Articles

French business confidence picks up in December, boosted by manufacturing sentiment

December 18, 2025 15:14 Forexlive Latest News Market News

Well, at long last we are starting to perhaps see some improvements in French business sentiment. Confidence in this space has been languishing for well over a year already but is this an early sign of things to come? The composite business confidence estimate picks up in December, recording a reading of 98.7 – its highest since June 2024.

The jump there is largely helped by a marked improvement in manufacturing confidence (102 vs 98 previously) while services confidence remained steady (98 vs 98 previously).

This now at least sees French business confidence move closer back towards the long-term average of 100. The last time the index touched that line was all the way back in March last year.

Going back to the report by INSEE, employment conditions eased a little with the index slipping to 95 from 96 in November. The drop owes mostly to the downturn in the balance of future workforce size in the services sector.

Meanwhile, there was also a sharp rebound in he whole sector comprising retail trade and trade and repair of motor vehicles. The index there gained seven points to 104, its highest since January 2024. This rebound mainly stems from a rise in the balances related to ordering intentions.

It’s not much but it is at least potentially a start of some improvement in fortunes for the French economy. Or at least that is what the optimists will be hoping for. Political uncertainty and instability has been a bane for France for quite some time now and that won’t go away in 2026. So, expect there to continue to be strong headwinds for the economy as a whole.

But at least for now, inflation isn’t so much so a problem but domestic demand conditions are still suffering for the most part. So, any improvement in sentiment is very much welcome.

This article was written by Justin Low at investinglive.com.

Switzerland November trade balance CHF 3.84 billion vs CHF 4.32 billion prior

December 18, 2025 14:14 Forexlive Latest News Market News

- Prior CHF 4.32 billion; revised to CHF 4.20 billion

The Swiss trade surplus narrowed in November as exports were seen down 7.1% on the month while imports fell by 6.8% on the month. The Swiss numbers tend to be rather volatile, as they exclude precious metals and stones, works of art and antiques. As for Swiss watch exports, they are seen down 7.3% year-on-year in nominal terms to CHF 2.25 billion.

This article was written by Justin Low at investinglive.com.

US CPI report to overshadow key central bank decisions today

December 18, 2025 12:39 Forexlive Latest News Market News

This will be yet another unusual report release, something akin to what we saw with the labour market report earlier this week. This time around though, just be wary that the BLS will not be releasing a full report for October and so market players will have to make due with a gap between the September CPI report to this one today.

So, what does this all mean?

Well, it’s not exactly true that we won’t see any October numbers. For some context, price data collection is typically conducted via in person or by phone, which wasn’t possible during October amid the government shutdown. That being said, just over 20% of price data in the CPI basket is taken from a variety of sources that don’t necessarily require personal collection as a whole. Instead, they rely more on online prices and private data providers.

As such, if the BLS does want to try and disseminate that information as part of the report, they can choose to do so. However, it remains to be seen how they would want to format and/or furnish the release today.

It could be a case where the BLS just opts out from reporting on the month-on-month figures and focus more on the year-on-year numbers instead. Or they could just provide index numbers for some of these subcategories for November and then letting market players work things out for themselves in benchmarking that to September, with October being the missing piece.

So, we’ll have to just wait and see essentially. But Morgan Stanley is out with a note saying that: “Because of the shutdown, the individual months will not be reported, just a price level for November.”

In terms of what analysts are saying, it seems to be more or less the same story though. Core goods inflation is likely to pick up a little more towards the end of the year, owing to tariffs continuing to filter into the economy. But amid potential seasonal factors i.e. Black Friday price discounts, there could be a downside bias to the November price figures as a whole. So, just watch out for that.

Overall, the inflation picture should continue to point to some light moderation in price pressures and that likely will be the key takeaway once again when the dust settles. Barring any major surprises, traders and investors could react more strongly to the initial numbers than to the other key risk events today; that being the BOE and ECB policy decisions.

I mean, we very well expect a rate cut by the BOE and none from the ECB. So, there shouldn’t be much drama to that. As such, the US CPI report is what will likely be a stronger play for volatility in trading conditions for the day ahead.

But given time, I would expect market players to fade any major reactions to the numbers today amid data quality issues with regards to the monthly sampling for November and the limited reliability on the details for October.

So unless there is a major surprise to inflation developments, we could still look for a tamer market reaction in the bigger picture. That especially since the next Fed rate cut is only priced in for June next year. There’s no need to go rushing to price in something based on questionable data when there is still many months to go before figuring things out.

This article was written by Justin Low at investinglive.com.

investingLive Asia-Pacific FX news wrap: USD/JPY inches higher still

December 18, 2025 11:39 Forexlive Latest News Market News

- BofA warns of building stock bubble risk but sees more upside in AI

- Bank of England (BoE) set to cut rates as inflation slows, but easing seen as limited

- US approves $10bn-plus arms sales to Taiwan, China defence stocks index hits 2 mth high

- Japan signals FX vigilance, leans against yen weakness with verbal intervention

- Trump pre-Christmas $1776 check for US service members. Fiscal stimulus, at the margin.

- Honda to suspend Japan and China output as supply and demand pressures persist

- China to manage CNH liquidity, PBoC to issue CNY 40bln of 6-month bills in Hong Kong

- PBOC sets USD/ CNY mid-point today at 7.0583 (vs. prior close at 7.0450)

- South Korea flag FX volatility risks as policy divergence bites (they should call the RBI)

- Morgan Stanley sees US CPI confirming persistent inflation pressures

- BoJ is set to keep markets guessing on the terminal rate, signalling patience – preview

- Coinbase launches stock trading and prediction markets in major platform update

- Preview of the European Central Bank meeting – set to hold rates as euro zone growth firm

- Bank of Japan hike priced, forward guidance in focus – preview for Friday, December 19

- WSJ report on advice to Trump from his lawyers regarding serving a third presidential term

- New Zealand’s economy recorded a stronger-than-expected rebound in the September quarter

- investingLive Americas FX news wrap 17 Dec: Stocks continue to fall. USD ends higher

Major FX rates traded in subdued ranges through the Asian session, with markets largely marking time ahead of a heavy 24-hour run of central-bank decisions and key data releases. Volatility was limited, reflecting caution rather than conviction, as investors await clarity from multiple policy fronts.

The yen was a modest underperformer. USD/JPY ticked a little higher to around 150.80, despite, or arguably because of, only mild verbal intervention from Japan’s Chief Cabinet Secretary Minoru Kihara, who said authorities were closely watching market moves, including long-term interest rates. The lack of any concrete warning or escalation was taken as a signal that Tokyo remains uncomfortable with yen weakness but is not yet prepared to act, allowing the currency to drift softer.

Regional equities were mostly lower, tracking the soft tone on Wall Street on Wednesday, where weak price action weighed on sentiment and reinforced a defensive bias across risk assets.

Early data flow came from New Zealand, where third-quarter economic growth surprised to the upside and exceeded Reserve Bank of New Zealand forecasts. The expansion was broad-based, with investment spending showing particular strength, although household consumption lagged somewhat. While the data suggest the economy is beginning to lift itself off the canvas, markets were unconvinced. New Zealand rates edged lower and the kiwi dollar drifted modestly, reflecting lingering caution around the durability of the recovery and the near-term policy outlook.

In Washington, President Trump delivered a televised address from the White House that included several economy-related announcements. Trump said every U.S. service member will receive a one-off “warrior dividend” payment of $1,776 before Christmas, a fiscal transfer worth roughly $2.5 billion. While modest in macro terms, the move reinforces expectations of targeted fiscal support and the renewed use of direct cash payments. Trump also said he would soon name a new Federal Reserve chair who favours significantly lower interest rates, remarks likely to keep markets alert to policy-credibility risks.

The rest of Thursday brings a packed agenda. The Bank of England is expected to cut rates by 25bp to 3.75%, the ECB is seen holding policy steady, and U.S. November CPI is due. Attention then turns to Friday, when the Bank of Japan is expected to deliver a historic rate hike, to 0.75%, its highest level in three decades.

Asia-Pac

stocks:

- Japan

(Nikkei 225) -1.07% - Hong

Kong (Hang Seng) -0.44% - Shanghai

Composite +0.16% - Australia

(S&P/ASX 200) -0.07%

Bank of Japan Governor Ueda will make history tomorrow.

This article was written by Eamonn Sheridan at investinglive.com.

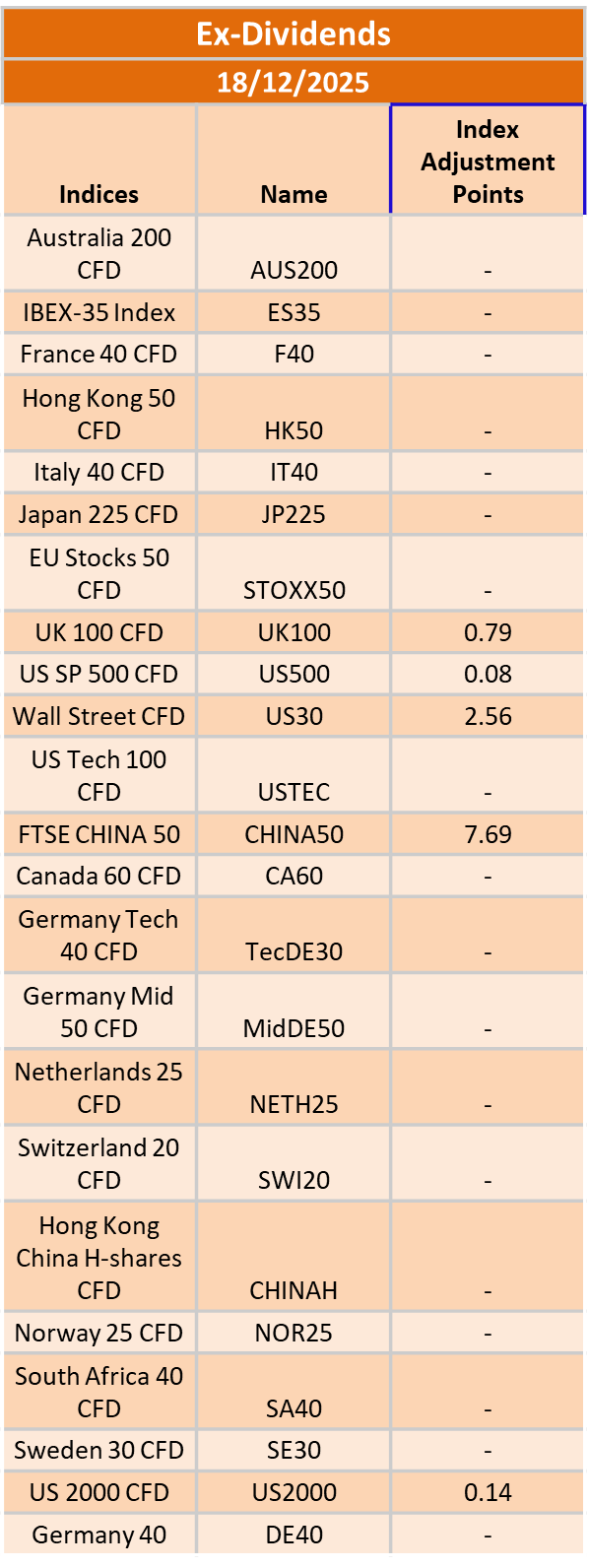

Ex-Dividend 18/12/2025

December 18, 2025 10:39 ICMarkets Market News

The post Ex-Dividend 18/12/2025 first appeared on IC Markets | Official Blog.

US approves $10bn-plus arms sales to Taiwan, China defence stocks index hits 2 mth high

December 18, 2025 10:30 Forexlive Latest News Market News

U.S. approves $10bn+ arms sales to Taiwan

- Package includes HIMARS, ATACMS, howitzers and drones

- Likely to inflame U.S.–China tensions

- China defence stocks jump on news

- Raises regional security risks

The Trump administration has approved a sweeping package of arms sales to Taiwan valued at more than $10 billion, sharply escalating military support for the island and injecting fresh tension into already strained U.S.–China relations.

The U.S. State Department announced the sales late Wednesday, coinciding with a nationally televised address by President Donald Trump, although the president did not reference China or Taiwan in his remarks. The package comprises eight separate agreements and represents one of the largest single tranches of U.S. military assistance approved for Taiwan.

At the core of the deal are 82 High Mobility Artillery Rocket Systems (HIMARS) and 420 Army Tactical Missile Systems (ATACMS), together valued at more than $4 billion. The systems mirror weaponry supplied by Washington to Ukraine during its conflict with Russia and are designed to enhance Taiwan’s long-range strike and deterrence capabilities. The package also includes around $4 billion worth of self-propelled howitzer systems and associated equipment, along with drones valued at more than $1 billion.

The announcement is likely to provoke a sharp response from Beijing, which considers Taiwan a breakaway province and has consistently opposed U.S. arms sales to the island. Such moves are typically met with diplomatic protests, military signalling and, at times, retaliatory measures targeting U.S. interests or companies.

Markets in China appeared to anticipate heightened regional tensions. China’s CSI Defence Index rose more than 2% to a two-month high following news of the approvals, reflecting investor expectations of increased domestic defence spending and procurement in response to rising geopolitical risks.

For Washington, the package reinforces a strategy of bolstering Taiwan’s defensive capabilities without formally altering long-standing policy frameworks. For Taiwan, the systems enhance deterrence but also raise the stakes in cross-strait relations at a time of elevated military activity in the region.

While the arms sales are unlikely to trigger immediate market dislocation beyond the defence sector, they add to a broader backdrop of strategic rivalry that continues to shape regional security, trade flows and investor sentiment across Asia.

This article was written by Eamonn Sheridan at investinglive.com.

Trump pre-Christmas $1776 check for US service members. Fiscal stimulus, at the margin.

December 18, 2025 09:30 Forexlive Latest News Market News

Trump announces “warrior dividend” for service members

- .

U.S. President Donald Trump said more than one million U.S. service members will receive a special one-off payment before Christmas, announcing what he described as a “warrior dividend” worth $1,776 per person.

Speaking at a campaign event, Trump said the payment would be made to every active-duty service member, framing the move as both recognition of military service and direct financial support. The amount, a reference to the year of American independence, was presented as symbolic as well as practical, delivering cash support ahead of the holiday period.

While details around funding and implementation were not immediately provided, the proposal carries clear fiscal and economic implications. A payment of this scale would amount to a stimulus injection of roughly $1.8 billion into household incomes, concentrated among a group with a high propensity to spend. Delivered before year-end, the payments would likely provide a short-term boost to consumer spending, particularly in retail and services sectors tied to holiday demand.

The announcement also fits within a broader pattern of using targeted fiscal transfers as an economic and political tool. Direct payments have proven effective in quickly supporting consumption, even when modest in size, and can help cushion households against cost-of-living pressures without requiring broader structural policy changes.

From a policy perspective, the proposal may raise questions about fiscal discipline and precedent, particularly if similar payments are extended to other groups. However, supporters may argue that the targeted nature of the dividend limits its inflationary impact compared with broader stimulus measures, while reinforcing support for military personnel.

Markets are unlikely to view the proposal as macro-significant in isolation, given its relatively small scale relative to the U.S. economy. Nonetheless, it adds to the broader narrative of renewed fiscal activism and the willingness of policymakers to deploy direct cash transfers as both an economic lever and a political signal.

Further clarity on timing, funding mechanisms and legislative backing will be required before the proposal can be fully assessed.

—

Trump has added more, promising to announce the next chair of the Federal Reserve ‘soon’. Trump says the new Fed Chair will believe in lower interest rates ‘by a lot’. Bad grammar, but a clear message of what Trump wants regardless.

This article was written by Eamonn Sheridan at investinglive.com.

Honda to suspend Japan and China output as supply and demand pressures persist

December 18, 2025 09:14 Forexlive Latest News Market News

Honda to suspend production in Japan and China

- Company cites ongoing chip shortages

- Demand conditions may also be a factor

- Shares fall on renewed uncertainty

- Output recovery risks persist

Honda Motor Co. is set to suspend vehicle production across parts of Japan and China in the coming weeks, underscoring continued fragility in global automotive supply chains and raising fresh questions about demand conditions in key markets.

The Japanese automaker said it will halt output at domestic plants on January 5 and 6, while production at all three Guangqi Honda joint-venture facilities in China will be suspended from December 29 through January 2. Honda cited ongoing semiconductor shortages as the primary reason for the stoppages, a reminder that chip supply disruptions continue to weigh on manufacturing schedules despite earlier signs of improvement.

The move comes as a setback after Honda had indicated production was expected to normalise from late November. Instead, the latest suspensions suggest that supply constraints remain unresolved, complicating efforts to restore output volumes and stabilise inventories.

However, the interruptions may also prompt scrutiny of underlying demand conditions. Auto demand in parts of Asia has softened amid higher borrowing costs, cautious consumer spending and uneven economic momentum. In that context, temporary production halts can serve a dual purpose, helping manufacturers manage inventories and align output more closely with sales trends. While Honda has not explicitly pointed to weaker demand, the overlap between lingering supply issues and a more challenging demand backdrop suggests the stoppages may reflect a broader recalibration rather than purely logistical disruption.

The announcement weighed on investor sentiment, with Honda shares falling around 1.5% in Tokyo trading following media reports. The market reaction reflects concern that prolonged supply constraints — combined with softer demand — could continue to cap earnings momentum into the new year.

China remains a critical market for Honda, both in terms of sales volumes and manufacturing scale, making the suspension of its joint-venture plants particularly notable. More broadly, the episode highlights how global automakers remain exposed to both supply-side bottlenecks and cyclical demand risks, even as the industry adapts by prioritising higher-margin models and adjusting production mixes.

I’m just gonna stick to their bikes 😉

This article was written by Eamonn Sheridan at investinglive.com.

Morgan Stanley sees US CPI confirming persistent inflation pressures

December 18, 2025 07:45 Forexlive Latest News Market News

The TL;DR:

- Morgan Stanley expects CPI to confirm firm inflation pressures

- Core CPI seen near 3.0% y/y in November

- Shelter and goods prices remain resilient

- Data limitations reduce monthly detail

- Supports cautious Fed policy outlook

U.S. consumer price data due on Thursday, December 18, is expected to confirm that underlying inflation pressures remain firm, according to Morgan Stanley, even as data limitations complicate interpretation of the latest release.

In a note previewing the report, Morgan Stanley said it expects core inflation to show continued resilience, driven by a rebound in shelter costs and ongoing firmness in goods prices. The bank estimates that core CPI inflation averaged around 0.28% month-on-month across October and November, a pace that would lift core inflation to roughly 3.0% year-on-year in November.

Headline inflation is also expected to remain elevated, averaging around 0.26% m/m over the same two-month period, reflecting similar underlying strength. Morgan Stanley said these readings point to persistent inflation momentum that remains inconsistent with a rapid return to the Federal Reserve’s 2% target.

However, the November CPI release comes with an important caveat. Due to the government shutdown, individual monthly prints for October and November will not be published. Instead, markets will receive only a November price level, significantly reducing transparency around month-to-month inflation dynamics. While this limits granularity, Morgan Stanley said the broader signal still points to firm underlying pressures.

Shelter inflation is expected to rebound after a period of moderation, reflecting the well-known lag between market rents and official inflation measures. Goods prices, which had previously contributed to disinflation, are also expected to remain resilient, suggesting that inflation pressures are not confined solely to services.

Morgan Stanley cautioned that the lack of detail may temper market reactions at the margin, but said the overall message should reinforce the Federal Reserve’s cautious approach to policy easing. With core inflation tracking around 3%, the data are unlikely to provide policymakers with the confidence needed to signal an imminent shift toward rate cuts.

In Morgan Stanley’s view, even a technically constrained CPI release is likely to validate the narrative that inflation remains sticky, keeping pressure on the Fed to maintain a restrictive stance into early 2026.

–

Meanwhile, the Wall Street Journal have published their survey of expectations:

The Journal’s noted Fed watcher, Nick Timiraos with his summation:

This article was written by Eamonn Sheridan at investinglive.com.

WSJ report on advice to Trump from his lawyers regarding serving a third presidential term

December 18, 2025 05:30 Forexlive Latest News Market News

President Donald Trump has been presented with a draft manuscript by prominent constitutional lawyer Alan Dershowitz examining whether the U.S. Constitution definitively bars a president from serving a third term, reopening a long-settled legal and political debate around presidential term limits.

The Wall Street Journal (gated) carries the report.

According to Dershowitz, who previously represented Trump during his first-term impeachment proceedings, the president received and discussed the draft during a recent Oval Office meeting. The forthcoming book, titled “Could President Trump Constitutionally Serve a Third Term?” and slated for publication next year, argues that while the Constitution clearly limits presidents to two elections, it may be ambiguous on other pathways to a third term.

“The Constitution is not clear on whether a president can become a third-term president,” Dershowitz told The Wall Street Journal, emphasising that the question is less about electoral limits and more about succession and procedural outcomes. Trump, he said, treated the discussion as an intellectual exercise and moved on to other topics, adding that he does not believe the president intends to pursue a third term.

Publicly, Trump has maintained that the Constitution is “pretty clear” that he cannot run again, a position echoed by White House chief of staff Susie Wiles in a recent interview. However, comments from other administration figures have kept the issue alive. White House spokeswoman Abigail Jackson said the country would be “lucky” to have Trump serve for a longer period, stopping short of endorsing a legal pathway.

Dershowitz’s book outlines several hypothetical scenarios, including one in which a third election could ultimately be decided by Congress if Electoral College members abstain from voting. Such an outcome would be unprecedented, and the National Constitution Center notes that elector abstentions have been extremely rare and never resulted in a congressional decision.

Legal scholars remain sceptical. Hofstra law professor James Sample described the Electoral College scenario as “absurd,” though he outlined a more plausible, if highly unconventional, route involving allies winning the presidency, resigning, and elevating Trump through the line of succession.

We’ve all been following along with Trump’s economic management since he resumed office in January this year. Policy volatility has been reflected in market volatility, rising inflation, and slowing job growth. Seven more years of this may lie ahead.

This article was written by Eamonn Sheridan at investinglive.com.

New Zealand’s economy recorded a stronger-than-expected rebound in the September quarter

December 18, 2025 05:14 Forexlive Latest News Market News

TL; DR summary:

- New Zealand GDP rebounded more than expected in Q3

-

Production-based GDP rose 1.1% q/q vs 0.9% forecast

- Expenditure-based GDP up 1.3% q/q, also beating estimates

-

Annual-average growth remains negative

NZD reaction modest, reflecting backward-looking nature of data

The investingLive economic calendar gives both the expected and priors if you’d like to keep track:

More detail:

New Zealand’s economy recorded a stronger-than-expected rebound in the September quarter, with official data showing solid gains across both production- and expenditure-based measures.

The quarterly bounce points to a period of improving activity momentum after earlier weakness, likely supported by resilient household spending and a stabilisation in domestic demand conditions through late winter. However, the broader picture remains more mixed. On an annual-average basis, production-based GDP was still down 0.5% in Q3 from a year earlier (i.e. Q3 2025 vs. Q3 2024), underscoring that the economy has yet to fully recover from the earlier downturn.

Market reaction was muted. The New Zealand dollar briefly ticked higher following the release, with NZD/USD popping only a handful of points before settling back, reflecting limited conviction that the data materially alters the near-term macro or policy outlook.

That restrained response highlights an important caveat around GDP data: it is inherently backward-looking. Today’s release largely captures economic conditions from several months ago, before more recent shifts in financial conditions, global growth dynamics, and evolving monetary-policy expectations. In a fast-moving environment, quarterly GDP tends to confirm what has already happened rather than signal what is happening now.

GDP also remains prone to revisions, sometimes meaningful ones, which can further temper its value as a real-time guide for investors or policymakers. As such, while the Q3 upside surprise adds context around New Zealand’s recent growth trajectory, markets are likely to place greater weight on higher-frequency indicators — particularly inflation, labour-market data, business surveys and financial-conditions metrics — when assessing the Reserve Bank of New Zealand’s next move.

This article was written by Eamonn Sheridan at investinglive.com.

investingLive Americas FX news wrap 17 Dec: Stocks continue to fall. USD ends higher

December 18, 2025 04:39 Forexlive Latest News Market News

- End of Day Summary: Tech Rout Batters S&P 500 and Nasdaq

- Silver Price Analysis: XAGUSD Hits Record Highs (Up 130% in 2025)

- The US treasury sells $13 billion of 20 year bonds at a high yield of 4.798%

- What if the chart of US oil production is wrong?

- Oracle is getting crushed again and is down nearly 50% since September

- EIA weekly US crude oil inventories -1274K vs -1066K expected

- China won’t need ASML’s chip-building machines for long

- Funny how none of the Fed candidates are talking about the one-off drop in oil prices

- Fed’s Waller: Jobs market is very soft, current payrolls growth not good

- investingLive European FX markets wrap: UK inflation cools just before BOE decision

- USDINR Technical Analysis: RBI intervenes to stop the Rupee selloff. Another failed try?

- Eurozone November final CPI +2.1% vs +2.2% y/y prelim

Key Takeaways for markets today

-

USD/JPY Rally: The Yen was the biggest mover vs the USD, pushing USD/JPY up +0.65% to 155.71. The BOJ will announce its interest rate decision on Friday.

-

Sterling Slump: GBP/USD fell -0.34% to 1.3375 after softer-than-expected UK inflation data cemented bets for a BoE rate cut tomorrow.

-

Commodity Strength: Silver surged it is up 4.34% and Oil rallied +2.92%, while Gold posted a gain of 1%

USDJPY: The Big Mover

The Japanese Yen struggled significantly today, finishing as the worst of the major currencies against the dollar. The pair rallied +0.65% to trade at 155.71, extending from lows of 154.52 earlier in the session.

-

The Catalyst: While Machinery Orders and Exports beat expectations, Imports missed. However, the focus remained on policy. The Bank of Japan will enter interest rate decision with expectations of a 0.25% rise in the targeted rate

GBPUSD: Inflation Data Weights on the Pound

The GBPUSD came under pressure earlier in the day after UK CPI data missed expectations but rebounded most of its sharp declines. The low for the day reached 1.3312. The current price is trading at 1.3375 with a high for the day near 1.3426.. Technically, the price is ending the day back above its 200 day moving average at 1.3346 and its 100 day moving average at 1.3357.

-

The Data: Headline CPI eased to 3.2% (vs. 3.5% expected), driven largely by falling food prices. Core CPI dipped -0.2% month-over-month.

-

The Impact: The report solidified market expectations for a 25 basis point rate cut from the Bank of England when the announcer interest rate decision tomorrow, with markets now assigning a ~99.7% chance of a cut, up from 91% pre-release.

EURUSD: Flat Ahead of the ECB

The EURUSD moved lower in sympathy with the Grecovered most of the declines in the North American session to end the day marginally lower by -0.06% .

-

The Outlook: Traders appear to be in a holding pattern ahead of Thursday’s ECB meeting, where rates are expected to remain unchanged. However, economic clouds persist as the German Ifo index hit its lowest level since May. Nevertheless expectations are for ECB’s Lagarde to reiterate the bank will remain data -dependent

USDCAD: Technical Buyers Gain Control

The USD/CAD pair rose +0.21% to 1.3783, but the technical story is the highlight.

-

Chart Watch: After multiple failed attempts where sellers defended the 100-hour moving average, buyers finally broke above this key resistance level today. The focus now shifts to whether they can sustain this momentum toward the 1.3800 level (200-hour MA). So far, that moving average has held resistance, putting the pair in a more neutral position above its 100 hour moving average at 1.3768, but below its 200 hour moving average at 1.300

Fed Governor Waller Signals Need for Rate Cuts Amid Soft Labor Market

Fed Governor Christopher Waller delivered a bearish assessment of the current economy, specifically characterizing the jobs market as “very soft” with payroll growth that is “not good.” He argued that this labor market weakness supports the case for continued interest rate cuts, estimating that the current policy rate remains 50 to 100 basis points above the neutral level. While acknowledging that inflation sits slightly above target, Waller expressed confidence that price pressures are under control, expectations remain anchored, and inflation should decline over the next few months. He advocated for proceeding at a “moderate pace” rather than taking dramatic action, and noted that while tariffs likely did not cause the current labor weakness, he remains hopeful for a stronger economic year in 2026.

Commodities & Crypto

-

Silver: The standout performer, rallying $2.70 or 4.25% at $66.44

-

Oil (USOIL): Gained $1.58 and $56.85.

-

Gold: Ticked higher by $42.92 or 1.0% at $4345

-

Bitcoin: felt $-2066 or -2.35% to $85,775.

Stocks slumped led by the tech/AI/chips

-

Dow Jones Industrial Average (DJI): Down -243.51 points (-0.51%) to 47,870.75.

-

S&P 500 (SPX): Down -78.34 points (-1.15%) to 6,721.92.

-

Nasdaq Composite (IXIC): The biggest loser, falling -410.71 points (-1.78%) to 22,700.75.

-

Russell 2000 (RUT): Small caps were not spared, dipping -28.72 points (-1.14%) to 2,490.58.

This article was written by Greg Michalowski at investinglive.com.