contained on any linked site. IC Markets Global is not liable for any harm caused by the transmission, through accessing the services or information on this site, of a computer virus, or other computer code or programming device that might be used to access, delete, damage, disable, disrupt or otherwise impede in any manner, the operation of the site or of any user’s software, hardware, data or property.

The post Trade the Euro on the Delayed Non-Farm Payrolls first appeared on IC Markets | Official Blog.

Ex-Dividend 20/11/2025

423674 November 19, 2025 17:14 ICMarkets Market News

The post Ex-Dividend 20/11/2025 first appeared on IC Markets | Official Blog.

General Market Analysis – 19/11/25

423672 November 19, 2025 15:00 ICMarkets Market News

US Stocks Drop Again – Nasdaq off 1.2%

US equities drifted lower again overnight as valuation concerns kept investors on the defensive ahead of Nvidia’s earnings release, due after the bell tonight. The Dow fell 1.07% to close at 46,091, while the S&P 500 slipped 0.83% to 6,617 and the Nasdaq dropped 1.21% to 22,432. The US dollar was little changed, with the DXY edging up 0.02% to 99.61. Treasury markets were steadier, with yields easing ahead of the latest Federal Reserve Meeting Minutes. The 2-year yield slipped 3.8 basis points to 3.573%, while the 10-year yield declined 2.5 basis points to 4.113%. Oil prices pushed higher in choppy trading as markets continued to digest the impact of sanctions on Russian crude. Brent rose 0.89% to $64.77, and WTI gained 1.25% to $60.66. Gold also found some support, lifting 0.62% off support levels to $4,069.51.

Gold to Trade on Dollar Sentiment in Coming Days

Gold has remained trading in a volatile manner in recent weeks but has stuck to a wider range as a variety of changing factors have led to strong rallies followed by equally strong descents. Recent reports that some major central bank players are now confirming – through data rather than any announcements – that they have been actively buying the world’s favourite precious metal over the last few months have answered a few questions for experienced traders with regard to the huge move up after the early September break of the previous record level. However, traders are now looking for fundamentals to reinforce moves in one direction or another. Gold bounced nicely off support levels overnight as some good buying flows came through the market, but traders are now expecting more moves on fundamentals, initially off the Fed Meeting Minutes tonight and then off the delayed September Non-Farm Payrolls data tomorrow. These should both see the dollar side of the equation dominate sentiment with regard to moves, at least for the next few sessions.

Busy Day Ahead for Traders

It’s a busier day ahead on the economic calendar today, with some key data due out across the sessions before we hit the Fed Meeting Minutes near the end of the day. Australian markets are again in focus during the Asian session, with Wage Price Index data (exp +0.8%) due out early in the day. There is key UK data due out in the European session, with the CPI figures (exp +3.5% y/y) the main market mover of a big data dump early in the day. In the US session, traders will be watching the weekly Crude Oil Inventory numbers (exp -1.9 million barrels) earlier in the day before attention shifts to the FOMC Meeting Minutes a few hours before the close and Nvidia’s highly anticipated results update.

The post General Market Analysis – 19/11/25 first appeared on IC Markets | Official Blog.