Articles

WH economic advisor Hassett: There is plenty of room to cut rates

December 16, 2025 21:30 Forexlive Latest News Market News

WH economic advisor Kevin Hassett is speaking on CNBC and says:

- There is plenty of room to cut rates

- US rates are out of touch with the rest of the world

- on the jobs data sees a solid upward trajectory.

- Trump thinks interest rates could be lower.

- If I were there, I’d have to negotiate with the rest of the committee.

- Fed would have to see what kind of consensus could be reached.

- Thinks we can reach 3% growth and 1% inflation again

- Deficit reduction is a key to the economy to lower rates.

- We are pretty positive that the Supreme Court will rule in our favor, and if not we have backup plans.

- We have deals 232s and 301s to use as a backstop for tariffs if the Supreme Court rules against the tariffs.

- If Trump has a good reason, and I agree with it, I will present it to the others at the Fed

- Need consensus based on facts, data.

- On jobs data, he is bullish on 2026

- The jobs data was colored by the governement shutdown.

- ON GDP growth, looking at supply side, need to have north of 4%

- On jobs, AI, seeing AI-trained workers have increased their productivity and wages

Earlier today, The latest US jobs and retail sales data painted a mixed picture of the economy, shaped in part by distortions from the recent government shutdown. Nonfarm payrolls showed a decline in October followed by a rebound in November, making it difficult to gauge the true trend in hiring, while the unemployment rate moved up to 4.6% from 4.4% which could be a worry but keep the Fed on the downside tilt.

On the consumer side, October retail sales were flat at the headline level, but the control group rose a solid 0.8%, pointing to firmer underlying demand that feeds directly into GDP. Together, the reports suggest moderating but still resilient economic momentum, leaving markets data-dependent and keeping the focus on whether growth can remain supported without reigniting inflation pressures.

For your guide:

- Section 301 and Section 232 are two US trade-law tools used to impose tariffs, but they serve different purposes and carry different market implications. Section 301 of the Trade Act of 1974 is aimed at addressing unfair foreign trade practices, such as intellectual property theft, forced technology transfers, or discriminatory policies. Under Section 301, the US Trade Representative (USTR) investigates whether another country’s practices are unreasonable or burden US commerce and, if so, can impose targeted tariffs, quotas, or other trade restrictions. These measures are often country-specific and product-specific, and they tend to be used as negotiating leverage in broader trade talks.

- Section 232 of the Trade Expansion Act of 1962, by contrast, is grounded in national security concerns. It allows the US Department of Commerce to investigate whether imports of certain goods—such as steel, aluminum, autos, or critical supply-chain items—threaten national security. If a risk is found, the president can impose tariffs or quotas regardless of country, making Section 232 actions broader and more structural. Markets typically view Section 232 tariffs as more persistent and harder to unwind, since they are justified on security grounds rather than trade imbalances.

For traders and markets, Section 301 tariffs are often seen as tactical and negotiable, while Section 232 tariffs are viewed as strategic and long-lasting. Both can affect inflation, supply chains, corporate margins, currencies, and risk sentiment, but Section 232 actions generally

This article was written by Greg Michalowski at investinglive.com.

US Retail sales for October rises by 0.0% versus 0.1% estimate

December 16, 2025 20:39 Forexlive Latest News Market News

Retail Sales data for the month of October 2025

- Prior month retail sales (September) 0.2% revised to 0.1%

- Retail sales for the month of October 0.0% versus 0.1% estimate.

- Retail sales ex autos 0.4% vs 0.3% expected. Prior month 0.3% revised lower to 0.1%

- Retail sales ex autos and gas 0.5% vs 0.0% last month (revised from 0.1%).

- Control group (feeds into US GDP) 0.8% vs 0.4% estimate. Last month -0.1%

Looking at some of the details from the line items:

-

Motor vehicle & parts dealers: -1.6% — a notable drag on the headline, reflecting weaker auto demand.

-

Furniture & home furnishings: +2.3% — strong rebound, pointing to resilience in discretionary household spending.

-

Electronics & appliance stores: +0.7% — moderate improvement after prior softness.

-

Building materials & garden supplies: -0.9% — continued weakness tied to softer housing-related activity.

-

Food & beverage stores (groceries): +0.3% — steady essential spending.

-

Health & personal care: -0.6% — pullback after strong gains in prior months.

-

Clothing & accessories: +0.9% — discretionary spending improved modestly.

-

Sporting goods, hobby, books: +1.9% — solid gain, supporting the idea of selective discretionary strength.

-

General merchandise stores: +0.5% — steady broad-based retail activity.

-

Nonstore retailers (online): +1.8% — e-commerce remained a key growth driver.

-

Food services & drinking places: -0.4% — slight decline, hinting at some consumer caution on services spending.

Top gainers (month-over-month)

-

Furniture & home furnishings: +2.3%

-

Sporting goods, hobby, books: +1.9%

-

Nonstore retailers (online): +1.8%

-

Clothing & accessories: +0.9%

-

Electronics & appliance stores: +0.7%

-

General merchandise stores: +0.5%

-

Retail sales ex-autos: +0.4%

-

Food & beverage stores (groceries): +0.3%

-

Retail sales ex-gas: +0.1%

Top decliners (month-over-month)

-

Motor vehicle & parts dealers: -1.6%

-

Building materials & garden supplies: -0.9%

-

Gasoline stations: -0.8%

-

Health & personal care stores: -0.6%

-

Food services & drinking places: -0.4%

Unchanged

-

Retail & food services (headline): 0.0%

Trader takeaway: gains were concentrated in discretionary and online spending, while autos and housing-related categories dragged, explaining the flat headline despite healthier underlying demand.

———————————————————————————————————————————

US retail sales: What the report tells traders about the consumer and growth

Why retail sales matter

When on schedule (today’s data is from October) US retail sales offer one of the clearest, most timely reads on consumer demand, which drives roughly two-thirds of overall US economic activity. Because the data are released monthly and feed directly into GDP calculations, markets often use the report to reassess growth momentum, Fed policy expectations, and near-term direction for yields, equities, and the US dollar.

Understanding the key components

The headline retail sales figure measures overall spending but can be volatile due to autos and gasoline. For that reason, traders focus more closely on retail sales ex-autos, which provide a cleaner signal of underlying demand, and the control group (excluding autos, gas, building materials, and food services), which feeds directly into GDP’s personal consumption component. A strong control group typically signals solid real economic growth, while weakness can quickly raise recession or slowdown concerns.

What the category breakdown reveals

The internal composition of the report is often as important as the headline. Strength in discretionary categories such as online sales, restaurants, and general merchandise suggests confident consumers and healthy labor income.

By contrast, weakness across multiple categories or reliance on essentials can indicate consumers are becoming more cautious, even if the headline number looks stable.

How traders use the data

For markets, strong retail sales tend to support higher Treasury yields and a firmer USD, particularly if paired with signs of rising prices or wages. Soft or slowing sales usually weigh on yields and the dollar, reinforcing expectations for Fed easing. Ultimately, traders use the report to judge whether the US consumer is powering growth, merely sustaining it, or beginning to pull back, shaping both short-term market moves and broader macro positioning.

This article was written by Greg Michalowski at investinglive.com.

US November non-farm payrolls +64K vs +50K expected

December 16, 2025 20:39 Forexlive Latest News Market News

- September was 119K

- October was -105K (just released)

- Unemployment rate 4.6% vs 4.4% expected

- Prior unemployment rate 4.4%

- Participation rate 62.5% vs 62.4% prior

- U6 underemployment rate 8.7% vs 8.0% prior

- Average hourly earnings +0.1% m/m vs +0.3% expected

- Average hourly earnings +3.5% y/y vs +3.6% expected

- Average weekly hours 34.3 vs 34.2 expected

- Change in private payrolls +69K vs +45K expected

- Change in manufacturing payrolls -5K vs -5K expected

- Government payrolls -5K vs +22K in September

The market was pricing in a 48% chance of a March cut before the report. USD/JPY was trading at 154.65 before the data and S&P 500 futures were down 8 points.

This article was written by Adam Button at investinglive.com.

Locked and loaded for the return of non-farm payrolls

December 16, 2025 20:14 Forexlive Latest News Market News

It’s been a long wait for the return of US economic data but we are finally here with November non-farm payrolls and October retail sales due at the bottom of the hour. The jobs report is the most up-to-date and the most meaningful. I wonder if the Fed got a nod that it was going to be a poor reading and that tilted them towards cutting rates.

In any case, the consensus is +50K from +119K previously. The BLS noted that the standard errors in this report will be larger than normal because of missing data from the shutdown, so be prepared for anything. A good check will be on the unemployment rate, which is projected to stay flat at 4.4%.

Retail sales are expected up 0.1% in October with the control group up 0.4%. In earnings season, companies were mostly upbeat on the consumer but there were certainly indications of K-shaped spending, with McDonald’s and Walmart highlighting the struggles of low-income consumers.

For more, see the investingLive economic calendar.

This article was written by Adam Button at investinglive.com.

US Treasury Secretary Bessent: Expect new Fed chair in early January

December 16, 2025 20:14 Forexlive Latest News Market News

KEY POINTS:

- Expects new Fed chair announcement in early January

- US Supreme Court ruling on tariffs also expected in early January

- Says Warsh and Hassett both very qualified for the job

- Expects substantial drop in inflation in the first half of 2026

- US-China relations remain positive

US Treasury Secretary, Scott Bessent, spoke in a Fox Business interview and commented on the upcoming Fed chair announcement and the US Supreme Court ruling on tariffs. Both decisions are expected in early January.

Bessent also added that Warsh and Hassett are both “very very qualified” for the job, which further confirms that it’s going to be either one of them.

Warsh recently overtook Hassett as favorite following a CNBC report saying that “Hassett candidacy was running into pushback from people close to Trump”. Warsh is also seen as a better pick in Wall Street.

Whoever it’s going to be, the new Fed Chair will still have only one vote, and monetary policy decisions are made on a majority basis. It will just make the FedWatching job more interesting as traders will need to closely follow the voters’ views on economy and policy, and monitor the economic developments.

That could bring more volatility and trading opportunities as expectations will likely swing with every comment and economic report.

This article was written by Giuseppe Dellamotta at investinglive.com.

investingLive European FX news wrap: UK jobs data soft but wages remain high, NFP next

December 16, 2025 19:39 Forexlive Latest News Market News

- Long stocks and gold are the most crowded trades according to BofA’s survey

- USDINR Technical Analysis: Key resistance reached, US NFP in focus next

- Eurozone October trade balance €18.4 billion vs €19.4 billion prior

- Germany December ZEW survey current conditions -81.0 vs -80.0 expected

- Major currencies little changed, eyes on US data

- UK December flash services PMI 52.1 vs 51.6 expected

- Italy November final CPI +1.1% vs +1.2% y/y prelim

- Eurozone December flash services PMI 52.6 vs 53.3 expected

- Germany December flash manufacturing PMI 47.7 vs 48.5 expected

- France December flash services PMI 50.2 vs 51.1 expected

- European indices hold lower at the open amid more cautious market mood

- What are the main events for today?

- Eurostoxx futures -0.5% in early European trading

- UK October ILO unemployment rate 5.1% vs 5.1% expected

- FX option expiries for 16 December 10am New York cut

- US futures keep lower at the tail end of Asia trading

- Reminder: US jobs data will be due today

- US Senate delays crypto market structure bill to 2026, as expected but still disappointing

The main highlight of the session was the UK labour market report. The unemployment rate ticked higher to 5.1% vs 5.0% prior as expected with payrolls declining once again. Wage growth, on the other hand, surprised to the upside, which could validate BoE’s Greene views that wage setting might have indeed changed.

The UK PMIs showed kind of the same with the commentary citing lacklustre growth, worryingly widespread job losses and renewed upturn in selling price inflation across both goods and services. Rising staff costs were reported as the key concern.for businesses. The pound strenghtened on a slightly hawkish repricing as the total easing for 2026 pulled back from 64 bps to 56 bps.

We had also the Eurozone PMIs which surprised to the downside. The main drag was once again Germany as the French PMIs were better than expected. The data didn’t change anything for the ECB though as it’s seen on hold well into 2027.

In the American session, it goes without saying that all eyes will be on the US NFP report and nothing else will matter. In fact, despite having also the US Flash PMIs on the agenda, the market will highly likely trade based on the US jobs report.

The November Non-Farm Payrolls is expected at 50K vs 119K prior, while the Unemployment Rate is expected to remain unchanged at 4.4%. The Average Hourly Earnings Y/Y is expected at 3.6% vs 3.8% prior, while the M/M figure is seen at 0.3% vs 0.2% prior.

There’s been lots of talk that this report could be noisy as the data collection process was affected by the shutdown. Moreover, Fed Chair Powell said in the press conference that they think job gains have been overstated by 60K in recent months and that they think there’s a negative 20K in payrolls per month.

Therefore, the Unemployment Rate will probably be the most important metric to look at in terms of market reaction, but big deviations in payrolls will also catch market’s attention.

This article was written by Giuseppe Dellamotta at investinglive.com.

Long stocks and gold are the most crowded trades according to BofA’s survey

December 16, 2025 18:45 Forexlive Latest News Market News

KEY POINTS:

- Long Mag 7 is the most crowded trade for 54% of participants

- Long gold takes the second spot at 29%

- Global investors are the most bullish in 3 and a half years due to “run it hot” macro and policy expectations

- Allocation to stocks and commodities at the highest since 2022

- BofA says positioning is a “big headwind” for risk assets

- AI bubble remains the biggest tail risk

The Bank of America Fund Manager Survey is a monthly global poll of institutional investors, revealing sentiment, asset allocation and economic expectations to gauge market positioning and potential crowded trades.

THE REASON FOR SUCH EXPECTATIONS:

In the latest survey, we can see that Mag 7 and gold are the most crowded trades driven by the “run it hot” macro and policy expectations. That shouldn’t be surprising given Trump’s expansionary policies and continues attacks on the Fed to lower interest rates.

On the other hand, the Fed is also not doing much to counter the expectations by keeping a dovish reaction function. In fact, Fed Chair Powell in its latest press conference not only downplayed the inflation risk but emphasized the labour market weakness, suggesting that there’s more tolerance for higher inflation than for weaker labour market.

And adding to that, he stated that the debate among FOMC members is just about how much more to cut. This is called a “dovish reaction function” because they will cut rates in case we see more weakness in the data but won’t do anything in case things strengthen.

REPRICING IN RATE CUT BETS INFLUENCES THE SHORT-TERM:

This remains a tailwind for risk assets and gold in the medium-term. In the short-term, the repricing in the dovish expectations is what triggers the pullbacks/corrections.

In fact, the market’s expectations were very dovish going into the October’s FOMC decision, but Powell’s statement that a December cut was not a foregone conclusion triggered a repricing that weighed on risk assets. As soon as Fed’s Williams hinted that a December cut was coming, we saw a strong rebound across the board.

Now, we are in the same situation. We have the market pricing in 58 bps of easing by the end of 2026. That’s 33 bps more than what the Fed projected. This week we get the US NFP and CPI reports. The market might not like strong data as it would trigger a hawkish repricing in interest rate expectations and lead to a deeper pullback. On the other hand, benign or even soft data will highly likely support risk assets.

This article was written by Giuseppe Dellamotta at investinglive.com.

Germany December ZEW survey current conditions -81.0 vs -80.0 expected

December 16, 2025 17:14 Forexlive Latest News Market News

- Prior -78.7

- Economic sentiment 45.8 vs 38.7 expected

- Prior 38.5

The current conditions index might show a slight decline but there is a major beat on the expectations outlook. So, that really outweighs the headline reading here. ZEW notes that expectations have become more positive and that chances for a recovery of the economy are looking good, which is being reflected in the sentiment among investors. The key boon of course being a more expansive fiscal policy, which is expected to provide new momentum to the German economy.

That’s a positive note at least but nothing that will get the ECB moving just yet as German price pressures remain a key sticking point. EUR/USD remains little changed on the day at 1.1757 currently.

This article was written by Justin Low at investinglive.com.

Eurozone October trade balance €18.4 billion vs €19.4 billion prior

December 16, 2025 17:14 Forexlive Latest News Market News

- Prior €19.4 billion; revised to €18.4 billion

Compared to the month of October last year, exports to the US are seen down nearly 15% this October while imports are up just a little over 4%. That sees the trade surplus with the US narrow in October this year to €11.2 billion with it being €19.5 billion in 2024. Something, something tariffs I guess.

This article was written by Justin Low at investinglive.com.

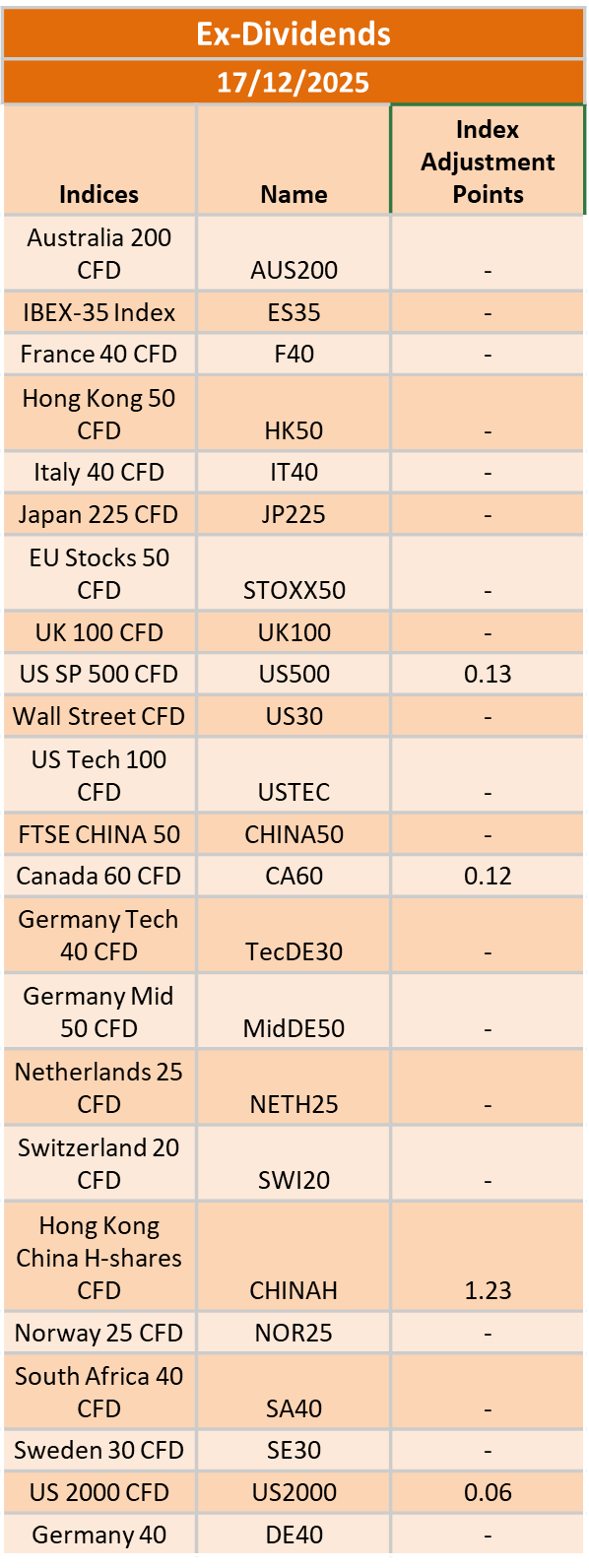

Ex-Dividend 17/12/2025

December 16, 2025 17:14 ICMarkets Market News

The post Ex-Dividend 17/12/2025 first appeared on IC Markets | Official Blog.

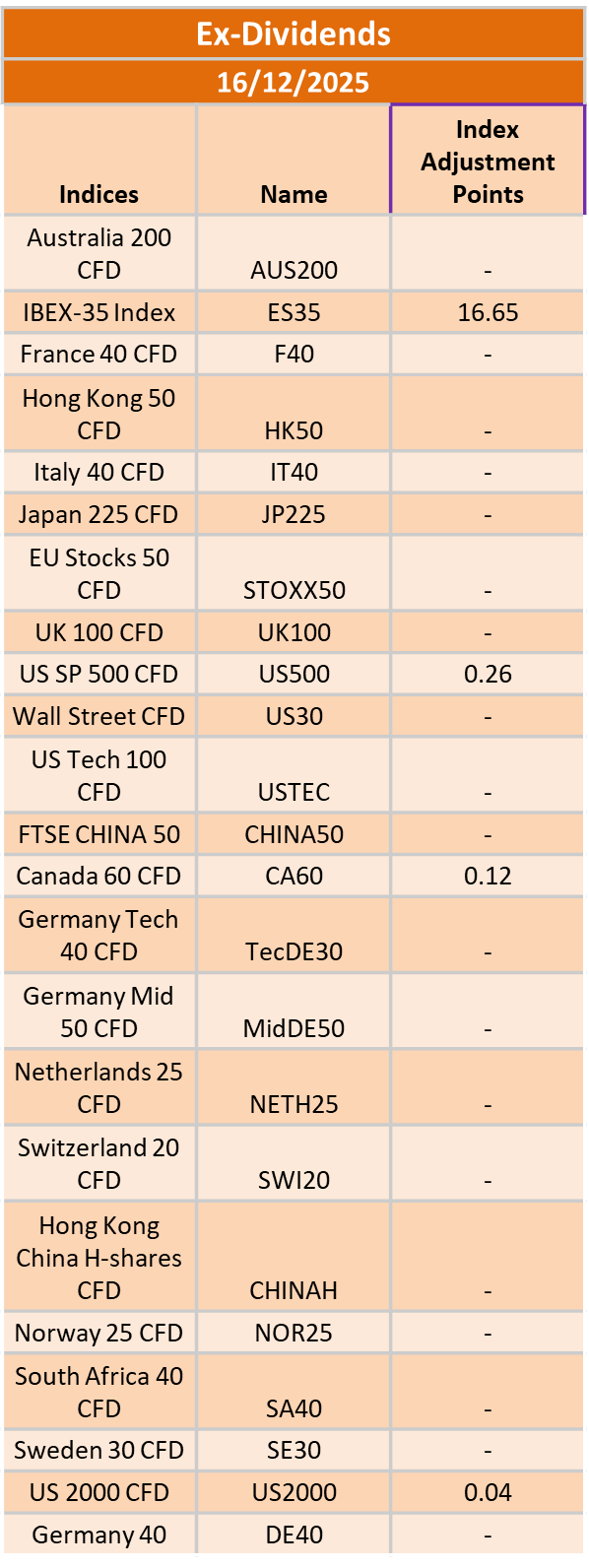

Ex-Dividend 16/12/2025

December 16, 2025 17:14 ICMarkets Market News

The post Ex-Dividend 16/12/2025 first appeared on IC Markets | Official Blog.

UK December flash services PMI 52.1 vs 51.6 expected

December 16, 2025 16:39 Forexlive Latest News Market News

- Prior 51.3

- Manufacturing PMI 51.2 vs 50.4 expected

- Prior 50.2

- Composite PMI 52.1 vs 51.6 expected

- Prior 51.2

These are nice beats, but the commentary isn’t as good. The agency cites lacklustre growth, worryingly widespread job losses and renewed upturn in selling price inflation across both goods and services.

It keeps the BoE on track to cut rates on Thursday, but the central bank will likely sound more cautious on the next moves, remaining highly data-dependent.

Key Findings:

- Output growth accelerates in December, led by

sharpest rise in new business for 14 months

Comment:

Chris Williamson, Chief Business Economist at S&P

Global Market Intelligence:

“December’s flash PMI surveys brought welcome news on

faster economic growth at the end of the year, with businesses

buoyed in part by the post-Budget lifting of uncertainty. The

PMI is consistent with GDP growth accelerating to 0.2% in

December, albeit with a more modest 0.1% gain signalled for

the fourth quarter as a whole.

“It’s a big relief that business confidence has not slumped in a

repeat of last year’s post-Budget gloom. Instead, companies

have ended the year on a slightly more optimistic note amid

signs of improving demand now that some of the uncertainty

created by the Budget has cleared. New orders are in fact

growing at the fastest rate for over a year.

“However, the overall pace of output and demand growth

remains lacklustre, and the expansion is still very dependent

on technology and financial services activity, with many other

parts of the economy struggling to grow or in decline.

“Job losses are also again worryingly widespread, and it

remains to be seen whether the uptick in orders during

December will persuade more companies to start hiring again,

especially as rising staff costs continue to be reported as one

of the key concerns of businesses. These higher cost pressures

were in turn cited as the key cause of a renewed upturn in

selling price inflation across both goods and services.

“The sluggish growth and worrying jobs data from the flash

PMI data therefore suggest that the odds remain in favour of

a further cut to interest rates at the December MPC meeting,

but that the path to further rate cuts in 2026 remains very data

dependent, as policymakers await confirmation that price

pressures are going to soften materially as the year proceeds.”

This article was written by Giuseppe Dellamotta at investinglive.com.